Get the free Mortgage and Home Equity Research Request

Show details

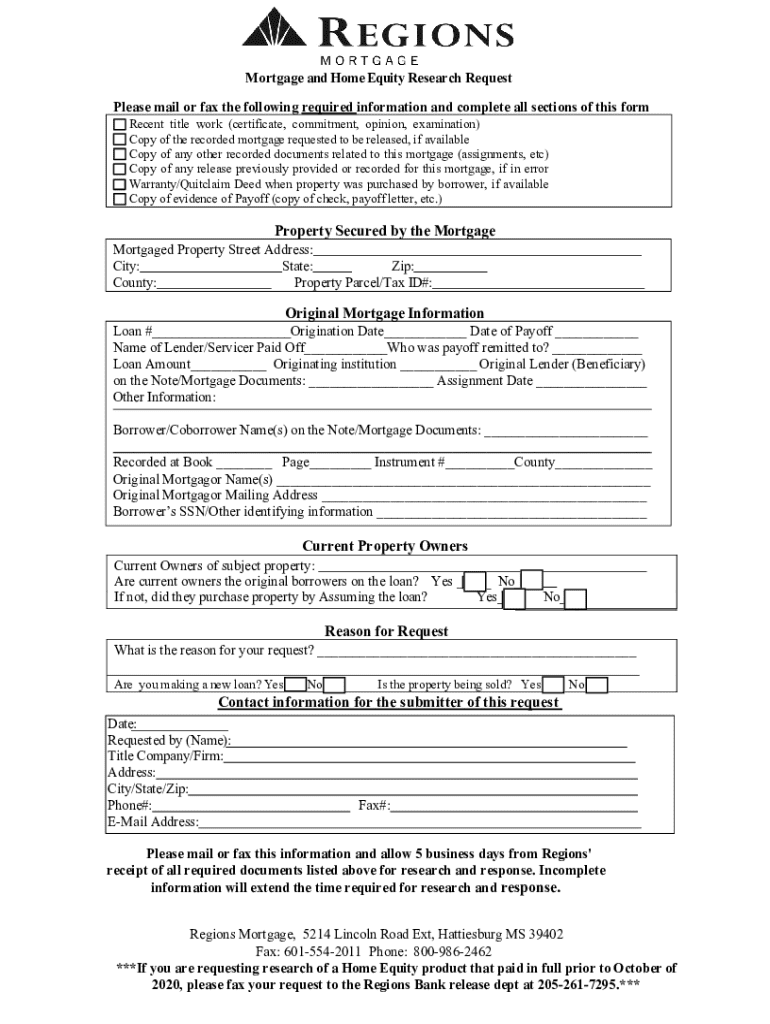

This document is a request form for mortgage and home equity research, requiring specific information and documentation related to a mortgage, including property details, original mortgage information,

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign mortgage and home equity

Edit your mortgage and home equity form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your mortgage and home equity form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit mortgage and home equity online

To use our professional PDF editor, follow these steps:

1

Create an account. Begin by choosing Start Free Trial and, if you are a new user, establish a profile.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit mortgage and home equity. Text may be added and replaced, new objects can be included, pages can be rearranged, watermarks and page numbers can be added, and so on. When you're done editing, click Done and then go to the Documents tab to combine, divide, lock, or unlock the file.

4

Get your file. When you find your file in the docs list, click on its name and choose how you want to save it. To get the PDF, you can save it, send an email with it, or move it to the cloud.

Dealing with documents is simple using pdfFiller.

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out mortgage and home equity

How to fill out mortgage and home equity

01

Gather financial documents including income statements, tax returns, and credit history.

02

Determine the amount you want to borrow and the type of mortgage or home equity loan you need.

03

Research and compare different lenders and their offered rates.

04

Complete the application form provided by your chosen lender, including personal and financial information.

05

Submit required documents and the application to the lender.

06

Undergo a credit check and property appraisal as part of the lender’s approval process.

07

Review the loan estimate provided by the lender, which outlines the terms of the mortgage or loan.

08

Finalize the details with the lender and prepare for the closing process.

09

Sign the necessary closing documents and fund the loan to complete the transaction.

Who needs mortgage and home equity?

