Get the free Credit Risk Assessment

Show details

This document is designed to gather information for assessing the credit risk of customers, including details about the company\'s contact information, banking information, and trade references.

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign credit risk assessment

Edit your credit risk assessment form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your credit risk assessment form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing credit risk assessment online

Follow the guidelines below to use a professional PDF editor:

1

Set up an account. If you are a new user, click Start Free Trial and establish a profile.

2

Prepare a file. Use the Add New button to start a new project. Then, using your device, upload your file to the system by importing it from internal mail, the cloud, or adding its URL.

3

Edit credit risk assessment. Rearrange and rotate pages, add and edit text, and use additional tools. To save changes and return to your Dashboard, click Done. The Documents tab allows you to merge, divide, lock, or unlock files.

4

Get your file. Select your file from the documents list and pick your export method. You may save it as a PDF, email it, or upload it to the cloud.

pdfFiller makes working with documents easier than you could ever imagine. Try it for yourself by creating an account!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out credit risk assessment

How to fill out credit risk assessment

01

Gather required financial documents such as income statements, balance sheets, and tax returns.

02

Assess the applicant's credit history by reviewing credit reports from credit bureaus.

03

Evaluate the applicant's current debts and financial obligations.

04

Analyze the applicant's cash flow to determine their ability to repay loans.

05

Rate the applicant on a predefined risk scale based on the analysis.

06

Document findings and include any recommendations for approval or denial.

Who needs credit risk assessment?

01

Banks and financial institutions offering loans or credit.

02

Businesses assessing potential credit customers.

03

Investors evaluating the creditworthiness of potential investments.

04

Insurance companies determining risk profiles for underwriting.

05

Any organization extending credit to individuals or businesses.

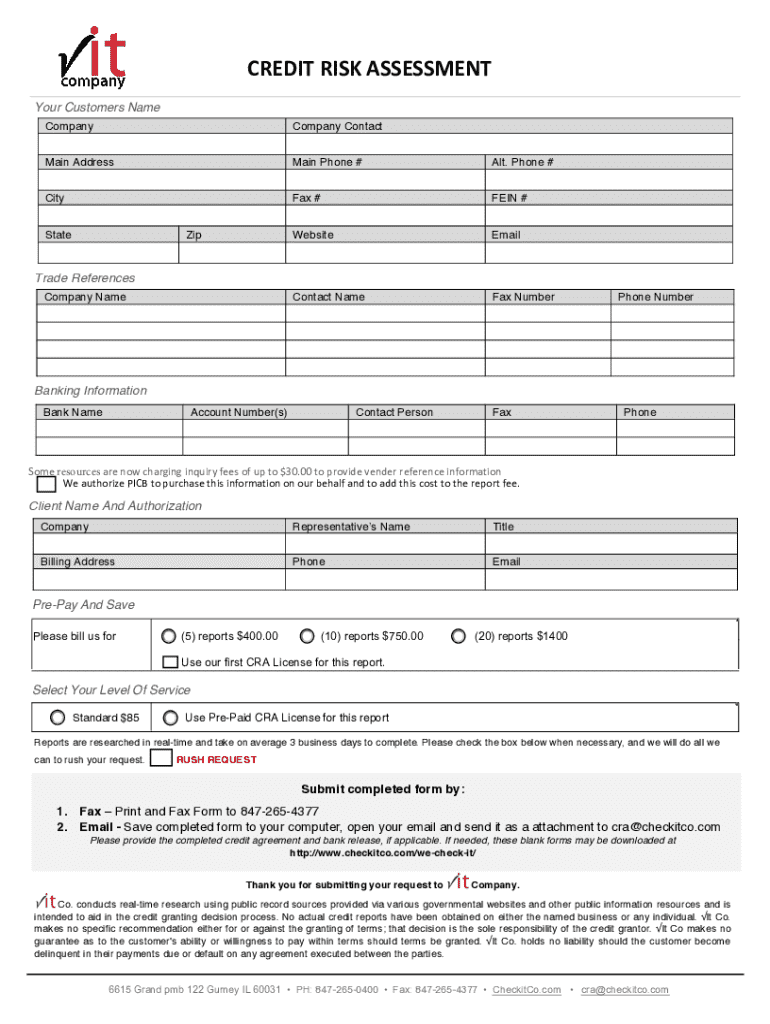

Understanding and Using the Credit Risk Assessment Form

Understanding the credit risk assessment form

A credit risk assessment form is a crucial document in the lending process, designed to evaluate the financial stability and creditworthiness of a borrower. This assessment helps lenders determine the likelihood that a borrower will default on a loan. Given that defaults can significantly impact a lender's bottom line, this form plays an essential role in risk management strategies. Credit risk assessment forms are not only fundamental for banks and financial institutions but also for small businesses and individual lenders looking to mitigate financial exposure.

