Last updated on Apr 18, 2016

Get the free Credit Report Dispute Letter

We are not affiliated with any brand or entity on this form

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

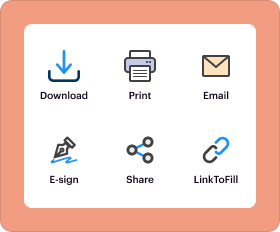

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

What is Dispute Letter

The Credit Report Dispute Letter is a personal legal document used by consumers to dispute inaccurate information in their credit reports.

pdfFiller scores top ratings on review platforms

Who needs Dispute Letter?

Explore how professionals across industries use pdfFiller.

Dispute Letter is needed by:

-

Consumers seeking to correct errors on their credit reports

-

Individuals applying for loans or mortgages

-

People planning to improve their credit scores

-

Borrowers facing credit assessment issues

-

Consumers wanting to engage with credit bureaus

Comprehensive Guide to Dispute Letter

What is a Credit Report Dispute Letter?

A Credit Report Dispute Letter is an essential document utilized by U.S. consumers to formally address inaccuracies within their credit reports. This letter serves the purpose of notifying credit bureaus of any incorrect information, prompting them to investigate and rectify those errors. It is crucial for consumers to engage in this process, as correcting inaccuracies can significantly impact their credit scores and overall financial health.

By disputing incorrect information, consumers not only protect their financial reputation but also ensure they make informed decisions about their credit history. Utilizing a dispute letter template simplifies this crucial task and empowers consumers to take control of their credit reports.

Purpose and Benefits of Using a Credit Report Dispute Letter

Submitting a Credit Report Dispute Letter offers numerous advantages for addressing inaccuracies found in one's credit report. Firstly, by correcting these inaccuracies, consumers often see an improvement in their credit scores, which can lead to better loan terms and interest rates. Furthermore, having accurate credit reports enhances one's ability to secure loans, mortgages, and other financial services.

This process not only corrects past errors but also empowers consumers to take charge of their credit history actively. Regularly checking and rectifying any issues using a free credit report dispute serves as a proactive approach to maintaining financial health.

Who Needs a Credit Report Dispute Letter?

A variety of individuals may find themselves in need of a Credit Report Dispute Letter. Those who have recently applied for loans, experienced identity theft, or detected discrepancies in their credit report will benefit from utilizing this document. Understanding consumer rights regarding credit reporting is essential, and consumers should remember that they are entitled to dispute incorrect information at any time.

It is vital for consumers to regularly check their credit reports to catch any inaccuracies early on. A credit bureau dispute form is crucial for addressing these discrepancies and ensuring fair treatment from credit reporting agencies.

How to Fill Out the Credit Report Dispute Letter Online: Step-by-Step Guide

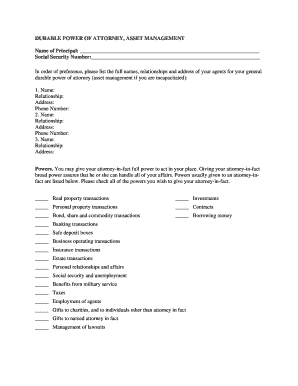

Filling out a Credit Report Dispute Letter online involves several key steps to ensure accuracy and completeness. First, you will need to provide personal information, such as your full name, address, and Social Security number. Next, detail the items you wish to dispute, clearly specifying the inaccuracies.

Follow these steps for a successful submission:

-

Begin with your personal details, including your contact information.

-

List the specific items on your credit report that you are disputing.

-

Provide a brief explanation of why you believe the information is incorrect.

-

Select the appropriate credit bureau for submission.

By carefully following these instructions, you can ensure your dispute letter is effectively completed.

Submission Methods for Your Credit Report Dispute Letter

After completing your Credit Report Dispute Letter, it is essential to submit it correctly. There are several ways to submit your dispute letter:

-

Mail your letter to the credit bureau’s designated address.

-

Submit the letter online via the credit bureau's official website.

Keeping proof of submission is vital for tracking your dispute's progress. Additionally, you can inquire about the status of your dispute through the credit bureau's online portal or by contacting their customer service department. Being aware of any associated fees and deadlines is crucial to ensure timely resolution of your dispute.