01

First-time homebuyers who require financing to purchase a home.

02

Homeowners looking to refinance their current mortgage for a better interest rate.

03

Individuals seeking to access equity in their homes for large expenses such as renovations or education.

04

Investors looking to buy additional properties using leverage.

05

Those needing emergency funds for unexpected financial challenges.

Mortgage and home equity form: A how-to guide

Understanding mortgage and home equity forms

Mortgage forms are essential documents used in the borrowing process for purchasing a home. Their design can vary based on the type of mortgage or lender.

Common types of mortgage forms include fixed-rate, adjustable-rate, VA loans, and FHA loans. Each type has unique features and serves different borrower needs. Key components of these forms typically involve the loan amount, interest rate, repayment terms, and borrower details.

Home equity forms, conversely, focus on leveraging the existing equity in a homeowner’s property to secure additional financing. These forms can include home equity loans and lines of credit, allowing homeowners to tap into their asset value for financial needs.

Understanding both document types is crucial for any homeowner or prospective buyer, as they play a significant role in managing personal finances and maximizing property potential.

Key differences between mortgage and home equity forms

The first significant difference lies in the loan types and purposes. Mortgages are primarily used to purchase property, while home equity loans enable homeowners to borrow against their property's value. Essentially, mortgages help buyers enter the property market, whereas home equity loans assist homeowners in accessing funds without selling their property.

In terms of application processes, mortgage submissions typically involve more rigorous assessments, including credit checks and income verification, as lenders want to ensure borrowers can repay their loans. Home equity applications, although less stringent, still require property appraisal and credit evaluations to gauge the amount of equity that can be drawn.

Mortgages are used to purchase properties.

Home equity loans borrow against existing property value.

Mortgages require extensive documentation and checks.

Home equity forms may involve less stringent checks.

Preparing to fill out your mortgage form

Before starting to fill out your mortgage form, gather all necessary documentation. This typically includes recent income statements, tax returns, and statements of assets. Lenders will analyze this information to determine your eligibility.

Additionally, understanding your credit history is imperative. Your credit score plays a pivotal role in your application, affecting both the approval chances and the interest rates available to you. A higher credit score translates to better loan terms.

Gather income statements from the past two years.

Have your asset documentation ready, such as bank statements.

Review your credit history and score.

Step-by-step: filling out your mortgage form

Begin by filling out the basic information section, which usually requires personal details such as your name, address, and Social Security number. Ensure all information is accurately reported to avoid delays.

Next, move to the financial information section. This part covers your employment history and income sources, alongside any debts or assets you hold. Be honest about your financial situation; lenders appreciate transparency.

Continuing, provide thorough details about the property you wish to purchase, including its description and estimated value. Ensure that you also clarify the loan details, including desired amounts and specific loan terms that best suit your financial goals.

Fill out personal details in the basic information section.

Detail your income sources and employment in the financial section.

Provide a comprehensive description of the property.

Specify your desired loan amount and terms.

Step-by-step: filling out your home equity form

Before you begin, evaluate how much home equity you have available. Calculating home value minus outstanding mortgage balance will give you a comprehensive picture of your equity. This step is crucial to determine how much you can consider borrowing.

When completing the form, focus on key sections that detail your current mortgage information, the amount you wish to borrow, and the intended use for the funds. Many applicants falter by either undervaluing their equity or by misrepresenting the intended purpose for borrowing, which could lead to processing delays.

Evaluate your home equity before starting the form.

Include current mortgage information in your application.

Clearly state the amount you wish to borrow.

Indicate the intended use for the funds explicitly.

Interactive tools for managing your forms

Utilizing document editing tools can simplify the process of filling out mortgage and home equity forms. With features that allow for easy modifications and adjustments, these platforms enhance user experience and accuracy. Look for tools that offer templates specifically for mortgage and home equity forms, saving you time.

pdfFiller provides robust tools for document collaboration, making it easy to share forms securely. With eSigning capabilities, you can quickly finalize documents without the hassle of printing or scanning. Such functionalities not only streamline the process but also ensure you remain organized at every step.

Use editing tools to modify mortgage and home equity forms efficiently.

Take advantage of templates for quicker processing.

