Last updated on Apr 29, 2026

Get the free IRS Revenue Ruling 2004-107

We are not affiliated with any brand or entity on this form

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

What is IRS Revenue Ruling 2004-107

The IRS Revenue Ruling 2004-107 is a federal tax document used by taxpayers and tax professionals to understand inflation-adjusted amounts under § 1274A for qualified debt instruments and to address below-market loan treatments.

pdfFiller scores top ratings on review platforms

Who needs IRS Revenue Ruling 2004-107?

Explore how professionals across industries use pdfFiller.

IRS Revenue Ruling 2004-107 is needed by:

-

Taxpayers applying for below-market loans

-

Tax professionals advising clients on tax liabilities

-

Organizations offering qualified continuing care facilities

-

Individuals seeking to understand tax implications of loans

-

Accountants handling employment tax forms

-

Financial advisors guiding clients on tax planning

Comprehensive Guide to IRS Revenue Ruling 2004-107

What is IRS Revenue Ruling 2004-107?

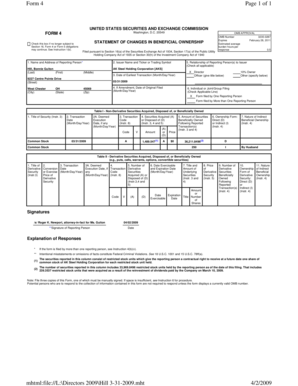

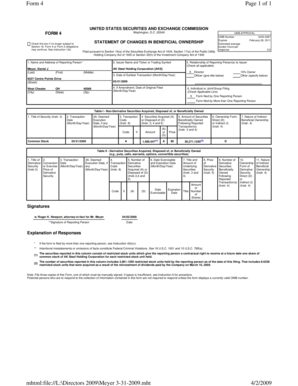

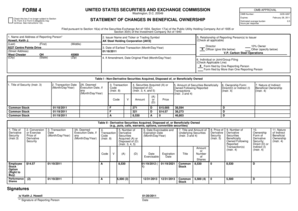

IRS Revenue Ruling 2004-107 serves a crucial role within the tax framework by addressing inflation-adjusted amounts specified under § 1274A. This ruling provides clarity on the treatment of below-market loans outlined in § 7872, which is essential for understanding how these loans interact with tax obligations. Taxpayers and financial professionals must be aware of the parameters that govern these adjustments.

Purpose and Benefits of IRS Revenue Ruling 2004-107

The significance of IRS Revenue Ruling 2004-107 stems from its ability to guide taxpayers and financial advisors in navigating complex tax regulations. By clarifying the treatment of below-market loans and detailing inflation-adjusted limits, it enables professionals to make informed decisions. Understanding these aspects can enhance financial planning and compliance for various stakeholders.

Key Features of IRS Revenue Ruling 2004-107

This ruling includes several critical elements and accompanying tables that summarize essential information. Among its key features is the relevance of qualified continuing care facilities in the context of loan treatment. These tables demonstrate the CPI adjustment loans and the treatment under § 7872, providing transparency for users.

Who Needs IRS Revenue Ruling 2004-107?

The target audience for IRS Revenue Ruling 2004-107 includes a diverse group of professionals and taxpayers. This encompasses financial advisors aiming to deliver expert guidance and accountants who must ensure compliance with tax laws. Understanding the nuances of this ruling will help various roles utilize the information effectively and apply it to their specific scenarios.

Eligibility Criteria and Related Documents for IRS Revenue Ruling 2004-107

Taxpayers or facilities wishing to benefit from IRS Revenue Ruling 2004-107 may face specific eligibility criteria. Key documents required for referencing or utilizing the ruling effectively include:

-

Proof of loan agreements

-

Tax returns for relevant years

-

Documentation of qualified continuing care facilities

-

Supporting materials for inflation adjustments

How to Access and Interpret IRS Revenue Ruling 2004-107 Online

Finding and interpreting IRS Revenue Ruling 2004-107 online can be accomplished through a simple process. Follow these steps to access the ruling:

-

Visit the official IRS website.