Common Errors to Avoid When Filing Your Credit Report Dispute Letter

Filing a Credit Report Dispute Letter can be straightforward, but consumers often make common mistakes that can hinder the process. Be aware of the following errors:

-

Failing to include personal identification information.

-

Not providing adequate explanations for the dispute.

-

Submitting the letter without reviewing it for accuracy.

Each of these mistakes could delay the review process or even lead to rejection of the dispute. Taking the time to ensure all details are correct before sending can save you significant time and effort in the long run.

Following Up After Submitting Your Credit Report Dispute Letter

Once you have submitted your Credit Report Dispute Letter, it’s important to know what to expect next. Credit bureaus typically respond to disputes within 30 days. During this time, you can check the status of your dispute through their online system or by contacting customer service.

In cases where the dispute does not produce a favorable outcome, consider taking additional steps, such as seeking further clarification from the bureau or filing a complaint with the Consumer Financial Protection Bureau (CFPB) if necessary.

Ensuring Security and Compliance While Handling Sensitive Documents

When dealing with the sensitive information contained in a Credit Report Dispute Letter, security is paramount. pdfFiller employs robust security measures, including 256-bit encryption, to protect your personal data. Adhering to compliance with standards such as HIPAA and GDPR is also crucial to ensure your privacy is safeguarded throughout the dispute process.

Being vigilant about protecting your personal information is essential when navigating the complexities of credit disputes.

Using pdfFiller to Create Your Credit Report Dispute Letter

pdfFiller provides an efficient platform for crafting your Credit Report Dispute Letter. With user-friendly features that facilitate easy editing, document management, and eSigning, pdfFiller streamlines the process, allowing consumers to fill out credit report dispute letters directly online.

Take advantage of pdfFiller to manage your dispute effectively, ensuring secure handling of your document at every step of the process.

Real-World Example of a Credit Report Dispute Letter

For reference, reviewing a sample completed Credit Report Dispute Letter can be highly beneficial. This sample illustrates the format and details necessary for a successful submission. Personalizing your letter based on the specifics of your dispute enhances its effectiveness.

Be mindful to adjust any sample letter according to your unique circumstances, as this will help in clearly communicating your dispute to the credit bureau.

How to fill out the Dispute Letter

-

1.Access pdfFiller and search for the 'Credit Report Dispute Letter' form in the template library.

-

2.Click on the form to open it in the pdfFiller interface.

-

3.Gather necessary personal information, including your name, address, and account information relating to the disputed items.

-

4.Begin by filling out your personal details in the designated fields at the top of the form.

-

5.Provide a clear description of the inaccurate information you wish to dispute, ensuring accuracy and completeness.

-

6.Use checkboxes to select which credit bureau(s) you are sending the dispute letter to.

-

7.Clearly state your request for correction or deletion of the inaccurate information in the appropriate section.

-

8.Review the filled form for any errors or missing information to ensure that all details are accurate.

-

9.Add your signature to authenticate the letter, which may be done electronically within pdfFiller.

-

10.Once finalized, save the document and select your preferred method of submission, whether by download or directly mailing it.

Who can use the Credit Report Dispute Letter?

Any consumer in the US who identifies inaccurate information on their credit report can use the Credit Report Dispute Letter to formally request a correction.

What information do I need to fill out this letter?

You will need personal details such as your name, address, specific account information, and details of the inaccuracies you are disputing before filling out the letter.

How do I submit the completed dispute letter?

After completing the dispute letter on pdfFiller, you can either download the document to send via mail or submit it electronically if the credit bureau allows such submissions.

What are common mistakes to avoid when filling out the dispute letter?

Ensure accuracy in your personal information, avoid vague descriptions of the disputed items, and make sure your letter is signed before submission to prevent delays.

Is there a deadline for disputing errors on my credit report?

While there's no strict deadline, it's recommended to dispute inaccuracies as soon as you notice them to ensure timely corrections can be processed by the credit bureaus.

Are there any fees associated with submitting a credit dispute?

Typically, there are no fees for disputing errors on credit reports. However, ensure to check with specific credit bureaus as some may have unique procedures.

How long does it take for a credit dispute to be processed?

Credit bureaus are required by law to investigate disputes within 30 days. However, the time may vary depending on the complexity of the dispute.

Related Forms

Get the latest insights from our blog

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.