Get the free Minimum Distribution or Systematic Partial Surrender Form

Show details

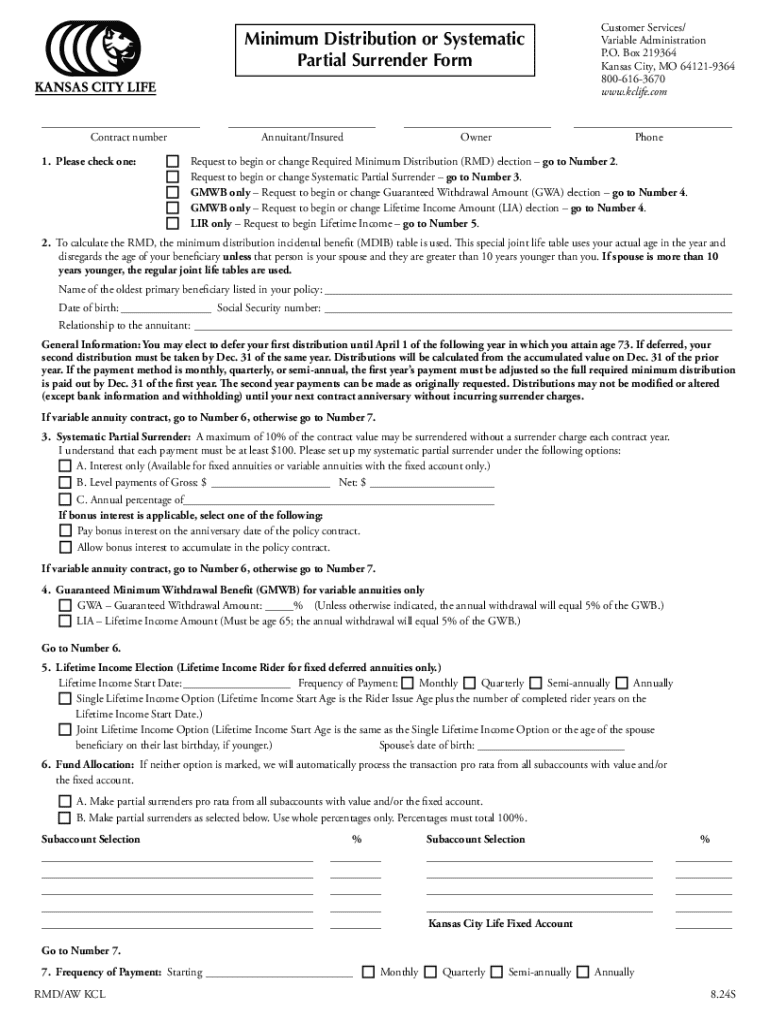

Minimum Distribution or Systematic Partial Surrender Form ___ Contract number 1. Please check one:___ Annuitant/Insured___ OwnerCustomer Services/ Variable Administration P.O. Box 219364 Kansas City, MO 641219364 8006163670 www.kclife.com ___ PhoneRequest to begin or change Required Minimum Distribution (RMD) election go to Number 2. Request to begin or change Systematic Partial Surrender go to Number 3. GMWB only Request to begin or change Guaranteed Withdrawal Amount (GWA) election go to...

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign minimum distribution or systematic

Edit your minimum distribution or systematic form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your minimum distribution or systematic form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing minimum distribution or systematic online

Here are the steps you need to follow to get started with our professional PDF editor:

1

Log in. Click Start Free Trial and create a profile if necessary.

2

Upload a document. Select Add New on your Dashboard and transfer a file into the system in one of the following ways: by uploading it from your device or importing from the cloud, web, or internal mail. Then, click Start editing.

3

Edit minimum distribution or systematic. Rearrange and rotate pages, insert new and alter existing texts, add new objects, and take advantage of other helpful tools. Click Done to apply changes and return to your Dashboard. Go to the Documents tab to access merging, splitting, locking, or unlocking functions.

4

Get your file. When you find your file in the docs list, click on its name and choose how you want to save it. To get the PDF, you can save it, send an email with it, or move it to the cloud.

pdfFiller makes dealing with documents a breeze. Create an account to find out!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out minimum distribution or systematic

How to fill out minimum distribution or systematic

01

Gather all necessary account statements and documents related to your retirement accounts.

02

Determine your required minimum distribution (RMD) age based on IRS rules, which is generally 72 years old.

03

Calculate your RMD using the IRS life expectancy tables and your account balance from the previous year.

04

Fill out the required distribution form provided by your financial institution or plan administrator.

05

Specify the amount of distribution you wish to take, ensuring it meets or exceeds the RMD.

06

Select your preferred method of receiving the distribution, whether it's a direct transfer, check, or other options.

07

Submit the completed form to your financial institution by the applicable deadline to ensure compliance.

Who needs minimum distribution or systematic?

01

Individuals who are age 72 or older and have tax-deferred retirement accounts, such as traditional IRAs, 401(k)s, and other similar plans.

