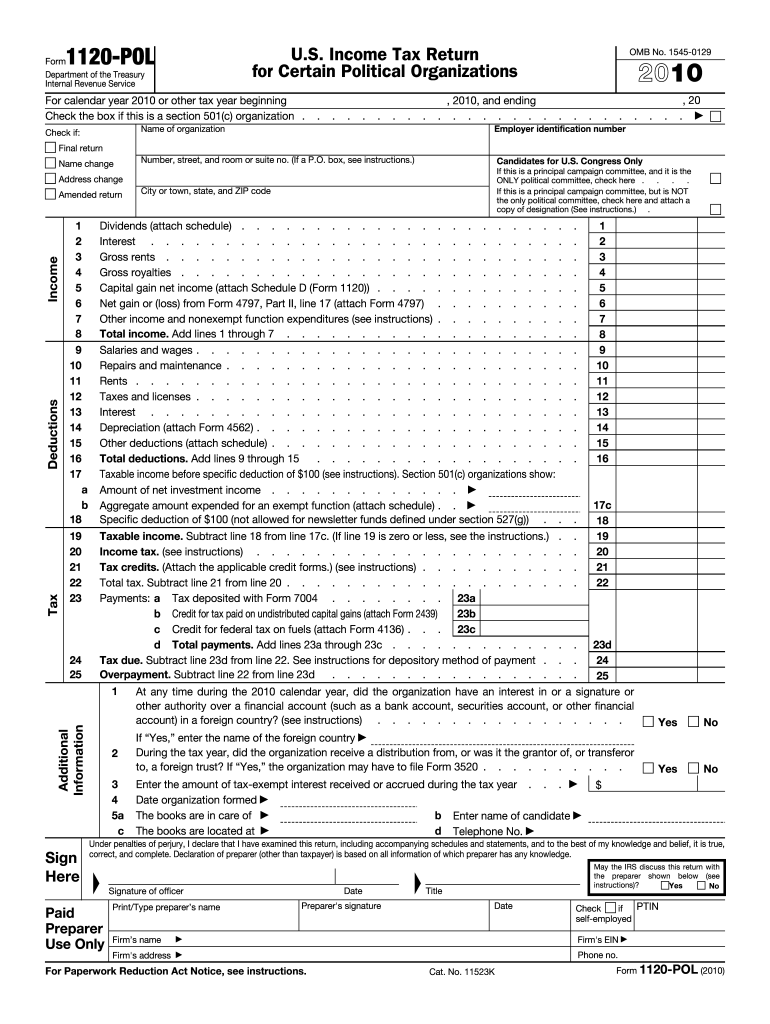

IRS 1120-POL 2010 free printable template

Get, Create, Make, and Sign IRS 1120-POL

Instructions and Help about IRS 1120-POL

How to edit IRS 1120-POL

How to fill out IRS 1120-POL

About IRS 1120-POL 2010 previous version

What is IRS 1120-POL?

What is the purpose of this form?

Who needs the form?

When am I exempt from filling out this form?

Components of the form

Due date

What payments and purchases are reported?

How many copies of the form should I complete?

What are the penalties for not issuing the form?

What information do you need when you file the form?

Is the form accompanied by other forms?

Where do I send the form?

FAQ about IRS 1120-POL

What should I do if I need to correct my submitted 2010 irs form tax?

If you've made a mistake on your submitted 2010 irs form tax, you need to file an amended return. Make sure to use the correct form designated for amendments, include the necessary corrections, and provide a brief explanation of the changes made. Keep a copy for your records.

How can I track the status of my 2010 irs form tax submission?

To track the status of your 2010 irs form tax, you can use the IRS's online tracking tool. This tool allows you to see whether your form has been received and processed, along with any potential issues you may need to address. Be sure to have your details ready for verification.

What should be done if I receive an audit notice related to my 2010 irs form tax?

If you receive an audit notice regarding your 2010 irs form tax, it's essential to respond promptly and prepare the requested documentation. Gather all relevant records and consult with a tax professional for guidance on how to proceed effectively.

Can I use electronic signatures when filing my 2010 irs form tax?

Yes, electronic signatures are generally acceptable for the 2010 irs form tax, provided you follow the IRS guidelines on e-signatures and ensure that your signature is secure and properly executed. This can facilitate a smoother filing process.