Get the free COVID-19: Consumer Loan Forbearance and Other Relief ...

Show details

This document allows individuals to request temporary financial relief through loan forbearance or payment deferral due to hardships caused by the COVID-19 Pandemic.

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign covid-19 consumer loan forbearance

Edit your covid-19 consumer loan forbearance form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your covid-19 consumer loan forbearance form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing covid-19 consumer loan forbearance online

Follow the steps below to use a professional PDF editor:

1

Register the account. Begin by clicking Start Free Trial and create a profile if you are a new user.

2

Prepare a file. Use the Add New button to start a new project. Then, using your device, upload your file to the system by importing it from internal mail, the cloud, or adding its URL.

3

Edit covid-19 consumer loan forbearance. Rearrange and rotate pages, insert new and alter existing texts, add new objects, and take advantage of other helpful tools. Click Done to apply changes and return to your Dashboard. Go to the Documents tab to access merging, splitting, locking, or unlocking functions.

4

Get your file. Select the name of your file in the docs list and choose your preferred exporting method. You can download it as a PDF, save it in another format, send it by email, or transfer it to the cloud.

Dealing with documents is always simple with pdfFiller.

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out covid-19 consumer loan forbearance

How to fill out covid-19 consumer loan forbearance

01

Gather necessary documentation, including proof of income and any relevant financial statements.

02

Review your loan agreement to understand eligibility for forbearance.

03

Contact your loan servicer to inquire about forbearance options offered due to COVID-19.

04

Fill out the required forbearance application form provided by your loan servicer.

05

Provide honest and accurate information on the application, including any financial hardships caused by the pandemic.

06

Submit the completed application along with any necessary documentation to your loan servicer.

07

Await confirmation of your application status and any next steps from your servicer.

Who needs covid-19 consumer loan forbearance?

01

Individuals facing financial hardships due to job loss, reduced income, or medical expenses related to COVID-19.

02

Borrowers struggling to make monthly loan payments as a result of the pandemic.

03

People who want temporary relief from their loan obligations during the crisis.

Navigating the COVID-19 Consumer Loan Forbearance Form

Understanding the COVID-19 consumer loan forbearance

Loan forbearance refers to an agreement between a borrower and lender to temporarily postpone or reduce payment requirements on a loan. During the COVID-19 pandemic, regions across the globe experienced unprecedented economic disruption. Loan forbearance became a critical tool for individuals and businesses alike, allowing them to manage their financial burdens during a period of uncertainty and income instability.

Forbearance is particularly important as it helps prevent delinquencies and defaults. Many consumers found themselves unable to make regular payments due to job losses, reduced hours, or unexpected expenses. By offering this relief, lenders contributed significantly to retaining household stability and maintaining consumer confidence.

Mortgage loans - Homeowners experiencing financial hardship can often suspend their mortgage payments.

Student loans - Many federal and private student loan borrowers can also benefit from temporary relief.

Personal loans - Customers with personal loans can negotiate forbearance terms directly with lenders.

Auto loans - Car borrowers may find relief options to avoid repossession or missed payments.

Eligibility criteria for forbearance

To be eligible for COVID-19 loan forbearance, applicants need to demonstrate specific circumstances and conditions. Individuals and small businesses that have faced financial hardship due to the pandemic can seek assistance. Many lenders established straightforward criteria ensuring accessibility for those in need, recognizing the varied impacts of the crisis on consumers.

The primary documentation required generally includes proof of income loss caused by COVID-19, such as pay stubs or unemployment benefit notifications. Additionally, providing loan account details is essential for the application process. Understanding the implications on credit scores is also crucial; while entering forbearance may not negatively impact your credit score, it's vital to stay informed about how forbearance differs from deferment.

Individuals - Borrowers who have lost income or job due to COVID-19 may apply.

Small businesses - Businesses demonstrating financial distress due to the pandemic are also eligible.

