Last updated on Apr 14, 2026

Get the free IRS Catch-Up Contribution Rules

We are not affiliated with any brand or entity on this form

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

What is irs catch-up contribution rules

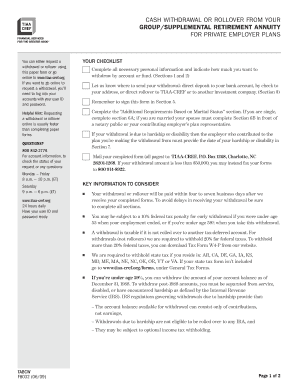

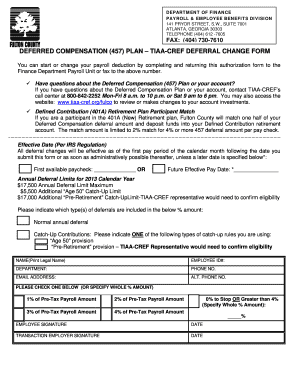

The IRS Catch-Up Contribution Rules is a tax document used by retirement plan sponsors to outline the rules for catch-up contributions to 401(k), 403(b), and governmental section 457 plans.

pdfFiller scores top ratings on review platforms

Who needs irs catch-up contribution rules?

Explore how professionals across industries use pdfFiller.

Irs catch-up contribution rules is needed by:

-

Retirement plan sponsors

-

Financial advisors

-

Tax professionals

-

Employees over 50

-

Individuals contributing to retirement plans

-

Human resources departments

Comprehensive Guide to irs catch-up contribution rules

What are the IRS Catch-Up Contribution Rules?

The IRS Catch-Up Contribution Rules are essential for enhancing retirement savings for individuals aged 50 and older. These rules allow participants in retirement plans, including 401(k), 403(b), and section 457 plans, to contribute additional funds beyond standard contribution limits. Established after December 31, 2003, these rules are vital for maximizing contributions, helping plan participants to secure their financial futures. Understanding these rules can significantly benefit employees by expanding their retirement savings options.

Purpose and Benefits of the IRS Catch-Up Contribution Rules

Utilizing the IRS Catch-Up Contribution Rules provides several advantages for retirement planning. For individuals aged 50 and older, these contributions can offer substantial financial benefits including enhanced savings potential. Additionally, there are considerable tax advantages associated with these contributions. Plan sponsors are encouraged to adopt these rules to ensure participants can take full advantage of the increased limits, promoting better financial health and retirement readiness for their employees.

Eligibility Criteria for IRS Catch-Up Contributions

To qualify for IRS catch-up contributions, individuals must meet specific eligibility criteria. Primary requirements include being at least 50 years old and having appropriate service in the plan. Additionally, the concept of 'universal availability' is vital, meaning that all eligible participants in a plan can make these contributions. Eligibility impacts the amount individuals can contribute to various plans such as 401(k), 403(b), and governmental section 457 plans, enabling them to maximize their retirement savings.

How to Fill Out the IRS Catch-Up Contribution Form Online

Filling out the IRS Catch-Up Contribution form online using pdfFiller is a straightforward process. Follow these steps:

-

Access the form through pdfFiller's platform.

-

Edit the document using the available tools to fill in the necessary fields accurately.

-

Ensure thoroughness in your entries to comply with IRS requirements.

Taking the time to understand the form and using pdfFiller's editing tools can enhance the clarity and accuracy of your submissions.

Common Errors and How to Avoid Them When Completing the Form

Several common errors can occur during the completion of the IRS Catch-Up Contribution form. These include:

-

Incorrect contribution amounts.

-

Missing signatures or dates.

To prevent these issues, double-check your entries and utilize validation tools provided within the pdfFiller platform. Thorough reviews before submission are essential to ensure compliance and avoid potential rejections.

Submission Methods and What Happens After You Submit

Once the form is completed, it can be submitted through various methods. Options include:

-

Electronic submission via the pdfFiller platform.

-

Physical submission by mail.

After submitting, you will receive confirmation of your submission, which is vital for tracking your application. Understanding processing timelines can help manage expectations regarding approval and subsequent actions.

Security and Compliance Considerations

When handling IRS documents, security and compliance are paramount. pdfFiller implements robust security measures, including 256-bit encryption, to protect sensitive information. Furthermore, the platform complies with regulations such as HIPAA and GDPR, ensuring data protection throughout the document handling process. Prioritizing security is crucial when dealing with financial documentation to safeguard personal and financial data.

Post-Submission: How to Correct or Amend Your IRS Catch-Up Contribution Form

If corrections are necessary after submitting your form, follow these procedures:

-

Identify the specific errors that need amending.

-

Complete any required forms to correct these errors.

Common reasons for rejections typically include incomplete submissions or inaccuracies in reported amounts. Maintaining a record of your submissions is important for future reference and potential follow-ups.

Harness the Power of pdfFiller for Your IRS Catch-Up Contribution Form

pdfFiller simplifies the process of managing IRS forms with several key features. Users can benefit from:

-

eSigning capabilities for quick approval.

-

Secure cloud storage for easy access.

-

Edit and customize forms as needed.

Utilizing pdfFiller ensures a seamless experience while ensuring compliance and security when filling out essential IRS documentation.

How to fill out the irs catch-up contribution rules

-

1.To access the IRS Catch-Up Contribution Rules form on pdfFiller, go to the pdfFiller website and use the search bar to find the specific form by its name or relevant category.

-

2.Once you locate the form, click on it to open it in the pdfFiller editor. Familiarize yourself with the interface, which allows you to navigate easily through the document.

-

3.Before filling out the form, gather all necessary information such as plan details, contribution limits, and eligibility criteria relevant to catch-up contributions after 2003.

-

4.Begin entering data in the designated fields. Use the pdfFiller tools to type or select options, and remember to save changes frequently to avoid loss of information.

-

5.Review all entered information for accuracy, ensuring all eligibility criteria and limits are correctly reflected in your inputs. Use the preview feature for a final check.

-

6.After completing the form, finalize your edits and select the option to save the document. Consider downloading it for your records or to submit later through appropriate channels.

-

7.If required, submit the completed form according to your plan's guidelines, whether electronically through pdfFiller or by printing and mailing it to the appropriate address.

What are the eligibility requirements for making catch-up contributions?

To make catch-up contributions, you must be aged 50 or older by the end of the calendar year. Additionally, you must be enrolled in a 401(k), 403(b), or governmental section 457 plan that allows for catch-up contributions.

What is the deadline for making catch-up contributions?

Catch-up contributions must be made before the end of the calendar year in which you turn 50. For contributions applicable to prior years, ensure they comply with the relevant tax year limits.

How can I submit my completed form?

Once you complete the IRS Catch-Up Contribution Rules form on pdfFiller, you can submit it electronically if your plan allows. Alternatively, download it and mail it directly to your plan administrator.

What documents do I need to support my catch-up contributions?

While specific documentation may vary, generally, you should maintain records of your age, contributions made, and any plan-specific requirements outlined in the IRS rules to validate your submissions.

What are common mistakes to avoid when filling out this form?

Common mistakes include failing to check eligibility before submitting catch-up contributions and miscalculating the amount, which may lead to compliance issues or penalties. Always review your form before submission.

How long does it take to process catch-up contributions?

Processing times for catch-up contributions may vary by plan. Typically, processing can take a few days to several weeks, particularly if additional documentation is needed for verification.

What if my plan doesn’t allow catch-up contributions?

If your retirement plan does not permit catch-up contributions, you may want to discuss alternative savings options with your plan administrator or consider other retirement accounts that may allow higher contributions.

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.