Last updated on Apr 2, 2026

Get the free IRS Revenue Ruling 98-31

We are not affiliated with any brand or entity on this form

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

What is irs revenue ruling 98-31

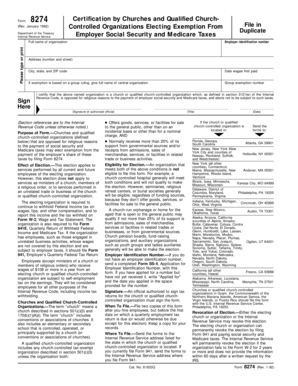

The IRS Revenue Ruling 98-31 is a tax document used by taxpayers to understand bond factor amounts for low-income housing credits under Section 42(j)(6) of the Internal Revenue Code.

pdfFiller scores top ratings on review platforms

Who needs irs revenue ruling 98-31?

Explore how professionals across industries use pdfFiller.

Irs revenue ruling 98-31 is needed by:

-

Taxpayers interested in low-income housing credits

-

Accountants preparing tax documents

-

Real estate developers seeking IRS guidance

-

Financial advisors advising clients on tax matters

-

Tax practitioners dealing with IRS documentation

-

Government agencies involved in tax regulation

Comprehensive Guide to irs revenue ruling 98-31

What is IRS Revenue Ruling 98-31?

IRS Revenue Ruling 98-31 serves as a significant document that provides taxpayer guidance on bond factor amounts under Section 42(j)(6) of the Internal Revenue Code. This revenue ruling highlights the importance of understanding the calculations for low-income housing projects and informs taxpayers about their obligations and options concerning those calculations.

The ruling aids in determining the amount of bond considered satisfactory by the Treasury Department during the applicable time frame. Thus, it holds critical relevance for those involved in low-income housing credit calculations.

Purpose and Benefits of IRS Revenue Ruling 98-31

The primary purpose of IRS Revenue Ruling 98-31 is to enhance taxpayers' understanding of bond factors associated with low-income housing credits. This clarity not only helps in compliance with Treasury Department guidance but also provides insight into how bond factor amounts are calculated under the Internal Revenue Code.

By utilizing this ruling, taxpayers can benefit from a more structured approach to their tax obligations, ensuring they adhere to the relevant laws and regulations while effectively managing their financial responsibilities.

Who Needs IRS Revenue Ruling 98-31?

IRS Revenue Ruling 98-31 is essential for various stakeholders in the low-income housing sector. Taxpayers involved in low-income housing projects will find this ruling particularly useful as it provides necessary guidance on bond factors.

Additionally, professionals such as tax advisors and accountants may require insights from this ruling to assist clients with compliance and financial planning related to low-income housing credits.

Eligibility Criteria for IRS Revenue Ruling 98-31

To effectively utilize IRS Revenue Ruling 98-31, certain eligibility criteria must be met. Primarily, it applies to qualified low-income buildings and taxpayers who are involved in low-income housing projects.

The Internal Revenue Code outlines specific conditions that these properties must satisfy to qualify for the bond factor amounts. Understanding these criteria is crucial for taxpayers seeking to apply the provisions of this ruling to their projects.

When to File or Submit IRS Revenue Ruling 98-31

Timelines for filing or submitting IRS Revenue Ruling 98-31 are essential for maintaining compliance. The guidance references a specific period: April through June of 1998, when submissions were required for bond factor calculations.

Failure to submit documentation on time can result in tax credit disqualifications. Therefore, knowing when to file IRS Revenue Ruling 98-31 is critical for taxpayers who wish to maximize their benefits from low-income housing credits.

How to Fill Out IRS Revenue Ruling 98-31 Online (Step-by-Step)

Filling out forms related to IRS Revenue Ruling 98-31 can be streamlined using pdfFiller. Here’s how to complete the process:

-

Access the IRS form 1998 through pdfFiller.

-

Gather all necessary factual information needed to fill out the sections accurately.

-

Input data into the relevant fields of the form.

-

Review the completed form to ensure accuracy.

-

Save and submit the form as required.

