NM TRD PIT-1 2016 free printable template

Get, Create, Make, and Sign NM TRD PIT-1

Instructions and Help about NM TRD PIT-1

How to edit NM TRD PIT-1

How to fill out NM TRD PIT-1

About NM TRD PIT-1 2016 previous version

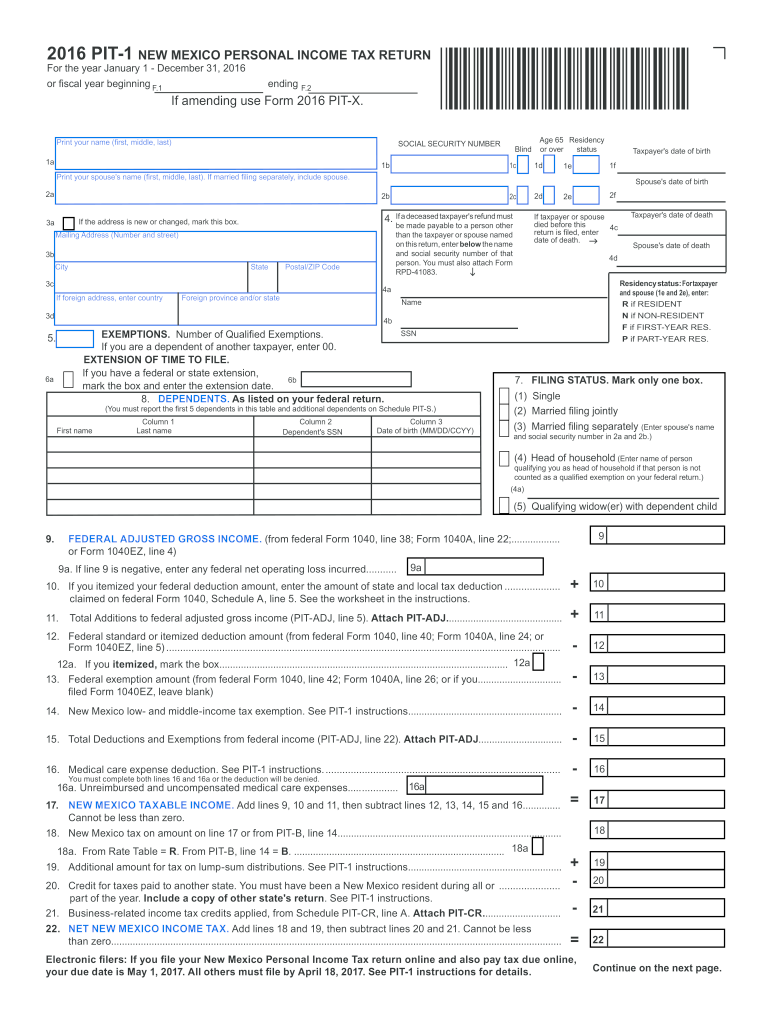

What is NM TRD PIT-1?

Who needs the form?

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about NM TRD PIT-1

What should I do if I discover an error after submitting my new mexico tax form?

If you find an error on your new mexico tax form after submission, you should file an amended return to correct the mistake. Ensure you indicate the changes made and include any necessary documentation to support your correction. This process helps maintain accurate records and compliance with state tax regulations.

How can I verify the status of my submitted new mexico tax form?

To check the status of your submitted new mexico tax form, visit the New Mexico Taxation and Revenue Department's website and use their online tracking system. You will typically need your Social Security number and the amount of your refund or balance due to access your status efficiently.

Are e-signatures accepted for the new mexico tax form?

Yes, e-signatures are permitted for the new mexico tax form, providing that they comply with the state’s regulations regarding electronic submissions. It is advisable to follow the specified guidelines to ensure that your submission is accepted without issues.

What should I do if my new mexico tax form is rejected?

If your new mexico tax form gets rejected, carefully review the rejection notice for error codes and guidance on the issue. Make the necessary corrections and resubmit your form as soon as possible to comply with the filing requirements and avoid penalties.

How long should I retain records related to my new mexico tax form?

You should retain records related to your new mexico tax form for at least three years after the filing date. This period covers typical audit requirements and ensures you have documentation available in case of any disputes or clarifications needed by the state.