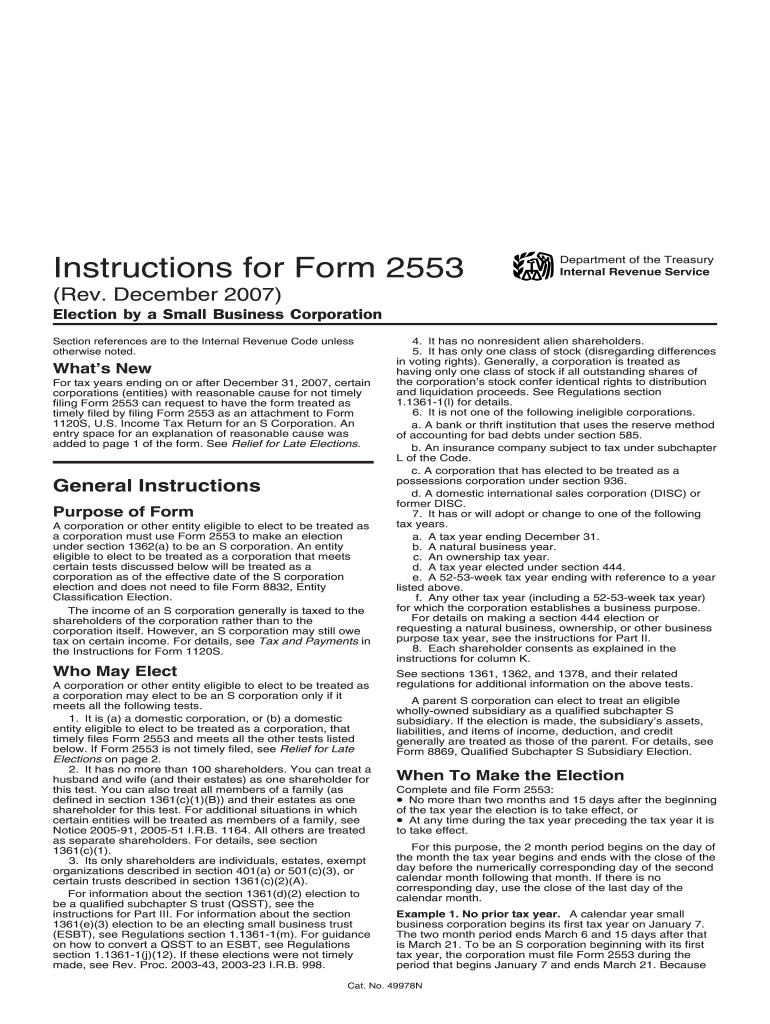

IRS Instruction 2553 2007 free printable template

Get, Create, Make, and Sign IRS Instruction 2553

Instructions and Help about IRS Instruction 2553

How to edit IRS Instruction 2553

How to fill out IRS Instruction 2553

About IRS Instruction 2 previous version

What is IRS Instruction 2553?

What is the purpose of this form?

Who needs the form?

When am I exempt from filling out this form?

Components of the form

What are the penalties for not issuing the form?

What information do you need when you file the form?

Is the form accompanied by other forms?

Where do I send the form?

FAQ about IRS Instruction 2553

What should I do if I realize I've made an error on the irs form 2553 2007 after filing?

If you discover mistakes on your submitted irs form 2553 2007, you should file an amended return using form 1120-S, including the corrected information. It's essential to clearly indicate that the form is an amendment and to provide any necessary explanations regarding the changes made.

How can I check the status of my submitted irs form 2553 2007?

To verify the status of your irs form 2553 2007, you can contact the IRS directly or use the IRS’s online tools, if available. Keep your confirmation number and relevant details handy to expedite the process. It’s important to allow a few weeks after submission for processing before checking the status.

What should I do if my e-filed irs form 2553 2007 is rejected?

If your e-filed irs form 2553 2007 is rejected, carefully review the rejection code provided to understand the issue. Common errors include mismatches in taxpayer information. Correct the identified problems and resubmit the form promptly to avoid any delay in your tax status.

Are there specific retention requirements for documents related to the irs form 2553 2007?

Yes, it's recommended to retain a copy of the irs form 2553 2007 and any supporting documents for at least three years from the date the form was filed. This helps ensure compliance and provides necessary documentation in case of future inquiries or audits.

What legal considerations should I keep in mind when e-signing the irs form 2553 2007?

When e-signing the irs form 2553 2007, ensure that you are aware of the IRS's requirements for electronic signatures. Typically, e-signatures must comply with specific standards to be considered valid. It's advisable to use trusted software or platforms that meet these requirements to ensure compliance.