Last updated on May 4, 2026

Freddie Mac 65 / Fannie Mae 1003 - Residential 1992 free printable template

pdfFiller is not affiliated with any government organization

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

What is Freddie Mac 65 / Fannie Mae 1003 - Residential

The Uniform Residential Loan Application is a standardized document used by borrowers to apply for a residential mortgage loan.

pdfFiller scores top ratings on review platforms

What do you like best?

It has a lot of features but not overly complicated. There is a lot of function, and it runs smoothly.

What do you dislike?

Occasionally navigation of the sight has been sticky.

What problems are you solving with the product? What benefits have you realized?

I am always needing to combine multiple PDF files into one, and then do some filling and signing. PDF Filler has sped that process up.

It has a lot of features but not overly complicated. There is a lot of function, and it runs smoothly.

What do you dislike?

Occasionally navigation of the sight has been sticky.

What problems are you solving with the product? What benefits have you realized?

I am always needing to combine multiple PDF files into one, and then do some filling and signing. PDF Filler has sped that process up.

What do you like best?

I used PDFfiller to complete PDF versions of scholarship applications and it was such a time savings and so easy to work with that it was worth every penny. Since that time I have found many more features, like the verified signing, that it has become a necessary tool for both work and personal use.

What do you dislike?

Not really anything I disliked. I think the price for a personal user is a little expensive.

What problems are you solving with the product? What benefits have you realized?

Verified signatures and completing PDF documents.

I used PDFfiller to complete PDF versions of scholarship applications and it was such a time savings and so easy to work with that it was worth every penny. Since that time I have found many more features, like the verified signing, that it has become a necessary tool for both work and personal use.

What do you dislike?

Not really anything I disliked. I think the price for a personal user is a little expensive.

What problems are you solving with the product? What benefits have you realized?

Verified signatures and completing PDF documents.

What do you like best?

I like PDFFIller because it always works, unlike some other PDF tools I've purchased in the past. PDFFiller is my goto tool and will become my exclusive tool once my other package expires.

What do you dislike?

There's a little confusion when saving to my Google Drive. Now and then, the file can't be found there when on my phone.

Recommendations to others considering the product:

I've also used Ecopy for several years and just find PDFfiller to be more user friendly and stable. As I said, it's my goto PDF tool.

What problems are you solving with the product? What benefits have you realized?

I fill in forms, I create forms listing medical issues/histories, electronic signatures are always handy. I also convert to Office Documents if needed.

I like PDFFIller because it always works, unlike some other PDF tools I've purchased in the past. PDFFiller is my goto tool and will become my exclusive tool once my other package expires.

What do you dislike?

There's a little confusion when saving to my Google Drive. Now and then, the file can't be found there when on my phone.

Recommendations to others considering the product:

I've also used Ecopy for several years and just find PDFfiller to be more user friendly and stable. As I said, it's my goto PDF tool.

What problems are you solving with the product? What benefits have you realized?

I fill in forms, I create forms listing medical issues/histories, electronic signatures are always handy. I also convert to Office Documents if needed.

What do you like best?

Easy to learn and easy to use. I use it for filling in permit application forms from the county agencies we need to apply for permits from. They are extremely frustrating in redundancy, asking for the same information over and over. PDFFiller makes it easy to fill out these forms.

What do you dislike?

Some of the buttons seem a little clunky but they are easy to use.

Recommendations to others considering the product:

PDFFILLER is an inexpensive alternative to other vendors.

What problems are you solving with the product? What benefits have you realized?

Easy to fill PDF forms and easy to share them with other people.

Easy to learn and easy to use. I use it for filling in permit application forms from the county agencies we need to apply for permits from. They are extremely frustrating in redundancy, asking for the same information over and over. PDFFiller makes it easy to fill out these forms.

What do you dislike?

Some of the buttons seem a little clunky but they are easy to use.

Recommendations to others considering the product:

PDFFILLER is an inexpensive alternative to other vendors.

What problems are you solving with the product? What benefits have you realized?

Easy to fill PDF forms and easy to share them with other people.

What do you like best?

I have tried many different programs. I find PDFfiller to be the easiest to use for anything re: PDFs and to get signatures on paperwork.

