Get the free Line of Credit Agreements

Show details

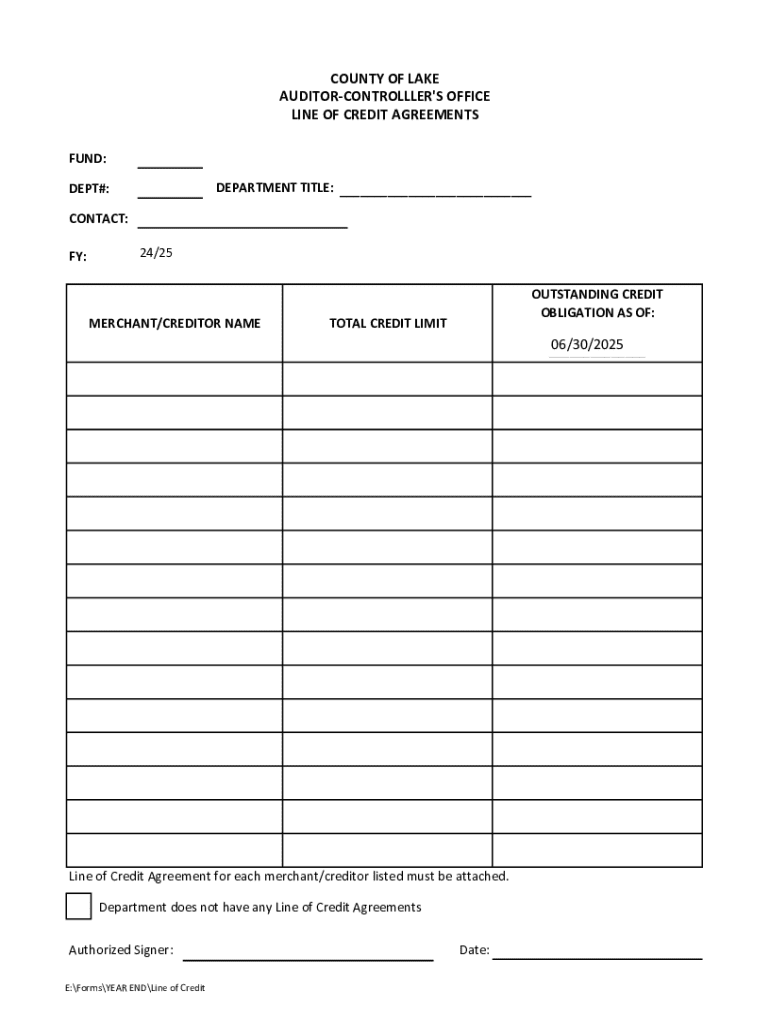

This document details the line of credit agreements for the County of Lake, specifying departments, outstanding obligations, and credit limits.

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign line of credit agreements

Edit your line of credit agreements form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your line of credit agreements form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing line of credit agreements online

Follow the steps down below to benefit from a competent PDF editor:

1

Set up an account. If you are a new user, click Start Free Trial and establish a profile.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit line of credit agreements. Add and change text, add new objects, move pages, add watermarks and page numbers, and more. Then click Done when you're done editing and go to the Documents tab to merge or split the file. If you want to lock or unlock the file, click the lock or unlock button.

4

Get your file. Select the name of your file in the docs list and choose your preferred exporting method. You can download it as a PDF, save it in another format, send it by email, or transfer it to the cloud.

With pdfFiller, it's always easy to work with documents. Try it!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out line of credit agreements

How to fill out line of credit agreements

01

Read the agreement thoroughly to understand the terms.

02

Gather necessary financial information including income and expenses.

03

Fill out personal information such as name, address, and contact details.

04

Provide details of your business if applicable, including business name and type.

05

Enter your requested credit limit.

06

Include any collateral information if required.

07

Review eligibility criteria and provide requested documentation.

08

Sign and date the agreement.

Who needs line of credit agreements?

01

Individuals seeking flexible access to funds for personal expenses.

02

Small business owners needing working capital for operations.

03

Homeowners looking to finance home improvements or major purchases.

04

Students needing financial support for education expenses.

05

Anyone requiring emergency funds or covering unexpected expenses.

Line of Credit Agreements Form: A Comprehensive Guide

Overview of line of credit agreements

A line of credit is a flexible loan option that allows borrowers to access funds up to a predetermined limit, giving them the ability to draw, repay, and borrow again as needed. This financial tool is not just a loan; rather, it provides a safety net, empowering users to meet various financial needs without having to reapply for new loans. For many, understanding the role of line of credit agreements is crucial to effectively managing personal finances.

The importance of a line of credit agreement lies in its capacity to offer immediate funding for expenses, smooth out fluctuations in cash flow, and allow for strategic financial planning. Common uses of this financial product include covering unexpected medical bills, financing home improvements, managing educational expenses, or even preparing for seasonal business shifts. By having a line of credit, individuals can maintain financial flexibility and respond quickly to opportunities or emergencies.

