CA FTB 3805V 2015 free printable template

Show details

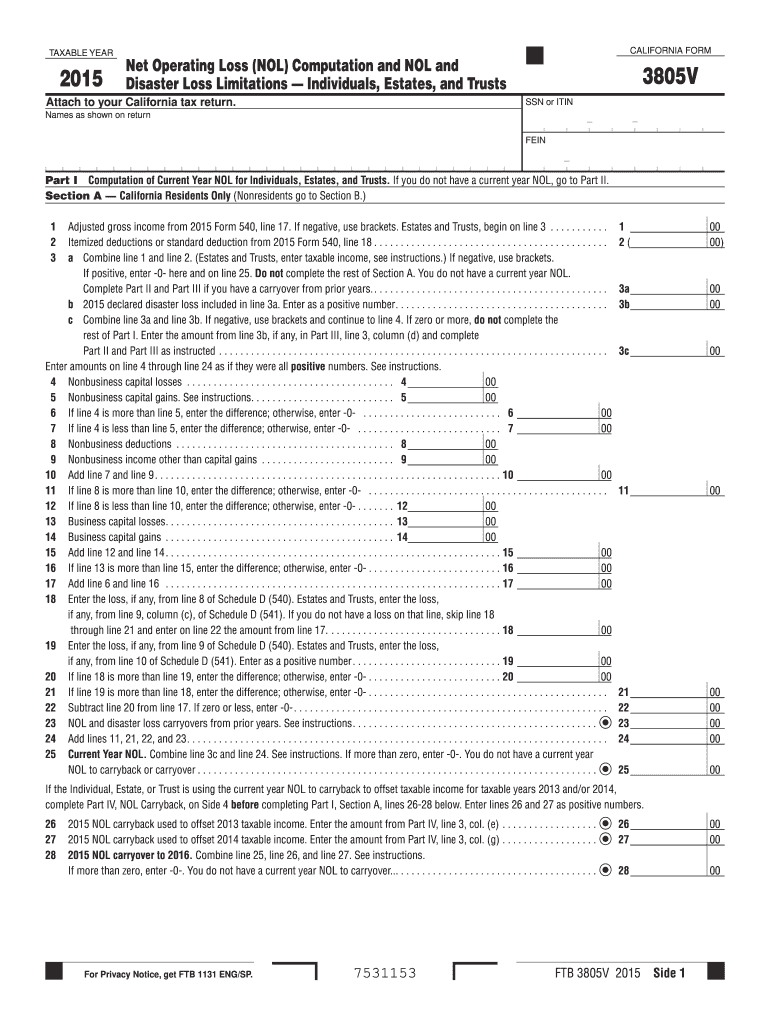

28 For Privacy Notice get FTB 1131 ENG/SP. 7531153 FTB 3805V 2015 Side 1 Section B Nonresidents and Part-Year Residents Only Computation of Current Year California NOL a Enter total amounts as if you were a CA resident for entire year. TAXABLE YEAR CALIFORNIA FORM Net Operating Loss NOL Computation and NOL and Disaster Loss Limitations Individuals Estates and Trusts Attach to your California tax return. 3805V SSN or ITIN Names as shown on return - FEIN Part I Computation of Current Year...

pdfFiller is not affiliated with any government organization

Get, Create, Make and Sign CA FTB 3805V

Edit your CA FTB 3805V form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your CA FTB 3805V form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit CA FTB 3805V online

Follow the guidelines below to benefit from the PDF editor's expertise:

1

Log into your account. If you don't have a profile yet, click Start Free Trial and sign up for one.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit CA FTB 3805V. Rearrange and rotate pages, add new and changed texts, add new objects, and use other useful tools. When you're done, click Done. You can use the Documents tab to merge, split, lock, or unlock your files.

4

Save your file. Select it in the list of your records. Then, move the cursor to the right toolbar and choose one of the available exporting methods: save it in multiple formats, download it as a PDF, send it by email, or store it in the cloud.

The use of pdfFiller makes dealing with documents straightforward. Now is the time to try it!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

CA FTB 3805V Form Versions

Version

Form Popularity

Fillable & printabley

How to fill out CA FTB 3805V

How to fill out CA FTB 3805V

01

Obtain a copy of form CA FTB 3805V from the California Franchise Tax Board website or other sources.

02

Fill in your personal information, including your name, Social Security number, and address in the designated fields.

03

Indicate the tax year for which you are filing the form.

04

Provide information regarding your tax liability, including the amounts from your income and deductions.

05

Complete any necessary schedules or sections related to credits and adjustments.

06

Calculate the total amount credited or owed as indicated in the form's instructions.

07

Review the form for accuracy and completeness.

