Amount of tax not to exceed 100,000. Note. If the Form 1118 is filed and assigned to a corporation, the company's name and identifying information must appear on the Form 1043. If the Form 1118 is filed and assigned to an employer, the employer must include the Form 1043(S) to determine the employer's withheld taxes under Revenue Ruling 2009-51. Refer to the Instructions for Form 1043 for information on assigning a Form 1118 to an employer. Use the tax year to which the Form 1118 applies. Check box 1 on each Form 1118, except Form 1118, Part II. No. Amount of tax. Note. Use one of the following options to include income from a trade or business with your trade or business. A. The employee's distributive share of the partnership's distributive share of an item of income or loss on which no credit was allowed is included in the employee's gross income as in the case of a creditable event; therefore no additional information is required on Form 1040, Schedule C. B. The employee's distributive share of the partnership's distributive share of an item of income or loss on which an allowable credit was allowed is excluded from the employee's gross income and added to the employee's gross income for the taxable year as in the case of an allowable credit. C. The employee's distributive share of the partnership's distributive share of any gain that the employee's trade or business, including the employee's trade or business activities, generated in the relevant period (within the meaning of section 1221(a)), is excluded from the employee's gross income and added to the employee's gross income for the relevant period (within the meaning of section 1221(a)) to the extent that the gain was not derived on the sale of tangible personal property used in the trade or business. 1. Exclude gains from sale of, or exchanges for, real property or intangible property on which no credit was allowed. Examples of property whose use in the operation of the trade or business was not deemed to reduce the cost of the property: farm equipment, inventory or real estate used as a business asset, or land used, in whole or in part, to support a farm in which such property is located. 2. Exclude gains from sales of, or exchanges for, partnerships items using gross receipts.

Get the free form 1118 2009

Show details

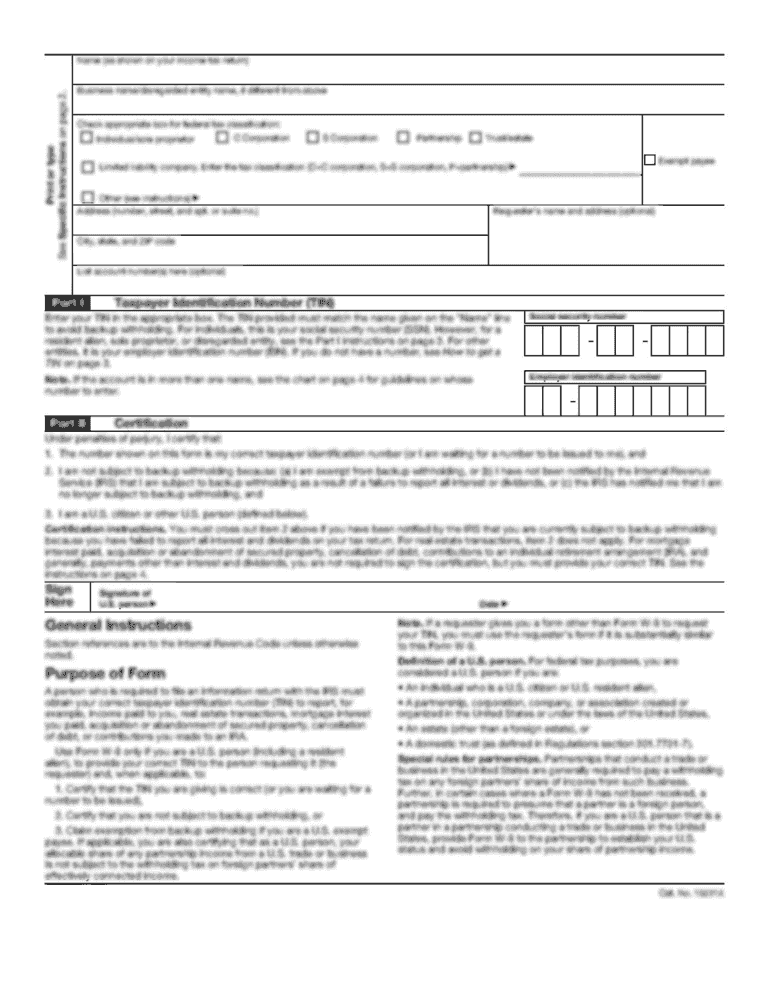

Cat. No. 10900F Form 1118 Rev. 12-2009 Page 2 Part I Foreign Taxes Paid Accrued and Deemed Paid see instructions 1. Form Rev. December 2009 Department of the Treasury Internal Revenue Service Name of corporation Foreign Tax Credit Corporations See Attach For calendar year 20 separate instructions. to the corporation s tax return. or other tax year beginning OMB No. 1545-0122 and ending Employer identification number Use a separate Form 1118 for ...

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign

Edit your form 1118 2009 form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your form 1118 2009 form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Fill form : Try Risk Free

Fill out your form 1118 2009 online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Not the form you were looking for?

Keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.