Emergency expenses such as medical bills or car repairs

Home renovations or repairs that require immediate funds

Educational costs, including tuition or books

Funding for seasonal expenses or business operations

Types of line of credit agreements

Line of credit agreements can vary significantly based on how they're secured and whether they revolve or not. Understanding the differences between secured and unsecured lines of credit is vital for borrowers. A secured line of credit is backed by an asset, such as a home or savings account, thereby reducing risk for lenders and often resulting in lower interest rates. Conversely, unsecured lines do not require collateral, making them riskier for lenders, which can lead to higher interest rates.

Additionally, revolving and non-revolving lines of credit offer disparate usage patterns. A revolving line of credit allows borrowers to repeatedly draw up to a limit, repay, and borrow against the same credit. A non-revolving agreement, however, is more fixed; once the borrowed amount is repaid, the credit does not refresh. Borrowers should consider their financial habits and needs before deciding which type of agreement aligns best with their circumstances.

Secured lines of credit: Often tied to valuable items, like homes, offering lower rates.

Unsecured lines of credit: Based on creditworthiness without collateral, resulting in higher interest.

Revolving lines of credit: Enable ongoing borrowing up to a limit as payments are made.

Non-revolving lines of credit: Once repaid, the line does not remain open for further borrowing.

Key components of a line of credit agreement

When entering a line of credit agreement, several essential terms should be clearly understood to avoid confusion in the future. The credit limit is a crucial figure that denotes the maximum amount you can borrow. Interest rates, which may be variable or fixed, determine how much you'll owe in addition to the principal. Lastly, repayment terms outline the schedule for making payments, including minimum payments and when they are due.

Important clauses in any line of credit agreement typically cover potential penalties for defaulting, the specific purposes for which you can use the funds, and the governing laws that dictate the agreement. Including a clear dispute resolution clause can also help protect both parties in the event of misunderstandings or disagreements.

Credit limit: The maximum amount available for borrowing.

Interest rates: The charges assessed on borrowed funds.

Repayment terms: Describing the schedule and requirements for payments.

Default clauses: Outlining penalties for missed payments.

Purpose of funds: Stipulating how the money can be used.

Governing law: The jurisdiction governing the agreement.

How to fill out a line of credit agreement form

Filling out a line of credit agreement form requires careful attention to ensure accuracy. Start by gathering necessary documents such as identification, income verification, and financial statements to provide clear insight into your financial position. Next, enter your personal and financial information accurately; this will include your name, address, income level, and employment details.

It’s essential to specify your desired credit limit and any specific terms that fit your repayment ability. Finally, review the agreement thoroughly to confirm all information is correct. A clear understanding of your responsibilities will culminate in signing the agreement confidently, knowing you have laid the groundwork for financial flexibility.

Gather documents: Identification, income verification, and financial statements.

Enter personal and financial information: Ensure accuracy and completeness.

Specify credit limit and desired terms: Align with your repayment capabilities.

Review agreement: Check for accuracy and understanding before signing.

Editing and managing your line of credit agreement

Once a line of credit agreement has been signed, the need for amendments may arise. Whether due to changing financial conditions or adjustments in your borrowing needs, knowing how to make amendments is crucial. Changing terms, such as adjusting the credit limit or altering repayment schedules, should be approached through formal channels established in the agreement. Always consult with your lender to comprehend any potential implications of changes.

Using pdfFiller for document management allows for seamless editing of your agreement. Features such as cloud storage, easy document sharing, and eSigning facilitate timely adjustments without the hassle of printing or mailing. This cloud-based solution provides an intuitive interface for users, making alterations to your agreement straightforward and efficient.

Contact lender for any amendments: Understand the process and implications.

Use pdfFiller for editing: Access your document anytime and make changes easily.

Review changes carefully: Ensure that any adjustments are clearly documented.

eSigning your line of credit agreement

The electronic signature process has revolutionized how agreements are finalized, offering convenience and speed. When using pdfFiller, the eSigning process is straightforward. Users can upload their document, add their signature, and send it for signing without the traditional delays associated with paper documents. This method not only speeds up the transaction but also allows for secure data handling.

Importantly, eSignatures are legally recognized in many jurisdictions, which adds a layer of trust and validity to your agreement. However, it’s crucial to verify local laws and regulations regarding electronic signatures to ensure compliance.

Upload the agreement to pdfFiller: Prepare your document for eSigning.

Add signature: Utilize pdfFiller's intuitive tools for an easy signing process.

Send for signing: Ensure all parties receive the document for their signatures.

Verify local eSignature laws: Confirm validity in your jurisdiction.

FAQs about line of credit agreements

When utilizing a line of credit agreement, questions often arise regarding implications and functions. A critical inquiry is what happens if one defaults on the agreement. Defaulting can lead to severe penalties, increased interest rates, or even legal action from the lender. It’s paramount to maintain consistent payments to avoid these pitfalls.