Key components of a credit risk assessment form include borrower information, financial statements, and credit history. Understanding these components is vital for an accurate assessment. Categories of borrower information typically include personal and contact information, as well as details about their business or employment. Financial statements such as income statements and balance sheets provide insight into the economic health of the borrower. Lastly, a comprehensive view of the borrower's credit history can give an indication of their borrowing behavior, which is crucial for risk evaluation.

Details about the borrower including identity and employment.

Includes balance sheets, income statements, and cash flow statements.

Background of the borrower’s borrowing and repayment history.

Completing the credit risk assessment form

Filling out a credit risk assessment form may seem daunting, but it can be simplified by following structured steps. The first step involves identifying the borrower's details. This includes capturing their name, contact information, and relevant business profile, which provides context to their financial activities. Make sure all information is current and accurate. Inaccuracies can lead to misjudgment in the evaluation.

Next, it’s essential to collect the necessary financial statements. The types required typically include the balance sheet, income statement, and sometimes the cash flow statement. Borrowers can obtain these documents from their accountants or financial software. These statements are vital as they showcase the borrower's financial health, enabling a true reflection of their capability to repay the loan.

After gathering financial statements, analyze them for key indicators such as liquidity and profitability. Liquidity assessments help determine whether the borrower can meet short-term obligations. Profitability metrics measure the borrower's capacity to generate earnings relative to their expenses over time.

Calculating financial ratios is the next crucial step. Ratios such as the debt-to-equity ratio and current ratio provide insights into the borrower's financial leverage and ability to meet short-term liabilities. Finally, assessing the borrower's credit history through credit reports adds another layer to understanding their behavior in past borrowing.

Identifying the borrower's details: Name, contact information, and business profile.

Collecting financial statements: Obtain balance sheets, income statements, and more.

Analyzing financial statements: Assess liquidity and profitability indicators.

Calculating financial ratios: Common ratios for credit assessment.

Determining credit history: Resources for checking credit scores.

In-depth analysis of the borrower’s financial position

Estimating the borrower's current financial position is inherently tied to evaluating their assets versus liabilities. This helps to understand whether they possess sufficient resources to cover their obligations. A well-prepared balance sheet is crucial here, as it offers a snapshot of what the borrower owns and owes at any given moment. Additionally, assessing cash flow statements reveals how money moves in and out of the business—critical for understanding operating efficiency.

Predicting the future income or profits of a borrower requires using reliable forecasting methods. This may involve examining industry trends, economic indicators, and the borrower’s historical performance. Various factors, such as competition, market conditions, and internal operations, can significantly influence future profitability. An awareness of these dynamics can help lenders make informed decisions regarding to loan approval or the terms of the proposed loan.

Evaluating assets vs. liabilities: Understanding net worth.

Assessing cash flow statements: Monitoring operational efficiency.

Methods for forecasting income: Exploring historical performance.

Factors influencing profitability: Market conditions and competition.

Loan purpose and risk assessment

Understanding the loan purpose is critical in the credit risk assessment process. Loans can be categorized into various types, including personal loans, business expansion loans, or equipment financing. Each type presents unique risks and potential returns for lenders. For instance, a personal loan might be less risky than a business expansion loan, which typically involves larger sums and uncertain returns.

Evaluating collateral, when applicable, is another crucial component of this assessment. Different types of collateral can significantly affect the perceived risk level. For example, loans secured by real estate might be considered lower risk compared to those secured by inventory or equipment, given the stability and liquidity aspects associated with property. Understanding the implications of collateral can aid in making more refined lending decisions.

Different loan purposes: Personal loans vs. business loans.

Impact of loan purpose on credit risk: Assessing the risk profile.

Types of collateral: Real estate, inventory, equipment.

How collateral affects risk level: Evaluating risk mitigation.

Utilizing interactive tools for enhanced assessment

In an increasingly digital world, utilizing interactive tools for credit risk assessment has become essential. pdfFiller provides various features that can significantly streamline the process, such as document editing and management capabilities. Users can collaborate in real-time, share the credit risk assessment form effortlessly, and make necessary edits or adjustments easily. This collaborative approach can lead to more precise evaluations and a more efficient workflow.