-

Navigate to the forms and publications section.

-

Search for IRS Revenue Ruling 2004-107 in the search bar.

-

Download or view the ruling to interpret the required information.

Common Errors and How to Avoid Them When Using IRS Revenue Ruling 2004-107

While working with IRS Revenue Ruling 2004-107, users may encounter common errors. To ensure accurate interpretation and application, consider these practical tips:

-

Double-check figures against the ruling's tables.

-

Consult tax professionals for complex scenarios.

-

Review eligibility criteria thoroughly.

-

Stay updated with any changes to tax regulations.

Using pdfFiller for IRS Revenue Ruling 2004-107

pdfFiller offers various features that facilitate the management of IRS Revenue Ruling 2004-107. Users can benefit from the following:

-

Edit and fill out forms easily.

-

E-sign documents securely.

-

Convert IRS documents for better accessibility.

-

Share completed forms without hassle.

Security and Compliance with IRS Revenue Ruling 2004-107 Documentation

Maintaining security is vital when handling documents related to IRS Revenue Ruling 2004-107. pdfFiller ensures compliance with regulations such as HIPAA and GDPR, employing robust security protocols that include 256-bit encryption. This commitment protects sensitive information throughout the documentation process.

Understanding Next Steps After IRS Revenue Ruling 2004-107 Submission

After implementing the provisions of IRS Revenue Ruling 2004-107 and submitting any associated forms, users should track their submissions diligently. Important next steps include:

-

Confirming receipt of submitted documents.

-

Monitoring for any feedback or requests for additional information.

-

Correcting errors promptly when identified.

How to fill out the IRS Revenue Ruling 2004-107

-

1.Access pdfFiller and search for 'IRS Revenue Ruling 2004-107' in the form library.

-

2.Open the form to edit by clicking on it in the search results.

-

3.Review the details about the form to understand what information you will need.

-

4.Prepare essential documents and data related to below-market loans and qualified debt instruments before starting.

-

5.Utilize the pdfFiller interface to fill in each section as required, clicking on text fields to enter your information.

-

6.Check that all necessary tables and inflation-adjusted amounts are properly filled based on the guidelines provided in the form.

-

7.Regularly save your progress through the pdfFiller platform to prevent data loss.

-

8.Once you have completed the form, conduct a thorough review to ensure all information is accurate and complete.

-

9.Finalize the form by following the instructions on pdfFiller for making edits or adjustments as necessary.

-

10.To save, download, or submit the completed form, use the options available in pdfFiller to export or share your document directly.

Who is eligible to use IRS Revenue Ruling 2004-107?

Taxpayers using qualified debt instruments or engaging in below-market loans are eligible to reference this ruling for their tax calculations and understanding.

What is the deadline for addressing tax implications related to this ruling?

While specific deadlines may vary, it's typically advisable to consider this ruling during tax preparation periods or prior to filing annual returns to ensure compliance.

How should the IRS Revenue Ruling 2004-107 be submitted?

This ruling itself is not submitted; it serves as guidance for taxpayers. Ensure that any relevant tax returns or documents reflect its implications if applicable.

What supporting documents are needed when applying this ruling?

Supporting documents may include financial statements, loan agreements, and records of the amounts being tagged under qualified debt instruments.

What are common mistakes to avoid with this ruling?

Common mistakes include failing to apply the correct inflation adjustments, misinterpreting below-market loan definitions, or not consulting qualified tax advisors for clarification.

How long does it take to process related tax forms?

Processing times vary widely based on submission methods and IRS workload, but it generally takes several weeks to a few months for standard processing.

Are there any fees associated with the use of IRS Revenue Ruling 2004-107?

There are no fees specifically for referencing this ruling. However, consulting tax professionals may incur consultation fees depending on their services.

Related Content

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.