Get the free 457(b) Deferred Compensation Plan Deferral Change Form

Show details

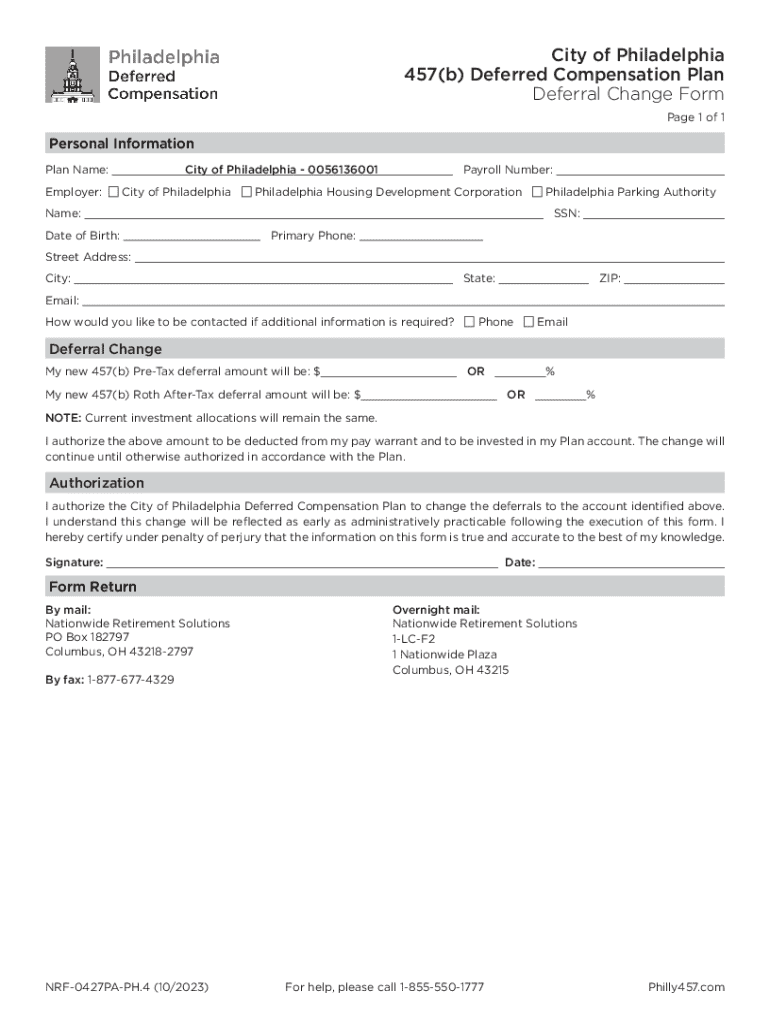

This form allows employees of the City of Philadelphia to change their pre-tax or Roth after-tax deferral amounts for the 457(b) Deferred Compensation Plan.

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign 457b deferred compensation plan

Edit your 457b deferred compensation plan form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your 457b deferred compensation plan form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing 457b deferred compensation plan online

To use our professional PDF editor, follow these steps:

1

Set up an account. If you are a new user, click Start Free Trial and establish a profile.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit 457b deferred compensation plan. Add and change text, add new objects, move pages, add watermarks and page numbers, and more. Then click Done when you're done editing and go to the Documents tab to merge or split the file. If you want to lock or unlock the file, click the lock or unlock button.

4

Get your file. When you find your file in the docs list, click on its name and choose how you want to save it. To get the PDF, you can save it, send an email with it, or move it to the cloud.

It's easier to work with documents with pdfFiller than you can have believed. You may try it out for yourself by signing up for an account.

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out 457b deferred compensation plan

How to fill out 457b deferred compensation plan

01

Review the eligibility requirements for the 457b deferred compensation plan provided by your employer.

02

Obtain the necessary enrollment forms from your HR department or their website.

03

Decide how much of your salary you want to defer into the 457b plan (up to the legal limit).

04

Fill out the enrollment forms, including your personal details, chosen deferral amount, and investment preferences.

05

Submit the completed forms to your HR department before the enrollment deadline.

06

Confirm your deferral contributions and investment selections through your employer’s payroll system.

07

Monitor your account regularly to make adjustments as needed.

Who needs 457b deferred compensation plan?

01

State and local government employees looking to save for retirement.

02

Non-profit organization employees who qualify for the plan.

03

High-income earners wanting to supplement their retirement savings beyond traditional retirement accounts.

04

Employees seeking tax-deferred growth on their retirement savings.