08

Sign and date the form, and include any additional documentation as required.

09

Submit the form to the address specified in the instructions, either by mail or electronically if applicable.

Who needs CA FTB 3805V?

01

Individuals who have a qualified solar energy system installed and are claiming the solar energy system property tax exclusion.

02

Taxpayers looking to claim a credit for taxes paid on solar energy system installations.

Instructions and Help about CA FTB 3805V

The following information is provided for educational purposes only and in no way constitutes legal, tax, or financial advice. For legal, tax, or financial advice specific to your business needs, we encourage you to consult with a licensed attorney and×or CPA in your State. The following information is copyright protected. No part of this lesson may be redistributed, copied, modified or adapted without prior written consent of the author. California has a number of ongoing requirements for your LLC to remain in compliance with the State. The first of these is the Statement of Information which we discussed in a prior lesson. Remember your first Statement of Information is due within 90 days of the approval of your LLC. Then, you'll need to file it again every two years. It will be due by the anniversary date of the approval of your LLC. If you have not watched this lesson yet, please do so now. The next requirement is the Annual LLC Franchise Tax of $800. California charges an $800 Annual LLC Franchise Tax on LCS. This tax is due by all LCS regardless of income or the business activity. This is a “prepay tax”, meaning that it pays for the current year. Your first $800 payment for the LLC Franchise Tax is due by 15th day of the 4th month after your LLC is filed. The month your LLC is filed counts as Month 1, regardless if you file on the 1st of the month, the last of the month, or any day of the month, really. This means that if you were to file your LLC on March 22nd, then you must pay the $800 fee no later than June 15th (in this example, March is Month 1, April is Month 2, May is Month 3, and June is Month 4×. Then, every year after your first payment $800 LLC Franchise Tax will be due by April 15th. You pay the $800 LLC Franchise Tax using Form 3522 called the LLC Tax Voucher. We've included this form below in the download section, so that you can see it and get familiar with it. Failure to file before the deadline will result in the State charging late fees and penalties, and they will eventually dissolve your LLC if you do not pay the $800 Annual LLC Franchise Tax. This is not a popular requirement for California, but it is mandatory, and it is the cost of doing business in the State. There's no way to get around this tax. If you want to form an LLC in California, you have to pay this $800 tax within 4 months after you file your LLC and then again by April 15th of each year. Next is Form 3536, the Estimated Fee for LCS. In addition to filing and paying the $800 Annual LLC Franchise Tax, you'll also have to file a return called Form 3536, Estimated Fee for LCS, and pay an additional fee only if your LLC will make $250,000 or more during the tax year. The more you make, the higher the fee. For example, again if you're under $250,000 you don't have to pay this additional fee, but if you're between $250,000 — $500,000, the fee is $900. Between $500,000 and a million it’s ×2,500, etcetera as you can look at the table there. Again, the fees above...

Fill

form

: Try Risk Free

People Also Ask about

How are capital gains taxed for non residents?

A flat tax of 30 percent is imposed on U.S. source capital gains in the hands of nonresident alien individuals physically present in the United States for 183 days or more during the taxable year. This 183-day rule bears no relation to the 183-day rule under the substantial presence test of IRC section 7701(b)(3).

Do I have to pay California income tax if I live out of state?

As a nonresident, you pay tax on your taxable income from California sources. Sourced income includes, but is not limited to: Services performed in California. Rent from real property located in California.

Does California allow corporate NOL carryback?

Effective for tax years beginning on or after January 1, 2013, California allows taxpayers to carryback current year net operating losses.

Does California allow NOL carryover?

Overview. If your deductions and losses are greater than your income from all sources in a tax year, you may have a net operating loss (NOL). You may be able to claim your loss as an NOL deduction. This deduction can be carried back to the past 2 years and/or you can carry it forward to future tax years.

When did CA suspend NOLs?

In 2020, the California Legislature suspended the use of NOLs and capped business tax credit usage at $5 million for tax years 2020, 2021, and 2022 to combat projected budget deficits resulting from the COVID-19 pandemic.

How do I avoid capital gains tax in California?

You do not have to report the sale of your home if all of the following apply: Your gain from the sale was less than $250,000. You have not used the exclusion in the last 2 years. You owned and occupied the home for at least 2 years.

Does California conform to NOL carryback?

Federal vs. California Your California NOL is generally calculated the same as the Federal. However, allowable amounts and the carryback/carryforward periods differ between Federal and California.

What can I do with money to avoid capital gains tax?

To limit capital gains taxes, you can invest for the long-term, use tax-advantaged retirement accounts, and offset capital gains with capital losses.

Does CA conform to 461 L?