Additionally, eSignature capabilities enable users to finalize documents without the tedious process of printing, signing, and scanning. This not only speeds up the process but also enhances security and compliance. Integrating interactive tools enhances the ability to process, evaluate, and manage documents from anywhere, making it an ideal solution for individuals and teams seeking comprehensive and flexible document creation solutions.

Introduction to pdfFiller’s interactive tools: Document editing features.

Benefits of workflow collaboration: Real-time feedback and document sharing.

eSignature capabilities for streamlined processes.

Access-from-anywhere solutions for teams.

Best practices for credit risk assessment

Applying best practices when filling out the credit risk assessment form is vital for both accuracy and efficiency. Regularly updating financial data ensures that all assessments are based on the most current information available. This can make a significant difference in the evaluation's outcome and support informed lending decisions. Additionally, maintaining detailed records will aid in subsequent assessments and promote transparency should questions arise later.

Avoiding common mistakes is just as crucial. Incomplete information can lead to improper risk evaluations, and skipping vital analysis can expose lenders to bond defaults. Neglecting to review all relevant data, such as market indicators and borrower credit history, can lead to misguided judgments. Establishing a checklist can eliminate this risk and improve the process’s integrity.

Regularly update financial data: Ensure accuracy in the assessment.

Maintain detailed records: Support transparency and future assessments.

Avoid incomplete information: Assess all relevant data points.

Use a checklist: Improve integrity and reduce oversight.

Maximizing the use of the credit risk assessment form in decision-making

The completed credit risk assessment form serves a crucial role in lending decisions. Lenders can utilize the comprehensive evaluations to make informed choices regarding loan approvals, interest rates, and repayment terms. By carefully considering the financial position, the intended use of the loan, and the borrower’s credit history, lenders can create a well-rounded picture of potential risks and rewards.

Integrating results from the credit risk assessment into overall financial planning and risk management strategies is essential for informed business practices. Such integration supports proactive decision-making and long-term sustainability. By aligning lending practices with a thorough understanding of credit risk, lenders can strategically manage their portfolios and reduce potential losses associated with defaults.

Using the completed assessment for lending decisions: Criteria for approval.

Integrating results into financial planning: Supporting long-term strategies.

Aligning lending practices with risk understanding: Proactive portfolio management.

Reducing potential losses through informed decision-making.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I modify credit risk assessment without leaving Google Drive?

You can quickly improve your document management and form preparation by integrating pdfFiller with Google Docs so that you can create, edit and sign documents directly from your Google Drive. The add-on enables you to transform your credit risk assessment into a dynamic fillable form that you can manage and eSign from any internet-connected device.

How can I edit credit risk assessment on a smartphone?

The pdfFiller mobile applications for iOS and Android are the easiest way to edit documents on the go. You may get them from the Apple Store and Google Play. More info about the applications here. Install and log in to edit credit risk assessment.

Can I edit credit risk assessment on an iOS device?

Create, edit, and share credit risk assessment from your iOS smartphone with the pdfFiller mobile app. Installing it from the Apple Store takes only a few seconds. You may take advantage of a free trial and select a subscription that meets your needs.

What is credit risk assessment?

Credit risk assessment is the process of evaluating the likelihood that a borrower will default on their financial obligations. It involves analyzing an individual's or organization's credit history, financial stability, and overall risk profile.

Who is required to file credit risk assessment?

Entities such as banks, credit unions, and other financial institutions are typically required to file credit risk assessments, especially when extending credit or loans to individuals or businesses.

How to fill out credit risk assessment?

Filling out a credit risk assessment usually involves gathering necessary financial documents, assessing credit history through credit reports, analyzing financial statements, and providing relevant information about the borrower's ability to repay debt.

What is the purpose of credit risk assessment?

The purpose of credit risk assessment is to determine the level of risk associated with lending to a particular borrower, to mitigate potential losses for lenders, and to set appropriate terms and interest rates for loans.

What information must be reported on credit risk assessment?

Credit risk assessments must report information including the borrower’s credit score, payment history, debt-to-income ratio, employment status, financial assets, liabilities, and any other relevant financial data that indicates the borrower's creditworthiness.

Fill out your credit risk assessment online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Credit Risk Assessment is not the form you're looking for?Search for another form here.

Relevant keywords

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.