What do you dislike?

It is a little more expensive than some of the other programs

Recommendations to others considering the product:

I highly recommend it for people who are not technical experts

What problems are you solving with the product? What benefits have you realized?

Signing documents, converting WORD files, editing PDFs

I have tried many different programs. I find PDFfiller to be the easiest to use for anything re: PDFs and to get signatures on paperwork.

What do you dislike?

It is a little more expensive than some of the other programs

Recommendations to others considering the product:

I highly recommend it for people who are not technical experts

What problems are you solving with the product? What benefits have you realized?

Signing documents, converting WORD files, editing PDFs

What do you like best?

I started using PDFfiller as an alternative to Adobe Acrobat, which is not available for Chromebook. I expected it to be something I could use to make small edits to PDFs and also to fill in non-fillable forms. It has proven to be way WAY more than that. I like that the program is incredibly versatile

What do you dislike?

I wish I could save files to by Google Drive into the folders that I want rather than having to move them from the PDFfiller folder.

Recommendations to others considering the product:

Try it first, but it really is that good.

What problems are you solving with the product? What benefits have you realized?

editing PDFs, converting PDfs to Power Point, signing documents directly,

I started using PDFfiller as an alternative to Adobe Acrobat, which is not available for Chromebook. I expected it to be something I could use to make small edits to PDFs and also to fill in non-fillable forms. It has proven to be way WAY more than that. I like that the program is incredibly versatile

What do you dislike?

I wish I could save files to by Google Drive into the folders that I want rather than having to move them from the PDFfiller folder.

Recommendations to others considering the product:

Try it first, but it really is that good.

What problems are you solving with the product? What benefits have you realized?

editing PDFs, converting PDfs to Power Point, signing documents directly,

Who needs Freddie Mac 65 / Fannie Mae 1003 - Residential?

Explore how professionals across industries use pdfFiller.

Freddie Mac 65 / Fannie Mae 1003 - Residential is needed by:

-

Homebuyers seeking mortgage financing

-

Real estate agents assisting clients with loans

-

Financial institutions offering residential loans

-

Investors looking to purchase properties

-

Loan officers aiding clients through the application process

-

Co-borrowers working alongside the main borrower

Comprehensive Guide to Freddie Mac 65 / Fannie Mae 1003 - Residential

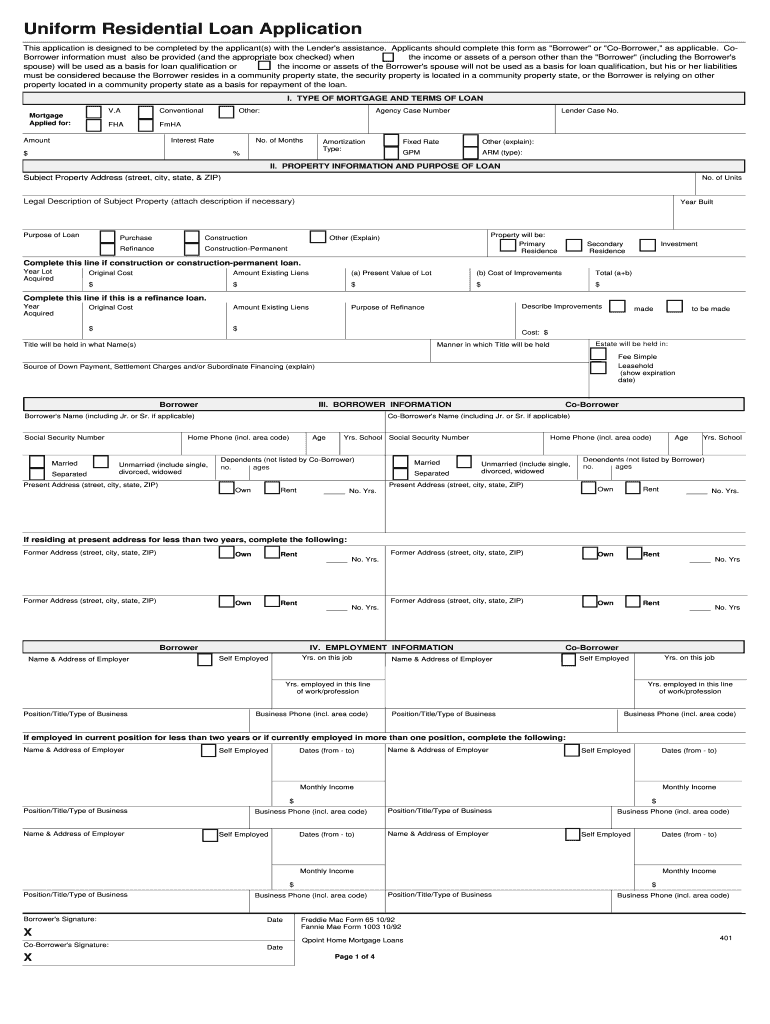

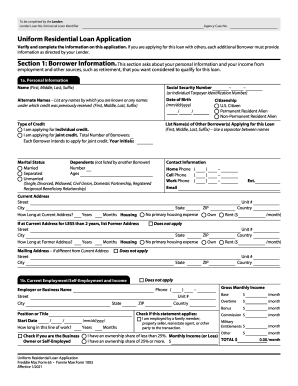

What is the Uniform Residential Loan Application?

The Uniform Residential Loan Application is a standardized form used in the mortgage process to apply for a residential mortgage loan. This form is significant as it helps in collecting essential information about the borrower's financial situation, making it easier for lenders to assess loan applications. By using this mortgage application form, both lenders and applicants benefit from a streamlined and organized process.

Standardization of the application allows for consistency across lenders, simplifying the experience for individuals applying for loans. The form serves as a crucial document in obtaining a residential mortgage loan, guiding applicants through necessary disclosures and requirements.

Purpose and Benefits of the Uniform Residential Loan Application

The Uniform Residential Loan Application has been developed to streamline the mortgage application process. Its primary purpose is to ensure comprehensive documentation of applicants' financial statuses, enabling lenders to make informed lending decisions. The form brings several benefits, making it easier for borrowers to gather and present their information coherently.

-

Streamlines the mortgage application process, reducing the time needed to complete submissions.

-

Ensures thorough documentation of the borrower’s financial situation.

-

Facilitates informed lending decisions by providing lenders with standardized data.

Key Features of the Uniform Residential Loan Application

This comprehensive loan application form includes multiple sections covering various aspects critical to the lending process. Key features include detailed sections on personal information, employment history, and comprehensive financial details.

-

Includes fields for property information and desired loan terms.

-

Provides a fillable format to aid in completing the application seamlessly.

-

Ensures all necessary information is captured for a thorough assessment.

Who Should Complete the Uniform Residential Loan Application?

The Uniform Residential Loan Application is designed for both borrowers and co-borrowers involved in obtaining a mortgage. It is suitable for a variety of individuals, particularly those seeking to purchase a new home.

-

First-time homebuyers utilizing the form to formalize their loan application.

-

Seasoned homebuyers looking to refinance or purchase additional properties.

-

Individuals co-signing a loan, providing additional security to the lender.

How to Fill Out the Uniform Residential Loan Application Online (Step-by-Step)

Completing the Uniform Residential Loan Application online can be accomplished by following these steps:

-

Access the application through a digital platform, such as pdfFiller.

-

Fill out personal information, ensuring accuracy in names and addresses.

-

Provide details regarding employment history and monthly income.

-

Input assets and liabilities, giving a complete picture of financial stability.

-

Review the filled form for completeness before submission.

Gathering necessary information beforehand can facilitate a smoother filling process. Utilizing the features of pdfFiller can enhance convenience while completing the application.

Common Errors and How to Avoid Them When Submitting the Uniform Residential Loan Application

Submitting the Uniform Residential Loan Application can lead to rejection or delays if common errors are not addressed. Notably, borrowers should avoid pitfalls that can hinder their chances of approval.

-

Incomplete sections that may raise concerns with lenders.

-

Inaccuracies in financial data that could misrepresent the borrower's position.

-

Failure to provide necessary supporting documentation.