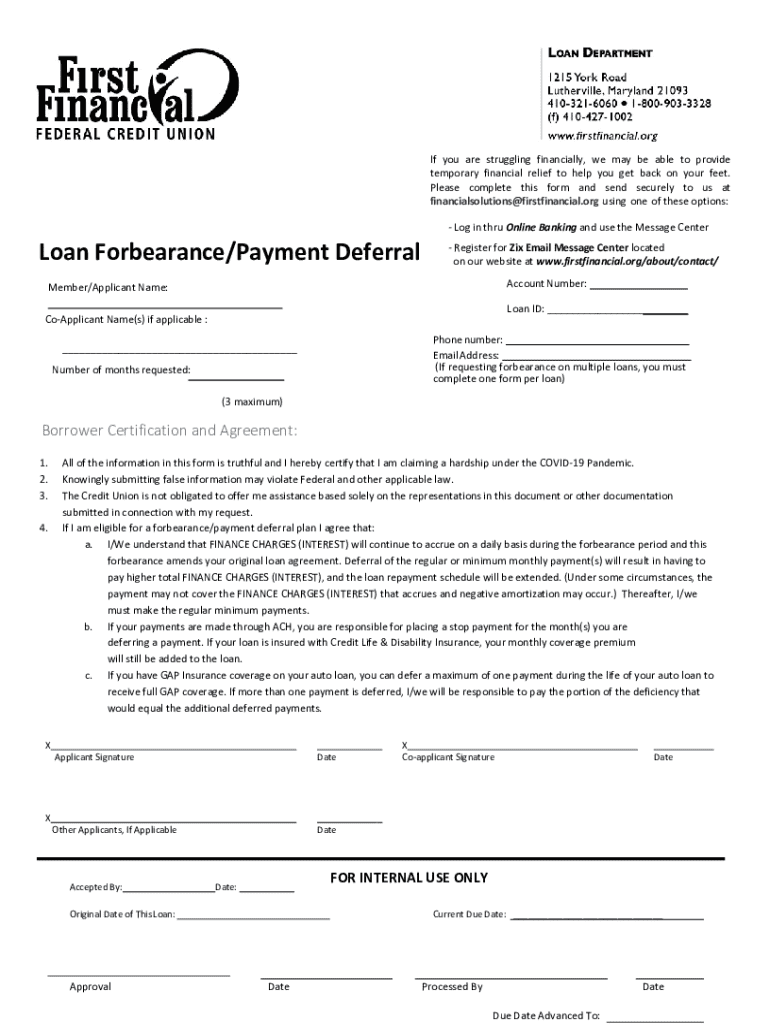

The COVID-19 consumer loan forbearance form explained

The COVID-19 consumer loan forbearance form is essential for anyone seeking to apply for payment relief. This form outlines the borrower's current financial situation and requests the lender to accept reduced payment terms or temporarily suspend payments. Without this form, there is no official record of the borrower's request, and the oversight may result in missed opportunities for relief.

Finding the right form is made easier through various online resources. Most lenders and financial institutions provide downloadable forms directly on their websites, making access straightforward. For added convenience, the pdfFiller platform allows users to access the form directly, providing customization for individual needs.

Step-by-step guide to completing the forbearance form

Before completing the forbearance form, prepare by gathering all necessary documents, including your loan details, proof of income changes, and any correspondence from your lender regarding relief options. Being organized will make filling out the form smoother and more efficient.

Once you’re prepared, follow this detailed walkthrough of each section on the loan forbearance form:

Personal Information - Include your full name, contact information, and any necessary references.

Loan Details - Fill in specifics about your loan, including account numbers and type of loan.

Financial Hardship Explanation - Clearly outline the changes that have impacted your ability to pay.

Signature and Submission Process - Sign the form and follow submission guidelines specified by your lender.

Be cautious of common mistakes, such as failing to include all necessary information or not clearly articulating the reasons for your financial hardship.

Editing and signing the forbearance form on pdfFiller

Editing the COVID-19 consumer loan forbearance form is simplified with pdfFiller’s robust tools. Users can enhance the form by utilizing interactive features that allow them to add notes, comments, or additional documentation.

Once the form is complete, signing it digitally is straightforward. The electronic signature process offered by pdfFiller is legally recognized and streamlines the submission process. Digital signatures eliminate the need for printing, thereby saving time and reducing paper waste.

Submitting the completed form

After completing the forbearance form, the next step is submission. Ensure that you review the submission instructions, as different lenders may have varied methods for receiving forms. Many lenders have online portals while others accept forms via email or traditional mail. Familiarize yourself with the deadlines to avoid delays in processing your request.

