Last updated on Mar 11, 2016

Get the free Authorization to Run Credit on Non-Borrowing Spouse

We are not affiliated with any brand or entity on this form

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

What is Non-Borrowing Spouse Credit Authorization

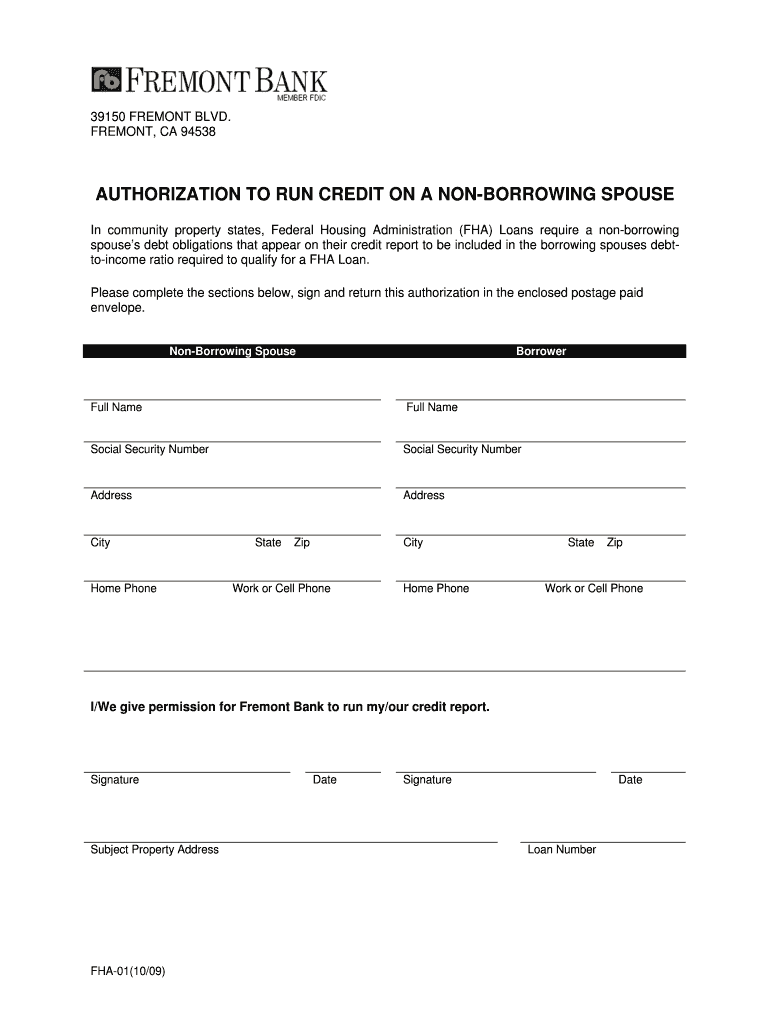

The Authorization to Run Credit on Non-Borrowing Spouse is a document used by borrowers in community property states to authorize credit checks on their non-borrowing spouses for FHA loan applications.

pdfFiller scores top ratings on review platforms

Who needs Non-Borrowing Spouse Credit Authorization?

Explore how professionals across industries use pdfFiller.

Non-Borrowing Spouse Credit Authorization is needed by:

-

Borrowers applying for FHA loans

-

Non-borrowing spouses in community property states

-

Real estate agents assisting clients

-

Lenders processing FHA loans

-

Financial advisors guiding clients through mortgage applications

Comprehensive Guide to Non-Borrowing Spouse Credit Authorization

What is the Authorization to Run Credit on Non-Borrowing Spouse?

The Authorization to Run Credit on Non-Borrowing Spouse form serves a vital purpose in community property states, particularly when securing FHA loans. In such states, this document allows lenders to assess the creditworthiness of both spouses, ensuring a comprehensive evaluation of the borrowing spouse's debt-to-income ratio. The role it plays is significant, as it impacts both the borrowing and non-borrowing spouse's financial profiles during the loan approval process.

This form ensures that lenders have the necessary information to make informed decisions regarding loan eligibility and terms, which is essential for couples navigating the complexities of shared financial responsibilities.

Purpose and Benefits of the Authorization to Run Credit on Non-Borrowing Spouse

This authorization is particularly critical in community property states like California, where marital property laws influence credit assessments. By authorizing lenders to run credit on a non-borrowing spouse, the borrowers can achieve more accurate debt-to-income ratio calculations. This practice smooths loan processing and facilitates faster approvals.

Additionally, having both spouses' credit considerations can prevent potential issues during underwriting, ensuring that all relevant financial information is taken into account. Ultimately, this enhances the chances of securing a favorable loan for the couple.

Who Needs the Authorization to Run Credit on Non-Borrowing Spouse?

The target audience for the authorization includes couples where one spouse is not formally listed as a borrower but whose credit significantly impacts the approval process. This situation commonly arises in community property states where each spouse’s credit profile is considered in determining loan eligibility.

Understanding these implications is crucial for both spouses. The non-borrowing spouse's credit can affect overall loan terms and approval status, making it essential for them to authorize a credit check as part of the lending process.

How to Fill Out the Authorization to Run Credit on Non-Borrowing Spouse (Step-by-Step)

-

Begin by entering your full name and the non-borrowing spouse’s details in the provided fields.

-

Complete all required personal information, including Social Security numbers and contact information.

-

Ensure both spouses sign and date the form in the designated areas.