Proactive steps to ensure that the application is accurate and complete can enhance approval chances. Resources are available for verification and validation prior to submission.

Security and Compliance for the Uniform Residential Loan Application

When submitting personal information via the Uniform Residential Loan Application, it’s essential to understand the security measures in place to protect sensitive data. pdfFiller utilizes 256-bit encryption to safeguard user information during the application process.

-

Compliance with relevant regulations such as HIPAA and GDPR ensures legal protection.

-

Security features help to protect borrower information from unauthorized access.

Using a secure platform introduces peace of mind when handling personal documents necessary for mortgage applications.

How to Submit the Uniform Residential Loan Application

Once the Uniform Residential Loan Application has been filled out, multiple submission methods are available to applicants. Understanding these methods can streamline the overall process.

-

Online submission through platforms like pdfFiller, allowing for immediate processing.

-

Mailing the completed application to the lender, ensuring a physical record.

After submission, it is crucial to keep track of the application status and obtain any necessary confirmations from the lender.

What Happens After You Submit the Uniform Residential Loan Application

After submitting the application, borrowers can expect a defined processing timeline from the lender. Typically, application reviews will include potential follow-ups or requests for additional information.

-

Timelines for processing applications can vary, but banks usually update applicants regularly.

-

Watch for communication about additional requirements or clarification needed from the lender.

Checking the application status is an important step in understanding the approval journey and addressing any emerging issues.

Enhance Your Application Experience with pdfFiller

Utilizing pdfFiller can significantly improve your experience in completing the Uniform Residential Loan Application. This platform simplifies the process, making it easier to fill out and submit necessary forms.

-

Benefits of using pdfFiller include the ability to eSign documents and create fillable forms quickly.

-

Digital signatures facilitate a faster and legally binding agreement process.

Starting with pdfFiller for all your form-filling needs can ease the burden of applying for a mortgage.

How to fill out the Freddie Mac 65 / Fannie Mae 1003 - Residential

-

1.Access the Uniform Residential Loan Application on pdfFiller by searching for the form in the document library or uploading it directly if you have a copy.

-

2.Once the form is open, navigate through the sections clearly labeled for borrower, co-borrower, property information, loan terms, and declarations. Use the built-in tools to click into each field.

-

3.Before starting, gather necessary documents such as identification, income statements, employment verification letters, and asset details to complete the application accurately.

-

4.As you fill in the fields, ensure to input correct and detailed information about personal details, employment history, income, assets, and liabilities, following the form's prompts.

-

5.Regularly review your entries on pdfFiller to spot any errors or omissions. Use the preview feature to see how the completed form will look.

-

6.Finalize the form by adding necessary signatures for both the borrower and co-borrower using the electronic signature feature.

-

7.To save your work, click the save button, and choose to download the form as a PDF or submit it electronically as per your lender's requirements.

Who is eligible to use the Uniform Residential Loan Application?

The Uniform Residential Loan Application is designed for individuals applying for a mortgage loan, including both borrowers and co-borrowers. Applicants must provide personal details, income information, and assets.

What documents do I need to complete the application?

To complete the Uniform Residential Loan Application, you will need personal identification, proof of income, employment verification, and a detailed list of your assets and liabilities.

Can I fill out the application electronically?

Yes, you can fill out the Uniform Residential Loan Application electronically using pdfFiller. This allows for easy editing, saving, and uploading of completed forms.

What common mistakes should I avoid when filling out the form?

Common mistakes include providing incomplete information, entering incorrect details like Social Security numbers, or forgetting to sign the application. Review all fields before submitting.

How long does it take to process the application?

Processing times for the Uniform Residential Loan Application can vary, but typically it takes from a few days to several weeks, depending on the lender's requirements and workload.

How do I submit the completed application?

After completing the Uniform Residential Loan Application in pdfFiller, you can submit it directly through the platform or download it to send via email or postal service to your lender.

Are there any fees associated with applying for a loan using this form?

While the form itself may not have a fee, lenders might charge application fees or additional costs during the mortgage application process. Always check with your lender for specific details.

Freddie Mac 65 / Fannie Mae 1003 - Residential Form Versions

Related Content

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.