02

Beneficiaries of inherited retirement accounts who are required to withdraw distributions.

03

Individuals who wish to supplement their income during retirement can also benefit from systematic withdrawals.

Minimum Distribution or Systematic Form: A Comprehensive Guide

Understanding minimum distributions

Minimum distributions are essential components of financial planning, especially as you transition into retirement. These distributions ensure that you withdraw necessary funds from your retirement accounts, which can include IRAs and 401(k)s, among others. The two primary types of minimum distributions are Required Minimum Distributions (RMDs) and systematic withdrawals. Understanding the differences and nuances of each can aid in effective financial management during retirement.

Required Minimum Distributions (RMDs) are mandatory withdrawals from retirement accounts starting at a certain age, while systematic withdrawals are more flexible and can be set up according to personal financial needs. Both strategies are crucial for adhering to tax regulations and managing income during retirement.

Definition and significance in financial planning.

Types of minimum distributions: Required Minimum Distributions (RMDs) vs. systematic withdrawals.

Required Minimum Distributions (RMDs)

RMDs kick in once you reach a specific age, typically 72 years for most retirement accounts. However, some exceptions apply, such as for certain inherited IRAs. RMDs are calculated based on the account balance and your life expectancy, following guidelines established by the IRS. Missing an RMD can lead to severe penalties, making it crucial to be aware of when and how to withdraw.

To calculate your RMD, you would first need to determine your account balance at the end of the previous year and then use the IRS life expectancy table to figure your necessary distribution period. This straightforward formula allows you to meet government requirements effectively.

Age requirements for RMDs.

Exceptions and special circumstances, such as inherited IRAs.

Calculation of RMDs

Calculating your RMD is central to ensuring you don't incur tax penalties. The process involves two key steps: determining your account balance as of December 31 of the previous year and dividing it by a distribution period from the IRS's life expectancy table. For example, if your traditional IRA balance was $100,000 and your life expectancy factor is 25.6, your RMD would be approximately $3,906.

It's essential to stay updated on IRS guidelines, as the tables for life expectancy can be updated over the years, affecting your distribution calculations.

Step-by-step guide to calculating RMDs.

IRS guidelines on life expectancy tables.

Reporting and withholding taxes on RMDs

When it comes to RMDs, proper reporting to the IRS is critical. Financial institutions are responsible for communicating these distributions, but the ultimate responsibility lies with you. Ensuring that your RMDs are reported properly helps avoid unnecessary tax penalties.

Additionally, when taking your RMD, you can choose to withhold taxes from your distributions. This is particularly beneficial if you want to avoid a larger tax bill when tax season arrives. To streamline your tax management, consider working with a financial advisor who can advise on the best withholding strategies based on your overall financial situation.

IRS reporting requirements for RMDs.

Tax withholding options and strategies to minimize tax liability.

Systematic withdrawal plans

A systematic withdrawal plan (SWP) offers a distinct approach to taking funds from your retirement savings. Unlike RMDs, which mandate specific withdrawal amounts based on IRS rules, an SWP allows you to withdraw a predetermined amount, at regular intervals, to create a steady income stream. This flexibility can be advantageous as it aligns more closely with your lifestyle and financial needs.

Benefits of adopting a systematic withdrawal strategy include the ability to tailor your withdrawals to match your spending needs, potential for more effective tax management, and the capability to adjust the frequency and amount based on market conditions or personal goals.

Definition and comparison with RMDs.

Benefits of using a systematic withdrawal strategy.

Establishing a systematic withdrawal plan

Creating a systematic withdrawal plan involves several considerations. First, determine the frequency and amount of your withdrawals to ensure they align with your overall financial goal without depleting your assets too quickly. Regular review and adjustment of this plan are imperative to adapting to changing market conditions or shifts in personal circumstances.

Consider the tax implications of your withdrawals, as different retirement accounts can have varied tax impacts. For instance, distributions from traditional IRAs are taxed as ordinary income, whereas qualified withdrawals from Roth IRAs are tax-free. Tailoring your systematic withdrawal plan to leverage these tax benefits can enhance your financial stability.

Steps to set up a plan.

Factors to consider: frequency, amount, investment goals.

Tax implications of systematic withdrawals

Understanding tax implications is crucial for retirement planning. Systematic withdrawals can influence your tax situation significantly. It's essential to be aware that non-qualified accounts may be taxed differently than qualified retirement accounts. For instance, capital gains tax may apply when withdrawing from taxable investments, whereas traditional IRAs will incur ordinary income tax.

Additionally, keeping an eye on the overall impacts of your withdrawals on Social Security benefits is important, as excessive income can lead to taxation on your benefits.

Tax considerations for different accounts.

How withdrawals affect your overall tax situation.

Managing distributions from multiple accounts

For those with several retirement accounts, managing distributions can feel overwhelming. Combining distributions from various IRAs requires extensive knowledge to ensure compliance with tax regulations while addressing your financial needs effectively. Keeping track of all account balances and understanding the associated tax implications is pivotal.