Understanding the 457b Deferred Compensation Plan Form

Understanding the 457b deferred compensation plan

A 457b deferred compensation plan is a type of retirement savings plan that allows employees of state and local governments, as well as certain non-profit organizations, to defer a portion of their earnings until retirement. This unique tax-advantaged account is designed specifically for public sector workers, making it a vital component of their retirement strategy.

Key features of a 457b plan include pre-tax contributions that reduce an individual's taxable income and the potential for tax-deferred growth on investments. Unlike other retirement plans, such as 401(k)s or 403(b)s, 457b plans often allow for various types of contribution options and are not subject to the same early withdrawal penalties, making them appealing for many employees.

Pre-tax contributions lower taxable income.

Funds grow tax-deferred until withdrawal.

Different from 401(k) and 403(b) in terms of regulations.

Eligibility for the 457b deferred compensation plan

Eligibility for a 457b deferred compensation plan largely depends on your employer's participation in this type of program. Generally, employees of state and local governments can enroll. Certain non-profit employees qualified under the Internal Revenue Code may also participate. This feature distinguishes the 457b plan from others like the 401(k), which can have a broader eligibility criterion.

To participate, employees must meet specific criteria, including employment status and the opting into the plan through the appropriate enrollment process. It is a common misconception that only public sector employees can benefit, but non-profit workers under specific conditions may also gain access to these plans.

Public employees of state and local governments are eligible.

Certain non-profit organizations may offer 457b plans.

Eligibility criteria may vary by state or organization.

Contributions to the 457b plan

For 2023, the contribution limit for a 457b deferred compensation plan is set at $22,500. Employees aged 50 and older can take advantage of catch-up contributions, allowing them to contribute an additional $7,500, making for a total of $30,000. It’s essential to maximize these contributions, as they play a significant role in securing a comfortable retirement.

The contributions can be categorized into two types: elective deferrals, where employees choose to postpone a portion of their salary before taxes, and non-elective contributions, which are made by employers. This flexibility allows participants to customize their saving strategy based on personal financial goals.

Standard contribution limit is $22,500.

Catch-up contribution limit is an additional $7,500 for those aged 50+.

Contributions can be elective or non-elective based on the employer’s provisions.

Completing the 457b deferred compensation plan form

Filling out the 457b deferred compensation plan form accurately is critical for a smooth enrollment process. The form typically requires personal information such as your name, address, and social security number, along with your employment details and chosen contribution amounts.

To ensure that you fill it out correctly, follow this step-by-step guide:

Gather all required documents, including identification and employment verification.

Input personal information accurately on the form.

Select your preferred contribution options, including the amount and frequency.

Sign and date the form to complete your enrollment.

Be cautious of common mistakes, such as incorrect social security numbers or miscalculating contribution amounts, which can delay your application process.

Managing your 457b plan

Once enrolled in the 457b deferred compensation plan, managing your account effectively is vital. Utilizing tools such as pdfFiller can greatly streamline your experience. You can easily access your account online, check your contribution status, and even edit your forms when needed, all through a user-friendly interface.

Regularly reviewing your contribution amounts will help you stay aligned with your retirement goals. As life circumstances change, adjusting these amounts is important for optimal savings. pdfFiller provides an interactive platform that allows you to track contributions and review investment performance seamlessly.

Access account online via pdfFiller for easy management.

Edit contribution forms as necessary.

Regularly check your retirement goals and adjust contributions accordingly.

Advantages of the 457b plan

One of the principal advantages of a 457b deferred compensation plan is the favorable tax treatment of contributions and withdrawals. Depositing pre-tax dollars means that you'll reduce your taxable income, and your money grows tax-deferred until you withdraw it in retirement, often at a lower tax rate.

Another strength is the flexibility in withdrawal options. Unlike some other retirement plans, 457b participants may withdraw funds without the typical 10% penalty before reaching the age of 59½. This flexibility can be especially beneficial during unforeseen financial circumstances.

Tax treatment allows for growth without immediate tax obligations.

Flexibility in withdrawal options minimizes penalties.

Potential for higher contribution limits compared to other retirement accounts.

Withdrawal rules and distribution options

Understanding the withdrawal rules for the 457b deferred compensation plan helps in effective financial planning. Withdrawals can typically be made in several ways, including early withdrawals, in-service withdrawals, or rollovers to other retirement accounts.

However, taxation of withdrawals varies; they are taxed as ordinary income in the year they are taken. In addition, 457b plans often provide survivor benefits, ensuring that funds can be passed on to beneficiaries under certain conditions, enhancing financial security for loved ones.

Early withdrawals may be permitted without penalty.

