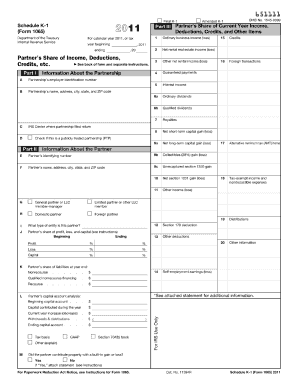

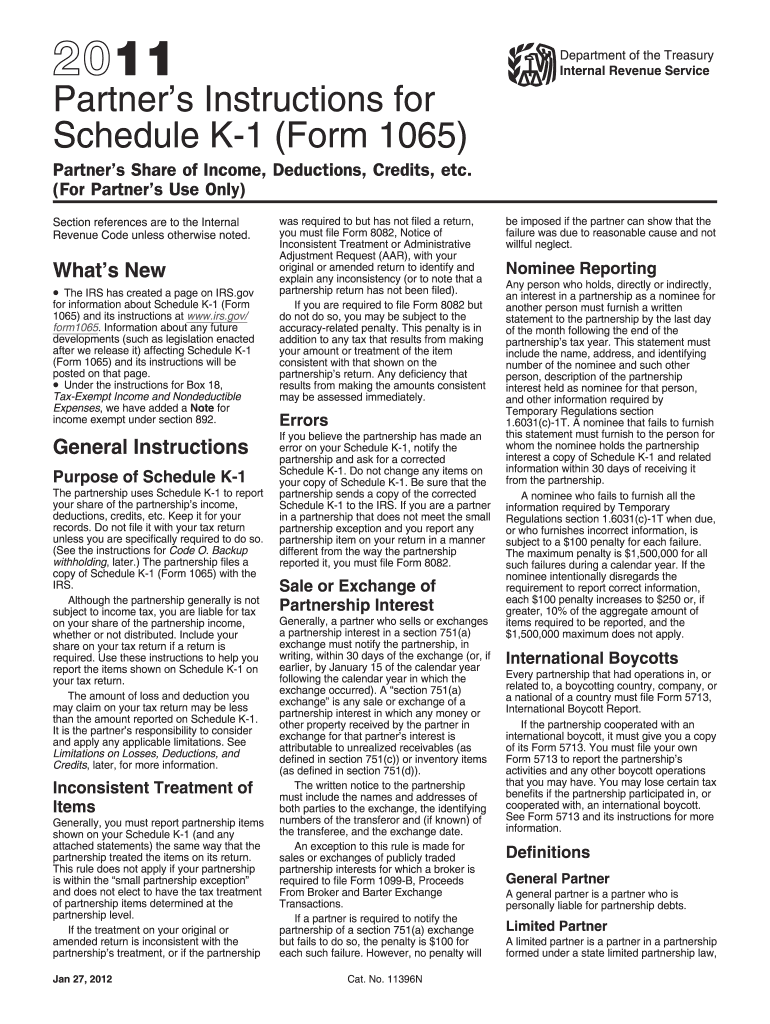

IRS Instruction 1065 - Schedule K-1 2011 free printable template

Get, Create, Make, and Sign IRS Instruction 1065 - Schedule K-1

Instructions and Help about IRS Instruction 1065 - Schedule K-1

How to edit IRS Instruction 1065 - Schedule K-1

How to fill out IRS Instruction 1065 - Schedule K-1

About IRS Instruction 1065 - Schedule K-1 2011 previous version

What is IRS Instruction 1065 - Schedule K-1?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

What is the purpose of this form?

Who needs the form?

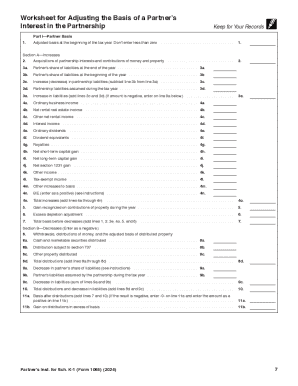

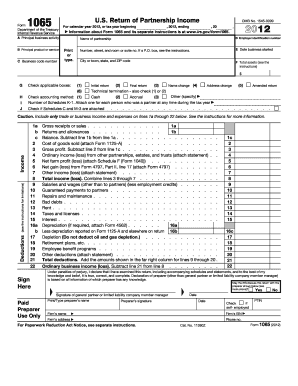

Components of the form

What information do you need when you file the form?

Where do I send the form?

FAQ about IRS Instruction 1065 - Schedule K-1

What should I do if I discover an error after filing form 1065 2011?

If you realize that there was an error on your form 1065 2011 after it has been submitted, you can file an amended return. This involves completing a new form with the correct information and marking it as an amendment. Make sure to include a cover letter explaining the changes for clarity.

How can I verify the status of my submitted form 1065 2011?

You can check the status of your form 1065 2011 by contacting the IRS directly or by using their online tools if you filed electronically. Keep in mind that processing times may vary, and it’s important to allow some time before checking on the status after submission.

Is e-signature acceptable when submitting form 1065 2011?

Yes, the IRS accepts electronic signatures for form 1065 2011 when e-filing. Ensure that you follow the specific guidelines provided by the e-filing software you are using to ensure compliance with signature requirements.

What should I do if my e-filed form 1065 2011 gets rejected?

If your form 1065 2011 is rejected after e-filing, review the error codes provided by the IRS. Correct the issues indicated and resubmit your filing as soon as possible to avoid further delays and potential penalties.

How long should I retain records related to form 1065 2011 filings?

It is advisable to retain records related to your form 1065 2011 for at least three years from the date you filed, as this period typically covers the statute of limitations for audits. However, maintaining records for a longer duration is prudent in case of inquiries or audits from the IRS.