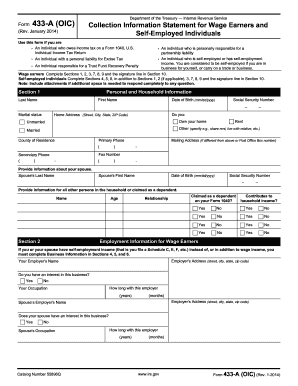

IRS 433-A 2008 free printable template

Get, Create, Make, and Sign IRS 433-A

Instructions and Help about IRS 433-A

How to edit IRS 433-A

How to fill out IRS 433-A

About IRS 433-A 2008 previous version

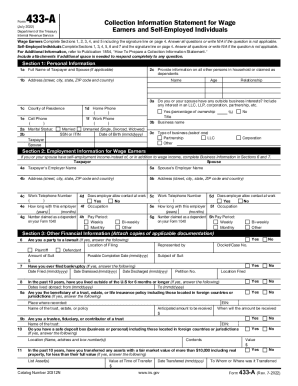

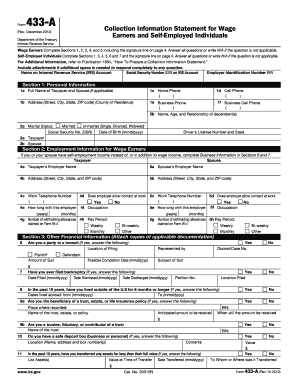

What is IRS 433-A?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

Where do I send the form?

What is the purpose of this form?

Who needs the form?

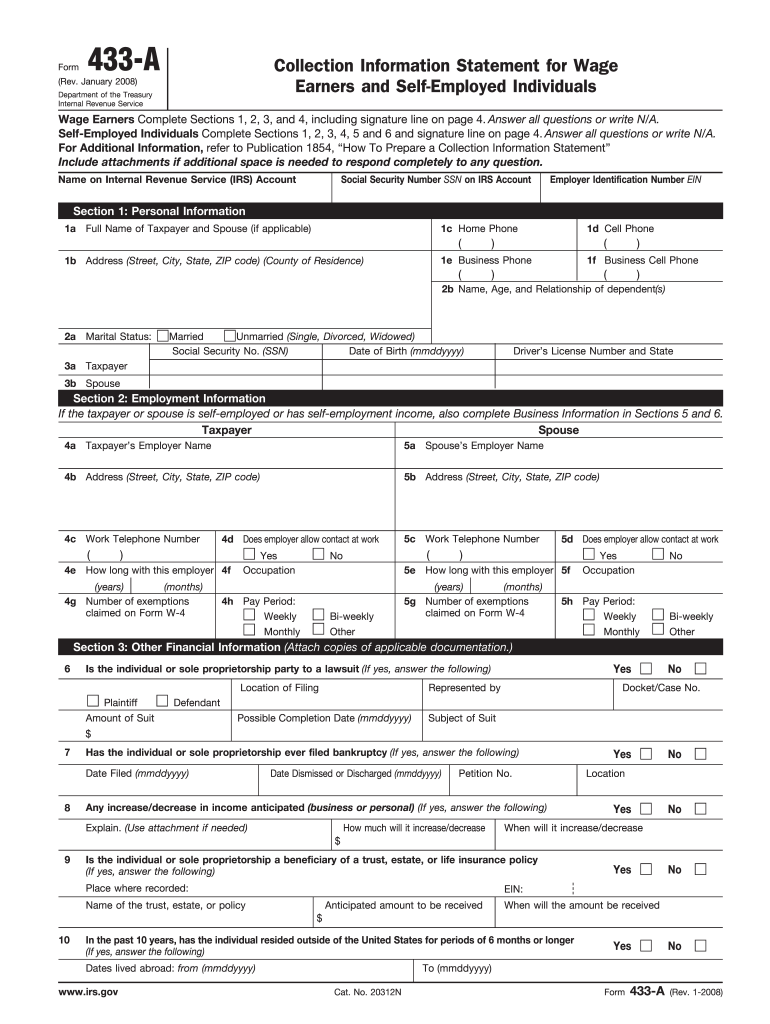

Components of the form

What information do you need when you file the form?

FAQ about IRS 433-A

What should I do if I realize I've made a mistake on my IRS Form 433A 2008 after submitting it?

If you need to correct mistakes on your IRS Form 433A 2008 after submission, you can file an amended version of the form. Make sure to indicate clearly that the new form supersedes the previous submission. Keeping a copy of both forms is important for your records.

How can I check the status of my IRS Form 433A 2008 submission?

To verify the status of your IRS Form 433A 2008, you can contact the IRS directly or use their online services. Make sure to have your submission details on hand, as you will need to confirm your identity for any inquiry regarding your form's processing.

Is e-signature acceptable for filing Form 433A 2008?

Yes, electronic signatures are generally accepted for Form 433A 2008 when filed online, provided you follow the guidelines set by the IRS which ensure the authenticity of the signature. It’s crucial to review the specific e-filing instructions for any updates regarding signatory requirements.

What common errors should I watch for when completing IRS Form 433A 2008?

Common errors to avoid when completing your IRS Form 433A 2008 include incorrect Social Security numbers, failing to accurately report income and expense amounts, and not signing the form correctly. Thoroughly double-checking all entries before submission can minimize these mistakes.

What action should I take if I receive an IRS notice regarding my Form 433A 2008?

If you receive an IRS notice concerning your Form 433A 2008, carefully read the communication to understand the issue raised. Prepare any necessary documentation that supports your case and respond within the timeline provided in the notice to address any concerns raised by the IRS.