Credit Dispute Letters That Work

What is Credit dispute letters that work?

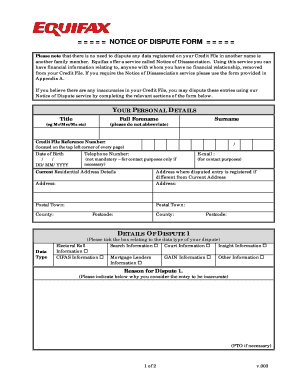

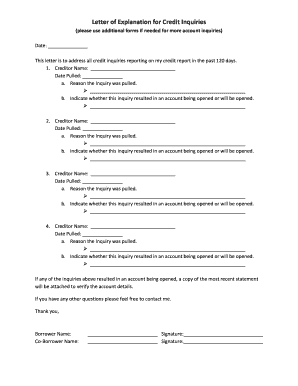

Credit dispute letters that work are professional. They are formal documents used to challenge incorrect information on your credit report. These letters are essential in disputing inaccuracies and improving your credit score.

What are the types of Credit dispute letters that work?

There are several types of Credit dispute letters that work, including: Goodwill letters, Debt validation letters, and Pay-for-delete letters.

Goodwill letters

Debt validation letters

Pay-for-delete letters

How to complete Credit dispute letters that work

Completing Credit dispute letters that work is a straightforward process. Here are the steps to follow:

01

Gather your credit report and identify inaccuracies

02

Write a clear and concise dispute letter addressing each error

03

Include any supporting documentation to strengthen your case

04

Send the letter via certified mail to ensure it's received

05

Follow up with the credit bureau if necessary

pdfFiller empowers users to create, edit, and share documents online. Offering unlimited fillable templates and powerful editing tools, pdfFiller is the only PDF editor users need to get their documents done.

Video Tutorial How to Fill Out Credit dispute letters that work

Thousands of positive reviews can’t be wrong

Read more or give pdfFiller a try to experience the benefits for yourself

Questions & answers

Do 609 letters really work?

In general, a 609 letter is not a legal loophole that consumers can use to remove accurate information from their credit reports. This means they can't relieve you of any verifiable debt. If a credit bureau is able to verify your debt, it will stay on your report. They also can't relieve you of your existing debt.

What is a 623 dispute letter?

4) 623 credit dispute letter A business uses a 623 credit dispute letter when all other attempts to remove dispute information have failed. It refers to Section 623 of the Fair Credit Reporting Act and contacts the data furnisher to prove that a debt belongs to the company.

What is the 623 credit law?

Section 623 of the FCRA and Regulation V generally provide that a furnisher must not furnish inaccurate consumer information to a CRA, and that furnishers must investigate a consumer's dispute that the furnished information is inaccurate or incomplete.

What is the 609 letter?

A 609 dispute letter is a request to the credit bureaus (TransUnion, Equifax, and Experian) to remove harmful, inaccurate, and not verifiable data from your credit report.

What is a 623 letter for charge off?

The 623 credit dispute letter, which references Section 623 of the FCRA, is a “last-ditch” attempt to remove a record. Once you go through the process of sending a general dispute letter or a 609, then sending a 611 dispute letter, you have the last option of contacting the data furnisher directly.

Is a 609 dispute letter effective?

If disputes are successful, the credit bureaus may remove the negative item. Any accurate or verifiable information will stay on your credit report—a 609 letter doesn't guarantee its removal. However, you may increase your chances of removal if you follow a 609 letter template and provide enough information.