In-service withdrawals are available under certain conditions.

Rollovers allow movement of funds between retirement accounts.

Resources for participants

When enrolling in a 457b deferred compensation plan, certain documents are required. These may include proof of employment, identification, and completed enrollment forms. It is often recommended to prepare for frequently asked questions, such as how changing jobs may affect your contributions or the tax implications of your plan.

Educational tools and calculators available through platforms like pdfFiller can also aid participants in understanding their plan better. Utilizing these resources can help ensure that you make informed decisions about your retirement savings.

Documents required for enrollment include identification and proof of employment.

FAQs help clarify how the plan interacts with job changes and tax obligations.

Educational tools and calculators enhance decision-making.

Employer responsibilities

Employers interested in offering a 457b plan must understand various responsibilities involved in plan management. This includes keeping track of employee contributions, ensuring compliance with regulations, and providing the right resources for employees to understand the plan.

To ensure the plan runs smoothly, employers should customize their support offerings based on employee needs, keeping the lines of communication open and clear. Best practices include keeping employment records accurate and staying updated on any changes in legislation affecting 457b plans.

Employers must maintain accurate records of contributions.

Compliance with state and federal regulations is critical.

Employers should offer tailored resources and support for participants.

Future of deferred compensation plans

The landscape of 457b deferred compensation plans is evolving, with new trends emerging in enrollment and contribution strategies. Legislative changes may be on the horizon, and these changes can directly affect how these plans function and what benefits they can offer to employees.

Insights from financial experts suggest that maximizing the benefits of a 457b plan will be increasingly important as the workforce changes. As more non-profit and governmental entities adapt to the needs of modern employees, 457b plans will likely become even more relevant in personal finance strategies.

Emerging trends indicate changing employer contributions and employee engagement.

Legislative changes may enhance or restrict plan offerings.

Increasing importance of 457b plans in modern financial strategies.

Interactive tools and examples

Providing practical examples and tools can significantly enhance understanding and engagement with the 457b deferred compensation plan. For instance, a sample completed 457b plan form can clarify how to properly fill it out based on real-world scenarios.

Interactive simulations that illustrate tax savings with deferred compensation can also help prospective participants visualize their future financial benefits. Furthermore, real-life case studies showcasing the success of various individuals who utilized a 457b plan can inspire confidence and provide valuable insights.

Sample completed forms serve as practical guides.

Tax savings simulations provide a visual representation of benefits.

Real-life case studies reveal the effectiveness of 457b plans.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I send 457b deferred compensation plan to be eSigned by others?

Once your 457b deferred compensation plan is complete, you can securely share it with recipients and gather eSignatures with pdfFiller in just a few clicks. You may transmit a PDF by email, text message, fax, USPS mail, or online notarization directly from your account. Make an account right now and give it a go.

How do I execute 457b deferred compensation plan online?

Easy online 457b deferred compensation plan completion using pdfFiller. Also, it allows you to legally eSign your form and change original PDF material. Create a free account and manage documents online.

How can I edit 457b deferred compensation plan on a smartphone?

You may do so effortlessly with pdfFiller's iOS and Android apps, which are available in the Apple Store and Google Play Store, respectively. You may also obtain the program from our website: https://edit-pdf-ios-android.pdffiller.com/. Open the application, sign in, and begin editing 457b deferred compensation plan right away.

What is 457b deferred compensation plan?

A 457b deferred compensation plan is a type of nonqualified retirement plan that allows employees, typically in government or certain nonprofit organizations, to defer receiving a portion of their income until a later date, such as retirement, while benefiting from tax advantages.

Who is required to file 457b deferred compensation plan?

Employers offering a 457b deferred compensation plan are required to file specific forms with the IRS, and the plan must comply with regulations set forth by the IRS to maintain tax-exempt status.

How to fill out 457b deferred compensation plan?

To fill out a 457b deferred compensation plan, participants typically need to complete an enrollment form provided by their employer, indicating the amount to be deferred, selecting investment options, and providing necessary personal information.

What is the purpose of 457b deferred compensation plan?

The purpose of a 457b deferred compensation plan is to help employees save for retirement by deferring a portion of their salary, allowing for tax-deferred growth and providing an additional savings vehicle alongside other retirement accounts.

What information must be reported on 457b deferred compensation plan?

Information that must be reported on a 457b deferred compensation plan includes participant contributions, employer contributions, account balances, distributions made, and other relevant plan details as required by the IRS.

Fill out your 457b deferred compensation plan online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

457b Deferred Compensation Plan is not the form you're looking for?Search for another form here.

Relevant keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.