-

Review the completed form for accuracy before submission.

Common pitfalls include skipping signature sections or failing to provide complete contact information, so be diligent in reviewing all fields to ensure a smooth submission process.

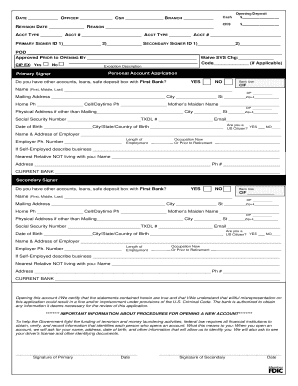

Field-by-Field Instructions for Completing the Form

Each field on the Authorization to Run Credit form must be filled out accurately to prevent delays in processing. Start with the 'Full Name' field, followed by 'Social Security Number', 'Address', and 'Home Phone'. The 'Work or Cell Phone' section should also be completed to ensure reliable communication.

Pay specific attention to the 'Signature' and 'Date' fields, as both spouses must sign for the authorization to be valid. Providing accurate information in these fields is critical for the lender's assessment.

Common Errors When Submitting the Authorization to Run Credit on Non-Borrowing Spouse

Users often make mistakes like omitting necessary information or providing incorrect details. Common errors include inaccurate Social Security numbers or missing signatures. To avoid these issues, double-check all fields before submission.

If errors are discovered after submission, contact the lender immediately for correction procedures to minimize delays in the loan process.

Submission Methods for the Authorization to Run Credit on Non-Borrowing Spouse

There are several methods for submitting the completed authorization form to lenders. Options typically include in-person delivery, email submission, or secure online upload through the lender's website.

Check with the lender for specific submission instructions, as they may have preferred formats or protocols to follow, ensuring that the document is received correctly and promptly.

What Happens After You Submit the Authorization to Run Credit on Non-Borrowing Spouse?

Once the authorization form is submitted, the couple can expect a processing timeline that varies by lender. It is advisable to maintain communication with the lender for updates regarding the status of the submission and any further steps needed.

Keeping track of the submission status is essential, as it allows the borrowers to address any issues that may arise quickly.

Security and Compliance When Handling the Authorization to Run Credit on Non-Borrowing Spouse

Handling sensitive documents requires stringent data protection measures. It is essential to comply with legal standards to ensure that personal information remains secure throughout the loan process.

Leading platforms like pdfFiller utilize advanced security measures, including 256-bit encryption and compliance with SOC 2 Type II, HIPAA, and GDPR standards, to safeguard personal data.

Experience the Ease of Filling Out Your Authorization to Run Credit on Non-Borrowing Spouse with pdfFiller

Using pdfFiller can enhance your form completion experience. The platform offers features such as online editing, eSigning, and secure storage, making the process seamless.

With its cloud-based PDF management capabilities and user-friendly interface, pdfFiller simplifies the filing of crucial documents, ensuring a stress-free experience for its users.

How to fill out the Non-Borrowing Spouse Credit Authorization

-

1.To access the form, navigate to the pdfFiller website and use the search bar to enter 'Authorization to Run Credit on Non-Borrowing Spouse'. Select the relevant form from the results.

-

2.Once the form is open, familiarize yourself with the sections before starting to fill it out. Ensure you have the required information ready, including full name, Social Security Number, addresses, and contact numbers for both parties.

-

3.Click on the text fields to enter the required information for both the non-borrowing spouse and the borrower. Make sure to input the data accurately in each respective field.

-

4.Ensure that the information entered reflects what is required by the form, including correct spellings and numeric data. Take your time to avoid typos and inaccuracies.

-

5.Once you have filled in all the required fields, review the form thoroughly to ensure that everything is correct. Check that all sections are completed, especially the signature and date fields.

-

6.If you need to make changes, use the editing tools provided by pdfFiller to adjust any incorrect information before finalizing.

-

7.After ensuring all data is correct, you can save the document by clicking the 'Save' option. To download the form, select 'Download' and choose your preferred file format.

-

8.Finally, if you need to submit the form, utilize the 'Submit' option available on pdfFiller, or print it out for physical submission as necessary.

Who is eligible to use the Authorization to Run Credit on Non-Borrowing Spouse?

Any borrower in California seeking an FHA loan can use this form if their spouse is a non-borrowing spouse. Both parties must provide their personal information and signatures.

Are there any deadlines for submitting this authorization form?

Typically, this form should be submitted as soon as possible during the loan application process. Check with your lender for any specific deadlines related to your FHA loan application.

How do I submit the completed authorization form?

You can submit the completed form electronically through pdfFiller, or print it out and deliver it to your lender directly. Ensure that signatures are included before submission.

What supporting documents do I need to provide with this form?

Generally, you will need personal identification documents and potentially financial statements. Verify with your lender if additional documentation is required for your specific situation.

What are common mistakes to avoid when filling out this form?

Ensure all information is complete and accurate, particularly the non-borrowing spouse's details. Avoid leaving any required fields blank and double-check signatures and dates.

How long does it take to process this authorization form?

Processing times may vary depending on the lender's timeline, but typically, it can take a few days to a week. Contact your lender for more specific timeframes.

What should I do if I made a mistake on the form?

If you notice a mistake after filling out the form, you can edit the information in pdfFiller or print a new copy and start again. Ensure all details are correct before final submission.

Related Forms

Get the latest insights from our blog

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.