This step-by-step guide makes filling out IRS Revenue Ruling 98-31 straightforward and efficient.

Common Errors and How to Avoid Them

Taxpayers often encounter common errors when dealing with IRS Revenue Ruling 98-31. Frequent mistakes might include miscalculating bond factors or failing to adhere to submission timelines.

To mitigate such errors, taxpayers should implement strategies that involve double-checking their information and keeping thorough records before submission. Awareness of these common pitfalls can significantly enhance compliance and accuracy.

Submission Methods and Delivery for IRS Revenue Ruling 98-31

When it comes to submitting IRS Revenue Ruling 98-31, taxpayers have several options available. Electronic filing remains the preferred method due to its convenience and efficiency.

Users can track submissions and be aware of processing times, which is crucial for ensuring that their forms are received and handled appropriately. Choosing the right submission method is essential for a smooth filing experience.

Security and Compliance for IRS Revenue Ruling 98-31

Ensuring privacy and data protection while handling IRS Revenue Ruling 98-31 is critical for taxpayers. pdfFiller employs robust security features, including 256-bit encryption, to guarantee safe transactions and compliance with regulations such as HIPAA and GDPR.

Best practices for maintaining compliance include using secure methods for document handling and understanding the implications of sharing sensitive information.

Maximize Your Experience with pdfFiller

Using pdfFiller for IRS Revenue Ruling 98-31 can significantly enhance the user experience. The platform offers user-friendly features that streamline the editing and submitting processes for tax forms.

With capabilities such as digital signatures and top-notch document security, pdfFiller is an excellent option for those looking to handle their tax documentation efficiently and securely.

How to fill out the irs revenue ruling 98-31

-

1.To access the IRS Revenue Ruling 98-31, visit pdfFiller and use the search feature to locate the form by its name.

-

2.Once you find the form, click on it to open the document in the pdfFiller editor.

-

3.Before starting, gather necessary documents and data including prior IRS rulings, bond factor variables, and any applicable financial details.

-

4.Use the toolbar to navigate the form, which may include dropdowns for selections although it lacks fillable fields.

-

5.Carefully review any sections that relate to bond factor amounts and other relevant guidance provided in the ruling.

-

6.After inputting all necessary information and ensuring accuracy, go over the entire form for completeness.

-

7.To save your progress, click on the save icon. You can download the form as a PDF or save it directly into your pdfFiller account.

-

8.If you need to submit the form electronically, follow the provided steps in pdfFiller to submit the document to the IRS or relevant parties.

Who needs to reference IRS Revenue Ruling 98-31?

Taxpayers seeking clarity on bond factors for low-income housing credits should reference this ruling, along with accountants and tax practitioners who support clients in navigating tax regulations.

Is there a deadline for using the guidance in IRS Revenue Ruling 98-31?

While specific deadlines for applying the guidance in this ruling can vary based on transactions, it typically pertains to the 1998 tax year. Always check current IRS regulations for the most relevant deadlines.

What submission methods are available for related tax forms?

Taxpayers may submit associated forms electronically through platforms like pdfFiller or via mail. It’s important to follow the IRS guidelines for each specific form submission method.

Are there any common mistakes when using this ruling?

Common mistakes include miscalculating bond factors or misunderstanding the scope of the guidelines. Always double-check calculations and ensure all terms align with IRS expectations.

What documents do I need to provide along with IRS Revenue Ruling 98-31?

While this document itself does not require attachments, having supporting documents such as financial statements, prior IRS instructions, and property information ready can facilitate the process when compiling tax forms.

What is the processing time for tax forms associated with this ruling?

Processing times can vary based on the IRS's backlog, but taxpayers typically can expect a response within a few weeks to a couple of months for various filings made in relation to low-income housing credits.

How can I ensure I am eligible for the low-income housing credit?

Eligibility criteria for the low-income housing credit generally include maintaining the income of tenants below certain levels and ensuring compliance with Section 42 of the Internal Revenue Code. Consult the IRS guidelines for detailed eligibility requirements.

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.