Amendments to the Rule 1003 Form: A Comprehensive Guide

Understanding the Rule 1003 Form

The Rule 1003 Form, officially known as the Uniform Residential Loan Application, is a pivotal document in the mortgage application process. It serves as a standardized means for borrowers to provide essential information to lenders, helping to streamline the approval process. Given its significance, the accuracy and completeness of the data submitted cannot be overstated. A single error can lead to delays or even denial of the loan.

Key components of the Rule 1003 Form include sections such as Borrower Information, Employment and Income, Loan and Property Information, and Disclosure Information. Each section is designed to capture specific details required by lenders. However, common pitfalls in filling out the form include skipping required fields, misrepresenting income, and incomplete disclosures.

Recent amendments to the Rule 1003 Form

Recent amendments to the Rule 1003 Form include several key changes aimed at enhancing clarity and compliance. These amendments are designed to improve both borrower and lender experiences alongside regulatory adherence. The alterations encompass new fields, modified questions, and revised instructions meant to standardize the form better and capture increasingly relevant information.

Introduction of additional borrower demographic questions to enhance data collection for fair lending compliance.

Refinements in income documentation requirements to reflect current income verification practices.

Expansion of language options for clearer understanding by non-English speaking borrowers.

The rationale behind these amendments is twofold: addressing regulatory motivations and industry feedback. Regulatory bodies have pushed for more detailed data collection to mitigate risks and increase transparency within the lending process. This, in turn, promotes better compliance standards while enhancing the overall user experience.

Navigating the amendments: Step-by-step guide

Preparing to fill out the revised Rule 1003 Form requires careful organization of documentation and relevant information. As a borrower or loan officer, having the necessary documents at hand will save time and reduce frustration. Key documents include proof of income, tax returns, asset statements, and personal identification.

Gather recent pay stubs and tax returns.

Prepare bank statements showing assets.

Collect identification documents such as a driver's license or passport.

When filling out the form, pay close attention to the amendments as they affect various sections directly. For instance, the Borrower Information section now includes optional demographic questions aimed at supporting fair lending efforts. In the Employment and Income Section, verify that income calculations align with the revised guidelines concerning multiple sources of income or self-employment.

Practical tools and resources

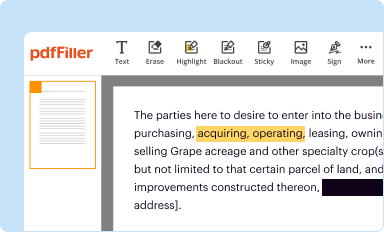

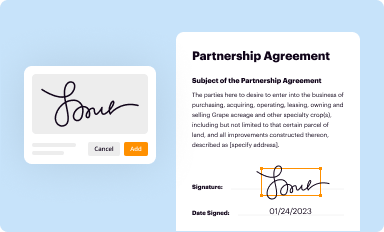

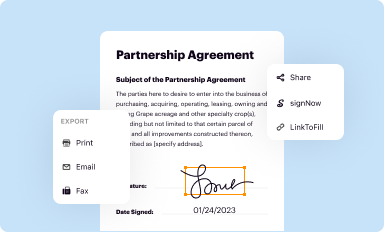

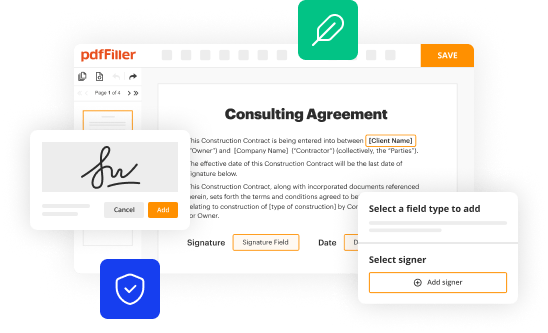

Using online tools for editing and signing the Rule 1003 Form can greatly enhance the experience. Platforms like pdfFiller facilitate efficient form management, allowing for easy edits, electronic signatures, and cloud storage. This ensures that all collaborators have the same access to the latest version of the form, significantly streamlining communication.

pdfFiller enables users to easily fill out and edit PDF forms without printing.

Cloud-based platforms provide security and easy access anytime from anywhere.

Interactive templates simplify the process while ensuring all required fields are addressed.

Moreover, utilizing eSignature capabilities on platforms like pdfFiller enhances efficiency. It allows borrowers to sign forms remotely, eliminating delays in obtaining necessary signatures.

FAQs about amendments to Rule 1003 form

The introduction of the amendments can raise numerous questions among users. A common inquiry is whether these amendments will affect a mortgage application timeline. Generally, while the alterations aim to streamline processes, borrowers should be prepared for possible delays if their previous submissions don’t align with the updated form.

How do the amendments affect my mortgage application timeline?

What should I do if I filled out an older version of the form?

Experts recommend that borrowers familiarize themselves with the changes. If you've already submitted an outdated version, contact your lender for guidance on whether a resubmission is necessary.

Collaborating with your team on form updates

When working as a team on Rule 1003 submissions, implementing a collaborative workflow is critical. Platforms like pdfFiller offer features that allow multiple team members to view, edit, and comment on forms in real time, ensuring everyone is aligned throughout the process. This approach reduces the risk of errors and miscommunication.

Set clear roles and responsibilities in the document preparation process.

Use version control features to track changes and updates effectively.

Implement secure sharing measures to protect sensitive borrower information.

When sharing documents, it's crucial to maintain privacy and confidentiality. Encrypting sensitive information and using password-protected access can help safeguard personal data.

Understanding the broader impact of amendments

The recent amendments to the Rule 1003 Form carry significant implications for the mortgage industry. By adjusting how lenders gather and process information, these changes can enhance lending practices and promote equitable access to credit for all borrowers. With a greater focus on data collection, lenders may see improvements in compliance standards, which can further establish trust within the industry.

How changes to the Rule 1003 Form influence lending practices.

Anticipated trends in document management and compliance.

Future trends are likely to introduce more innovations in document management, leveraging technology to simplify and enhance user experiences during the mortgage application process.

Related document changes and updates

In addition to the Rule 1003 Form, several related forms have also seen amendments. For instance, the 4506-T form, which allows lenders to request tax return information, and the Loan Estimate form, which details the costs associated with a mortgage, may have altered fields to ensure consistency across all documents. Understanding these connections is crucial as they interact seamlessly with the Rule 1003 Form.

Connection to forms such as the 4506-T and how they interact with the Rule 1003 Form.

Historical context of previous rule changes and their significance.

Reviewing a timeline of amendments can provide insight into the evolving nature of mortgage application documentation, recognizing shifts in regulatory standards and borrower expectations.

Contact and support information

For users requiring assistance with the updated Rule 1003 Form and its amendments, pdfFiller offers comprehensive customer support options. Users can contact support for direct assistance or navigate to help centers for peer advice and shared experiences on collaborative document management.

Access to pdfFiller's customer service for specific inquiries.

Engagement with community forums for additional tips and discussions.

Staying informed about changes in mortgage documentation is essential. Leveraging tools and support will streamline this process, providing added confidence to borrowers and lenders alike.