Add or replace text, adjust formatting, insert legally binding eSignatures, and send documents for signing without hopping between apps.

Get the free cg2010

Show details

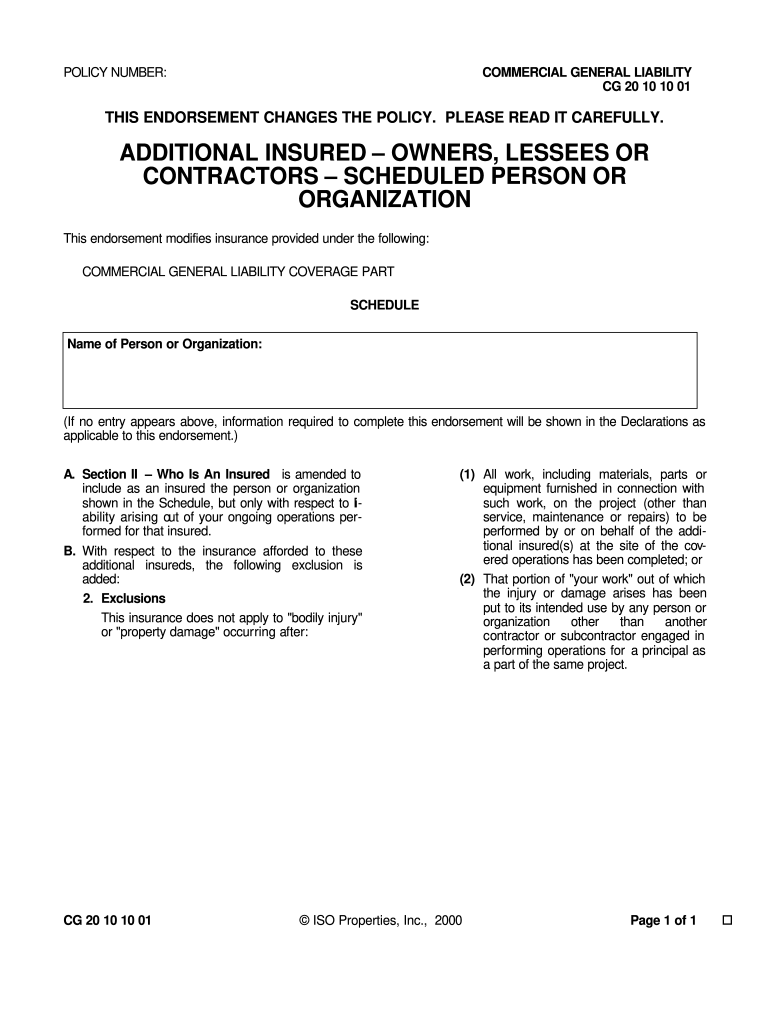

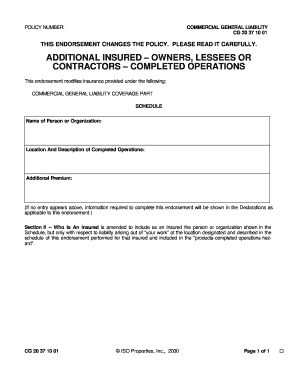

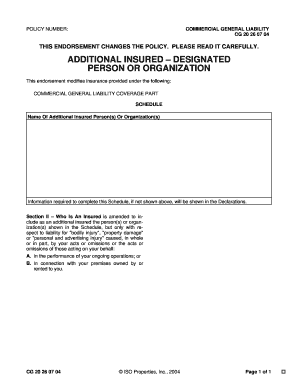

POLICY NUMBER: COMMERCIAL GENERAL LIABILITY CG 20 10 10 01 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. ADDITIONAL INSURED OWNERS, LESSEES OR CONTRACTORS SCHEDULED PERSON OR ORGANIZATION

We are not affiliated with any brand or entity on this form

Fill out, sign, and share forms from a single PDF platform

Manage all your documents quickly and securely in the cloud.

Edit and sign in one place

Create professional forms

Add and customize fillable fields to tailor each form to your needs and ensure easy completion without printing and scanning.

Simplify data collection

Quickly share forms via email or a secure link, enabling anyone to complete forms online in seconds, on any device.

Manage forms centrally

Keep all your forms and templates organized in one secure, cloud-based platform, track changes easily, and export documents in any format.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

Your Guide to CG 20 10 Form and Its Application

How do you understand the CG 20 10 endorsement?

The CG 20 10 endorsement, also known as the Additional Insured — Owners, Lessees, or Contractors — Scheduled Person or Organization endorsement, is a significant component of commercial general liability insurance. It allows a business to extend its insurance coverage to another entity, protecting them from claims made against the policyholder related to ongoing operations. Understanding its importance is crucial for contractors and subcontractors alike.

-

The CG 20 10 endorsement is vital for ensuring that all parties involved in a project are covered under the primary insurance policy, preventing costly legal battles.

-

Some key features include the ability to name specific additional insured parties and the assurance that the coverage extends only to liability arising out of the named insured’s operations.

-

This endorsement is typically utilized in construction and contracting scenarios, but can also be relevant in any situation where third-party entities are at risk.

What is the role of the CG 20 10 in commercial general liability?

Commercial general liability coverage is designed to protect businesses from potential lawsuits and damages that may arise during their operations. The CG 20 10 endorsement plays a crucial role in enhancing this coverage by providing additional protections. This is especially important for contractors and subcontractors who often work under the risk of exposure to liabilities that could impact their project and financial stability.