Another prevalent question is whether one can cancel a line of credit agreement. While cancellation may be possible, it generally requires following specific procedures mandated by the lender. Additionally, the differences between a line of credit agreement and a personal loan agreement can be significant; the former typically offers flexibility in borrowing and repayment, while the latter is more a straightforward, fixed loan.

What happens if you default? Likely penalties include increased rates or legal action.

Can you cancel? Follow lender procedures for cancellation.

Difference from personal loan: Lines of credit offer greater flexibility in borrowing.

Useful tools and resources

Managing a line of credit successfully also involves utilizing various tools available to help track expenses and repayments. An interactive calculator designed for line of credit costs can provide insights into what you'll be paying over time, helping you make informed financial decisions. pdfFiller also hosts a range of related templates, making it easier to access financial agreement forms when needed.

Beyond simple document creation, tools for monitoring and managing your line of credit can streamline your finances significantly. Regular oversight helps to prevent potential pitfalls such as overspending or missed payments.

Interactive calculator for assessment of line of credit costs.

Access to financial agreement templates on pdfFiller.

Tools for tracking expenses and managing repayments effectively.

Real-life applications and case studies

Understanding the practical applications of a line of credit can solidify its value as a financial product. Consider a case study where an individual utilized a line of credit effectively to manage unexpected home repairs. The homeowner faced a sudden plumbing issue, which required immediate attention but didn’t have sufficient savings. By accessing funds from their line of credit, they were able to resolve the issue quickly without incurring high-interest debit or credit card charges.

However, it’s important to highlight common pitfalls as well. Some individuals may use their line of credit indiscriminately, leading to spiraling debt. Awareness of these risks and strategic use can help prevent costly mistakes and ensure that the line of credit serves its purpose as a financial tool.

Case Study: Resolving unexpected home repairs through effective credit management.

Pitfalls: Indiscriminate use may lead to spiraling debt and financial strain.

Glossary of terms related to line of credit agreements

Navigating line of credit agreements involves understanding several financial and legal terms. Key financial terms include 'credit limit'—the maximum amount available for borrowing, and 'interest rate'—the percentage charged on borrowed amounts. Legal terminology, such as 'default', signifies failure to meet the contractual obligations of the agreement, which can have serious consequences.

Grasping these terms is essential for effectively engaging with creditors and ensuring compliance with the legal framework surrounding your agreement.

Credit limit: The total maximum amount you can borrow.

Interest rate: The cost of borrowing expressed as a percentage.

Default: When a borrower fails to meet their obligations.

Governing law: Legal framework under which the agreement operates.

Additional considerations

The impact of line of credit agreements on your credit score is a crucial aspect to keep in mind. Responsible management can enhance one’s credit score, while defaults or missed payments can result in significant declines. It's essential to monitor how utilization ratios affect your overall credit profile.

Also, being aware of market trends in line of credit options can offer broader insights into the financial landscape. As lenders adapt to economic conditions, increased competition may drive better terms and rates for borrowers, making it essential to stay informed.

Understand credit score impact: Manage responsibly to maintain good credit.

Stay informed on market trends: Adapt strategies to leverage improved lending options.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How do I modify my line of credit agreements in Gmail?

pdfFiller’s add-on for Gmail enables you to create, edit, fill out and eSign your line of credit agreements and any other documents you receive right in your inbox. Visit Google Workspace Marketplace and install pdfFiller for Gmail. Get rid of time-consuming steps and manage your documents and eSignatures effortlessly.

How can I send line of credit agreements for eSignature?

When you're ready to share your line of credit agreements, you can swiftly email it to others and receive the eSigned document back. You may send your PDF through email, fax, text message, or USPS mail, or you can notarize it online. All of this may be done without ever leaving your account.

How do I edit line of credit agreements straight from my smartphone?

You can easily do so with pdfFiller's apps for iOS and Android devices, which can be found at the Apple Store and the Google Play Store, respectively. You can use them to fill out PDFs. We have a website where you can get the app, but you can also get it there. When you install the app, log in, and start editing line of credit agreements, you can start right away.

What is line of credit agreements?

A line of credit agreement is a financial arrangement between a borrower and a lender that allows the borrower to access funds up to a specified limit, which can be used as needed and paid back over time.

Who is required to file line of credit agreements?

Borrowers, particularly businesses and individuals seeking to establish a line of credit, are required to file line of credit agreements to formalize the terms of the borrowing arrangement with the lender.

How to fill out line of credit agreements?

To fill out a line of credit agreement, the borrower must provide necessary information such as personal or business details, financial information, requested credit limit, collateral (if applicable), and agree to the terms and conditions specified by the lender.

What is the purpose of line of credit agreements?

The purpose of line of credit agreements is to provide flexibility and access to funds for borrowers, enabling them to manage cash flow, cover unexpected expenses, or finance projects as needed.

What information must be reported on line of credit agreements?

The information that must be reported on line of credit agreements includes the borrower’s identity, credit limit, repayment terms, interest rates, any fees, and details about collateral if required.

Fill out your line of credit agreements online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Line Of Credit Agreements is not the form you're looking for?Search for another form here.

Relevant keywords

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.