Monitoring the application status is crucial once submitted. Keep track of any confirmation emails and follow up with your lender if you do not receive an acknowledgment within a reasonable timeframe. Knowing what to expect in terms of timelines can alleviate anxiety and keep you informed.

Managing your loan during forbearance

After receiving approval for forbearance, understanding the terms is vital. Depending on the agreements set forth by your lender, borrowers may have options for managing any missed payments during the forbearance period. Some may require a repayment plan, while others offer flexibility to extend relief.

It's important to maintain open communication with your lender throughout this process. Establishing a rapport with your lender and having written documentation of all conversations can be beneficial in case any issues arise later.

Alternatives to forbearance

For borrowers who may not find forbearance to be the best option, exploring alternatives can be a valuable avenue. Understanding the differences between loan deferment and forbearance is essential. Unlike forbearance, which pauses payment obligations, deferment allows postponed payment without accruing interest.

Moreover, other options may include structured payment plans or modifications that allow borrowers to pay off their loan more gradually. Government assistance programs and local resources can also provide additional support during challenging financial times.

Frequently asked questions (FAQs)

Many borrowers have common questions about COVID-19 loan forbearance. One of the most frequent inquiries concerns the duration of forbearance. Generally, the length can vary based on the lender’s policies and the type of loan.

Other concerns include whether forbearance can be extended if circumstances change and how to proceed if your financial situation worsens. It’s essential to proactively engage with your lender to address any fresh challenges as they arise.

Tools and resources for further assistance

Various tools are available to help borrowers manage their loans effectively. For example, loan repayment calculators on pdfFiller allow users to visualize their repayment journey, providing insights into potential payment structures.

For more personalized support, individuals can seek assistance from financial advisors who can offer expert advice tailored to their unique situations. Additionally, consumer advocacy organizations often provide resources and guidance.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I modify covid-19 consumer loan forbearance without leaving Google Drive?

You can quickly improve your document management and form preparation by integrating pdfFiller with Google Docs so that you can create, edit and sign documents directly from your Google Drive. The add-on enables you to transform your covid-19 consumer loan forbearance into a dynamic fillable form that you can manage and eSign from any internet-connected device.

How do I edit covid-19 consumer loan forbearance online?

The editing procedure is simple with pdfFiller. Open your covid-19 consumer loan forbearance in the editor, which is quite user-friendly. You may use it to blackout, redact, write, and erase text, add photos, draw arrows and lines, set sticky notes and text boxes, and much more.

Can I create an electronic signature for the covid-19 consumer loan forbearance in Chrome?

Yes. You can use pdfFiller to sign documents and use all of the features of the PDF editor in one place if you add this solution to Chrome. In order to use the extension, you can draw or write an electronic signature. You can also upload a picture of your handwritten signature. There is no need to worry about how long it takes to sign your covid-19 consumer loan forbearance.

What is covid-19 consumer loan forbearance?

Covid-19 consumer loan forbearance is a temporary relief program that allows borrowers to pause or reduce their loan payments without facing penalties, as a response to the financial impact of the pandemic.

Who is required to file covid-19 consumer loan forbearance?

Consumers who are experiencing financial hardship due to the Covid-19 pandemic and wish to temporarily suspend or reduce their loan payments are required to file for forbearance.

How to fill out covid-19 consumer loan forbearance?

To fill out a covid-19 consumer loan forbearance application, borrowers typically need to contact their loan servicer, provide documentation of financial hardship, and complete any required forms as instructed by the servicer.

What is the purpose of covid-19 consumer loan forbearance?

The purpose of covid-19 consumer loan forbearance is to provide financial relief to borrowers affected by the pandemic by allowing them to temporarily avoid making full loan payments, thus helping them manage their financial obligations.

What information must be reported on covid-19 consumer loan forbearance?

Information that must be reported regarding covid-19 consumer loan forbearance may include the borrower's loan details, the duration of the forbearance, any missed payments, and whether the forbearance was granted due to financial hardship related to Covid-19.

Fill out your covid-19 consumer loan forbearance online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Covid-19 Consumer Loan Forbearance is not the form you're looking for?Search for another form here.

Relevant keywords

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.