-

Commercial general liability coverage includes protection against injuries and damages to property that a business may be responsible for because of its operations or products.

-

This endorsement integrates seamlessly by ensuring that subcontractors are also protected, which can help subcontractors secure their own contracts.

-

For contractors, this endorsement helps in mitigating risks as they navigate complex project environments with multiple stakeholders.

How do you fill out the CG 20 10 form?

Filling out the CG 20 10 form requires careful attention to specific details to ensure that the documentation is accurate and legally compliant. It's crucial to understand which sections need to be filled entirely to avoid delays in obtaining coverage.

-

Sections such as named insured, additional insured parties, and effective dates must be included accurately.

-

Double-check all entries against policy requirements to prevent any miscommunication with involved parties.

-

Common errors to avoid include leaving out required information or incorrectly labeling additional insured parties.

How can you manage your CG 20 10 documentation with pdfFiller?

Managing CG 20 10 documentation can be streamlined through pdfFiller, which offers comprehensive features for document handling. Using pdfFiller allows users to create, edit, and sign PDF documents directly from its cloud-based platform.

-

pdfFiller simplifies the entire process, from drafting your CG 20 10 form to final execution.

-

It enhances collaboration among team members, allowing for simultaneous editing and feedback.

-

Version control in pdfFiller ensures that everyone has access to the latest version of the document.

What are some tips for insurance professionals handling CG 20 10?

For insurance professionals, navigating the questions surrounding the CG 20 10 endorsement can be overwhelming, yet essential for client satisfaction. By understanding the nuances of the endorsement, agents can provide their clients with the support they need.

-

Insurance agents should familiarize themselves with common questions to provide quick references.

-

Effectively communicating the benefits ensures clients understand what protection they are getting.

-

Developing a checklist allows agents to systematically guide clients through the necessary steps regarding the endorsement.

What are key takeaways about the CG 20 10 endorsement?

Understanding the CG 20 10 endorsement is essential for any individual involved in projects requiring additional insured status. Key takeaways should focus on the importance of comprehending your policy’s exclusions and ensuring that adequate coverage is maintained.

-

The CG 20 10 plays a pivotal role in real-world situations where risk management is critical.

-

Awareness of exclusions can prevent gaps in coverage, which can be detrimental during claims.

-

By utilizing CG 20 10, businesses can ensure adequate coverage during multi-party projects.

Frequently Asked Questions about cg 2010 form

What is a CG 20 10 form?

The CG 20 10 form is an endorsement that provides additional insured status to specified parties under a commercial general liability insurance policy. It is crucial in situations where multiple parties are involved in a project, ensuring they are protected.

Who needs a CG 20 10 endorsement?

Typically, contractors or subcontractors require a CG 20 10 endorsement to protect clients or other contractors from claims during a project's lifecycle. This is often a requirement in contract agreements.

How do I fill out the CG 20 10 form?

Filling out the CG 20 10 form involves identifying the named insured, specifying additional insured parties, and entering the effective date. It’s crucial to double-check all entries to ensure accuracy.

What are the benefits of using pdfFiller for managing CG 20 10 forms?

pdfFiller offers features like collaborative editing, eSigning, and real-time updates, making it easier to navigate through the CG 20 10 documentation process. This helps streamline approvals and enhances productivity.

How does the CG 20 10 endorsement interact with other endorsements?

The CG 20 10 endorsement can work alongside other endorsements, such as CG 20 37, which addresses liability in completed operations. Understanding these interactions is key to comprehensive coverage.

pdfFiller scores top ratings on review platforms

was under the impression it was free will i finished to first one. was not happy 20$ a month is too much only need this for school to do 4 files....

My experience is minimal. I have not had any problems.

People Also Ask about cg 2010 10 01

What does CG 2010 cover?

The CG 20 10 11 85 provides coverage for liability arising out of contractors work, and “your work” includes both the named insured's ongoing and completed operations.

What is the difference between cg2033 and CG2010?

The blanket additional insured that most resembles the CG 20 10 is the CG 20 33. A significant difference between the CG 20 10 and CG 20 33, is CG 20 33's requirement that there must be a written contract or agreement between the additional insured and the named insured.

Which edition of the CG 2010 CG 2033 or CG 2038 do you require in your contract?

The contract should require the CG2038 or the CG2010 with automatic blanket language for ongoing operations and CG2037 for completed operations, but should accept alternatives if they provide equivalent coverage.

What is the difference between CG 2010 and 2037?

CG2037 4/13 This endorsement contains the same limitations and conditions as the CG2010 EXCEPT that this endorsement insures the additional insured for completed operations of the contractor and not ongoing operations. This endorsement supplements the CG2010.

What is ISO form CG 20 10 11 85?

CG 20 10 (Edition 11/85): Addresses a coverage requirement that is frequently imposed by project owners on contractors doing work for them – “the contractor will provide the owner with additional insured status for claims against the owner arising out of completed work”.

What is CG 20 10 11 85?

In the November 1985 edition – called the CG 20 10 11 85 – the entity being added as an additional insured was only an insured “with respect to liability arising out of 'your work. '” The “your work” refers to the work of the named insured – that is, the contractor.

Related pages

Related Content cg2010 form

Related to cg2010 form

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.