Coordinating RMDs across different account types adds another layer of complexity. For instance, RMDs from traditional IRAs are mandatory, while Roth IRAs do not have RMD requirements during the owner's lifetime. Understanding these rules helps streamline your withdrawal strategy and mitigates potential penalties.

Strategies for managing distributions from multiple retirement accounts.

Tips for calculating and fulfilling RMDs from traditional and Roth accounts.

Advanced strategies for distributions

For those looking to optimize their distribution strategy further, Qualified Charitable Distributions (QCDs) can be a beneficial tool. A QCD allows you to transfer funds directly from your IRA to a qualified charity, potentially reducing your taxable income and fulfilling your charitable giving goals simultaneously.

It's equally essential to handle under- or over-distributions appropriately. Missing your RMD can result in a substantial penalty of 50% of the required amount, while over-distributions may lead to tax burdens you weren't prepared to manage. Therefore, maintaining a dynamic approach to your withdrawal strategy, adjusting based on market performance, is critical.

Definition and benefits of QCDs.

Strategies for adapting withdrawal plans during market volatility.

Tools and resources for managing distributions

One versatile tool for managing the documentation involved in RMDs and systematic withdrawals is pdfFiller. This cloud-based platform empowers users to create, edit, eSign, and manage financial documents seamlessly from any location, making financial administration far less cumbersome.

Using pdfFiller, you can keep your records organized and accessible, improving efficiency when submitting necessary documentation to financial institutions. Whether it's IRS forms or withdrawal requests, pdfFiller simplifies the documentation process, ensuring you remain focused on your retirement goals.

How pdfFiller can streamline the documentation process for RMDs and systematic withdrawals.

Calculators for RMDs and withdrawal strategies available via pdfFiller.

Best practices for record keeping

Maintaining detailed records is a cornerstone of effective financial management, particularly when it comes to RMDs and systematic withdrawals. Using tools like pdfFiller for document management not only ensures thorough record-keeping but also facilitates review and audits by keeping everything accessible and organized.

Best practices for keeping track include regularly updating your accounts and records after each withdrawal, tracking any changes in tax law that might affect your distributions, and setting reminders for key distribution dates to maintain compliance and avoid penalties.

Importance of maintaining thorough records for tax purposes.

Suggested organizational strategies using pdfFiller tools.

FAQs about minimum distributions and systematic withdrawal plans

Understanding the nuances of RMDs and systematic withdrawal plans often raises several questions. For example, many individuals wonder what happens if they miss their RMD deadline. The IRS imposes dire penalties, so it's crucial to prioritize these withdrawals. If you find yourself in a bind, it's advisable to consult a tax advisor for potential corrective measures.

Similarly, questions about how withdrawals can impact Social Security benefits are prevalent. Essentially, while the withdrawals themselves do not directly affect your Social Security, the resulting increase in income could lead to higher taxes on those benefits. It's wise to strategize your distributions carefully.

What happens if I miss my RMD deadline?

How do I determine the right withdrawal amount?

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I edit minimum distribution or systematic from Google Drive?

People who need to keep track of documents and fill out forms quickly can connect PDF Filler to their Google Docs account. This means that they can make, edit, and sign documents right from their Google Drive. Make your minimum distribution or systematic into a fillable form that you can manage and sign from any internet-connected device with this add-on.

How do I make edits in minimum distribution or systematic without leaving Chrome?

minimum distribution or systematic can be edited, filled out, and signed with the pdfFiller Google Chrome Extension. You can open the editor right from a Google search page with just one click. Fillable documents can be done on any web-connected device without leaving Chrome.

How do I fill out minimum distribution or systematic on an Android device?

Use the pdfFiller Android app to finish your minimum distribution or systematic and other documents on your Android phone. The app has all the features you need to manage your documents, like editing content, eSigning, annotating, sharing files, and more. At any time, as long as there is an internet connection.

What is minimum distribution or systematic?

Minimum distribution or systematic refers to the required withdrawals from retirement accounts, especially for individuals who reach a certain age, typically 72, to ensure that funds are not left in tax-advantaged accounts indefinitely.

Who is required to file minimum distribution or systematic?

Individuals who have retirement accounts such as 401(k) plans or IRAs and have reached the required minimum distribution age are required to file for minimum distributions.

How to fill out minimum distribution or systematic?

To fill out minimum distribution or systematic, individuals should calculate their required distribution amount based on their age and account balance, then formally request the distribution from their retirement plan administrator.

What is the purpose of minimum distribution or systematic?

The purpose of minimum distribution or systematic is to ensure that individuals begin withdrawing funds from their retirement accounts, thereby triggering tax implications and preventing the indefinite deferral of taxes.

What information must be reported on minimum distribution or systematic?

Information that must be reported includes the account holder's age, the account balance at the end of the previous year, the amount of distribution taken, and whether any penalties are applied for not meeting the minimum distribution requirements.

Fill out your minimum distribution or systematic online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Minimum Distribution Or Systematic is not the form you're looking for?Search for another form here.

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.