Last updated on

Sep 21, 2025

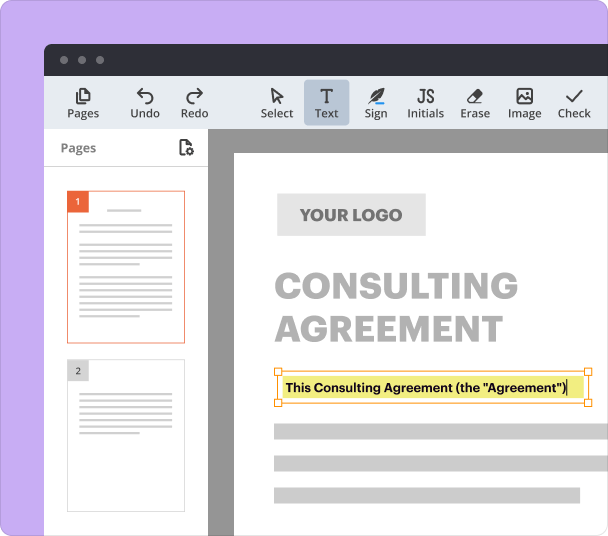

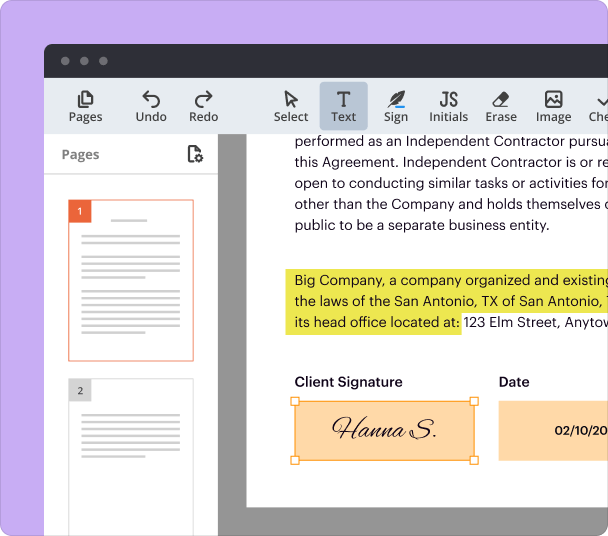

Go beyond editing and add context to your changes. After fixing a typo or updating a section, drop a comment or highlight the area to pinpoint and explain edits.

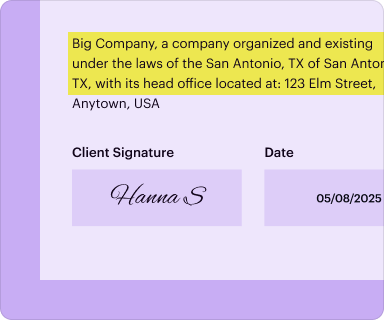

Annotating living trust PDFs involves adding notes, comments, or highlights to the document. With pdfFiller, you can seamlessly accomplish this to enhance collaboration and ensure every detail is captured effectively.

Annotation refers to the process of adding notes or comments to a document, aimed at clarifying content or providing additional information. In the case of living trusts, annotation can help involved parties understand terms, conditions, or instructions in a more digestible format. This can be especially beneficial when multiple individuals need to review or understand the terms laid out in the trust document.

Annotating documents like living trusts enhances collaboration by enabling all parties involved to communicate their thoughts clearly. This is particularly important given the complexities often associated with legal documents, as annotation helps eliminate ambiguity and fosters better understanding. Additionally, it allows users to track changes and discussions, making it easier to manage updates and revisions over time.

pdfFiller offers a robust range of annotation features designed to simplify the process of marking up PDFs. Key features include:

pdfFiller primarily supports PDF format for annotations but also allows for annotation on various document types, including:

This wide compatibility ensures you can annotate an array of document types as you manage your living trust paperwork.

pdfFiller is optimized for use in all major web browsers—Chrome, Firefox, Safari, and Edge—allowing smooth functionality regardless of your platform. Users can enjoy seamless annotation experiences with no installations or additional software. Simply upload your living trust PDF, utilize the annotation tools, and save changes directly to your document online.

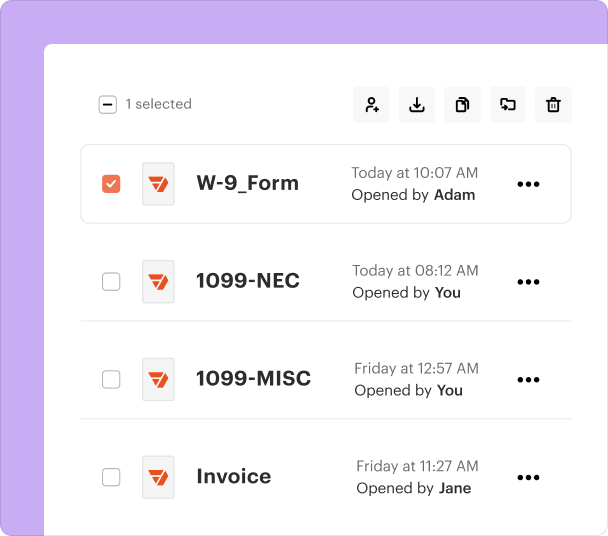

pdfFiller makes managing annotations straightforward with features that allow users to track, edit, and view changes. Some managing capabilities include:

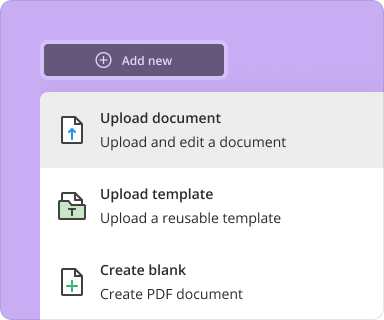

Follow these steps to annotate your living trust PDF using pdfFiller:

Utilizing pdfFiller for annotating living trust documents provides several advantages:

Different professional sectors and situations can benefit from PDF annotation:

These use cases demonstrate the practicality of using pdfFiller for efficient document management.

When comparing pdfFiller’s annotation capabilities with those of competing platforms such as Adobe Acrobat or DocuSign, several distinctions arise:

Annotating living trust PDFs with pdfFiller not only makes the document management process more interactive but also enhances understanding and clarity among all involved parties. Whether you're a legal professional or someone managing personal trusts, the powerful annotation features available in pdfFiller can significantly simplify your workflow. With easy-to-use tools, cross-browser compatibility, and secure management options, pdfFiller is the ideal platform for effective PDF annotation.