Excess Business Loss Limitation – The federal CARES Act made amendments to IRC Section 461(l) by eliminating the excess business loss limitation of noncorporate taxpayers for taxable year 2020 and retroactively removing the limitation for taxable years 2018 and 2019. California does not conform to those amendments.

What is the excess business loss limitation?

The EBL limitation applies to noncorporate taxpayers, such as individuals, trusts and estates, and does not allow a “business” loss to exceed $270,000 for single filers or $540,000 for married joint filers for the tax year 2022, indexed annually.

Are capital gains taxable on 1040NR?

Taxable capital gains may be subject to reduced tax rate under tax treaty agreements. If you are in receipt of capital gains income, you must report the gains on Form 1040NR.

How long can a NOL be carried forward in California?

In California, the standard rule for NOL carryovers is that they can be carried forward for 10 years2 following the loss year for losses generated in 2000 through 2007 and for 20 years following the loss year for losses generated in 2008 and forward.

How can you avoid paying taxes on capital gains?

How to Minimize or Avoid Capital Gains Tax Invest for the long term. Take advantage of tax-deferred retirement plans. Use capital losses to offset gains. Watch your holding periods. Pick your cost basis.

What is the tax rate for non-resident?

This income is taxed at a flat 30% rate unless a tax treaty specifies a lower rate. Nonresident aliens must file and pay any tax due using Form 1040NR, U.S. Nonresident Alien Income Tax Return.

How much tax do you pay on capital gains in California?

The capital gains tax rate is in line with normal California income tax laws (1%-13.3%). These California capital gains tax rates can be lower than the federal capital gains tax rates, which are 0%, 15%, and 20% for long-term gains (assets held for more than a year).

Does CA conform to excess business interest expense?

Limitation on deduction of business interest – Under federal law, every business, regardless of its form, is generally subject to a disallowance of a deduction for net interest expense in excess of 50% of the business's adjustable taxable income. California does not conform.

Do non residents pay capital gains tax in California?

If you are a nonresident and exchange real or tangible property located within California for real or tangible property located outside California, the realized gain or loss will be sourced to California. Taxation will not occur until the gain or loss is recognized.

How are non residents of Canada taxed?

Canadian financial institutions and other payers have to withhold non-resident tax at a rate of 25% on certain types of Canadian-source income they pay or credit to you as a non-resident of Canada. The most common types of income that could be subject to non-resident withholding tax include: interest. dividends.

Are CA NOLs limited to 80%?

116-136, in 2020 significantly changed the historic treatment of net operating losses (NOLs) for federal income tax purposes. The TCJA provisions, specifically, limit allowable NOL deductions to 80% of federal taxable income and lift the previously imposed 20-year limitation on carryovers.

Does California conform to excess business loss limitation?

Taxpayers can not deduct an excess business loss in the current year. However, for California purposes, the excess business loss will be treated as an excess business loss carryover instead of an NOL carryover for the subsequent taxable year.

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

Where do I find CA FTB 3805V?

The pdfFiller premium subscription gives you access to a large library of fillable forms (over 25 million fillable templates) that you can download, fill out, print, and sign. In the library, you'll have no problem discovering state-specific CA FTB 3805V and other forms. Find the template you want and tweak it with powerful editing tools.

How can I fill out CA FTB 3805V on an iOS device?

Install the pdfFiller app on your iOS device to fill out papers. Create an account or log in if you already have one. After registering, upload your CA FTB 3805V. You may now use pdfFiller's advanced features like adding fillable fields and eSigning documents from any device, anywhere.

How do I fill out CA FTB 3805V on an Android device?

Complete CA FTB 3805V and other documents on your Android device with the pdfFiller app. The software allows you to modify information, eSign, annotate, and share files. You may view your papers from anywhere with an internet connection.

What is CA FTB 3805V?

CA FTB 3805V is a form used by individuals in California to claim a credit for taxes paid to other states.

Who is required to file CA FTB 3805V?

Taxpayers who have income from other states and have paid taxes to those states may be required to file CA FTB 3805V.

How to fill out CA FTB 3805V?

To fill out CA FTB 3805V, taxpayers must provide their personal information, details of taxes paid to other states, and any relevant income information.

What is the purpose of CA FTB 3805V?

The purpose of CA FTB 3805V is to allow taxpayers to receive a credit on their California tax return for taxes paid to other states, thus avoiding double taxation.

What information must be reported on CA FTB 3805V?

Information that must be reported on CA FTB 3805V includes the other state's tax paid, the type of income earned in that state, and the amounts of tax credits claimed.

Fill out your CA FTB 3805V online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

CA FTB 3805v is not the form you're looking for?Search for another form here.

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.