IRS 1042 2011 free printable template

Get, Create, Make, and Sign IRS 1042

Instructions and Help about IRS 1042

How to edit IRS 1042

How to fill out IRS 1042

About IRS previous version

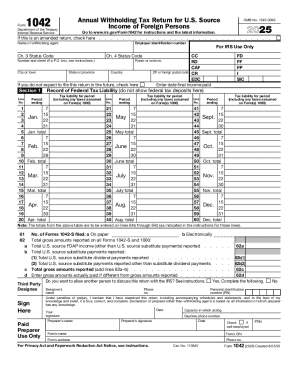

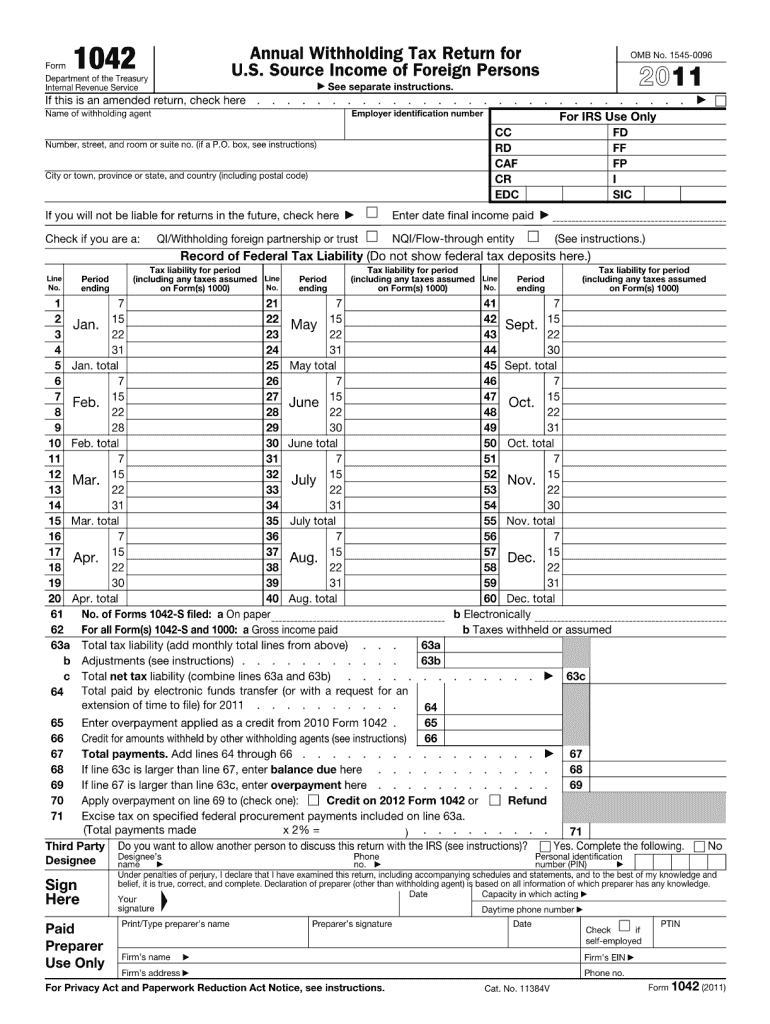

What is IRS 1042?

Who needs the form?

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about IRS 1042

What should I do if I discover an error on my filed 2011 form 1042?

If you find an error on your filed 2011 form 1042, you should correct it by filing an amended return. Ensure you clearly indicate that it is a correction and include the correct information along with any supporting documentation required. It's advisable to send the amended form as soon as possible to minimize any potential penalties or complications.

How can I verify the receipt and processing of my submitted 2011 form 1042?

To verify the receipt and processing of your 2011 form 1042, you can check the IRS website for updates or use their e-filing tracking tools, if applicable. Keep a copy of your submission and any confirmation notes or numbers received upon filing, as these will help in tracking your submission status.

Are there any specific data security measures I should take when filing my 2011 form 1042 electronically?

When filing your 2011 form 1042 electronically, ensure you are using secure networks and reliable e-filing software that complies with IRS standards. Additionally, consider using encrypted emails or secure portals when submitting sensitive information to protect your data from unauthorized access.

What should I include if I'm filing a 2011 form 1042 on behalf of a foreign payee?

When filing a 2011 form 1042 on behalf of a foreign payee, ensure you include a valid power of attorney or authorization documentation along with the form. This confirms that you are authorized to act on behalf of the payee and helps in processing the return accurately and promptly.