Utilize eSigning features for document finalization.

Reviewing and submitting your forms

Conducting a final review of your filled forms is essential before submission. Look out for any discrepancies in your information, including typos or missing details, as these can lead to significant delays in processing.

The submission process can vary by lender but generally involves submitting your forms electronically through their portal. Ensure you keep a copy of all submitted documents for your records, as they may be needed for follow-up inquiries.

Double-check all entries for accuracy.

Keep copies of submitted forms for your records.

Submit electronically through the lender's portal.

Common questions about mortgage and home equity forms

Many borrowers find themselves confused after a denial. If you’re denied, review the reasons provided by the lender. It's essential to address these issues before reapplying, as many common problems stem from credit scores or incomplete information.

Appealing a decision is possible, and understanding the lender’s criteria will help in formulating a robust case. Additionally, it’s important to know how to make updates or corrections to your forms after submission; generally, this process involves contacting your lender and providing the necessary documentation.

Understand reasons for denial before reapplying.

Consider formally appealing the lender's decision.

Know how to make updates after submission.

Managing your mortgage and home equity loans post-submission

After submitting your applications, it's essential to track their status actively. Many lenders provide online tools to check the progress of your application, which can significantly reduce anxiety during the waiting period.

Understanding the closing process is equally crucial. Once your application is approved, the process will typically lead to closing, where you'll finalize the details of the loan agreement and sign the necessary paperwork. Keep communication lines open with your lender during this period to facilitate a smooth closing process.

Use online tools to track application progress.

Understand the closing process after approval.

Maintain communication with your lender for a smooth transition.

Best practices for future home equity loans

Maintaining good credit is vital if you intend to apply for future home equity loans. Regularly monitor your credit score, pay bills on time, and keep your debt-to-income ratio low. These practices not only improve your chances of approval but also ensure you secure favorable interest rates.

When utilizing your home equity, approach it with caution. Use funds wisely for worthwhile investments or necessary expenses to avoid putting your home and financial future at risk. Remember, it’s crucial to ensure that your borrowing aligns with your long-term financial plans.

Regularly monitor your credit score and report.

Pay bills punctually to maintain a good credit standing.

Use home equity funds wisely for necessary investments.

Leveraging pdfFiller for a seamless document experience

pdfFiller stands out as a premier choice for document management, particularly for mortgage and home equity forms. Its platform enables users to create, edit, and manage documents efficiently from anywhere. The intuitive interface ensures that even those less familiar with technology can navigate through the document creation process seamlessly.

To maximize your experience with pdfFiller, use its collection of templates tailored for mortgage and home equity forms. This can significantly enhance your workflow, allowing you to focus on critical tasks without the hassle of formatting or design. With built-in tools for eSigning and collaboration, pdfFiller empowers users in their document management journey.

Utilize pdfFiller's templates for quick form creation.

Benefit from intuitive interface for ease of use.

Employ eSigning and collaboration tools effectively.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I manage my mortgage and home equity directly from Gmail?

You may use pdfFiller's Gmail add-on to change, fill out, and eSign your mortgage and home equity as well as other documents directly in your inbox by using the pdfFiller add-on for Gmail. pdfFiller for Gmail may be found on the Google Workspace Marketplace. Use the time you would have spent dealing with your papers and eSignatures for more vital tasks instead.

How do I edit mortgage and home equity in Chrome?

Install the pdfFiller Google Chrome Extension in your web browser to begin editing mortgage and home equity and other documents right from a Google search page. When you examine your documents in Chrome, you may make changes to them. With pdfFiller, you can create fillable documents and update existing PDFs from any internet-connected device.

Can I sign the mortgage and home equity electronically in Chrome?

You can. With pdfFiller, you get a strong e-signature solution built right into your Chrome browser. Using our addon, you may produce a legally enforceable eSignature by typing, sketching, or photographing it. Choose your preferred method and eSign in minutes.

What is mortgage and home equity?

A mortgage is a loan specifically used to purchase real estate, where the property serves as collateral for the loan. Home equity refers to the portion of a home that the owner truly owns outright; it's calculated by taking the current market value of the home and subtracting any outstanding mortgage balances.

Who is required to file mortgage and home equity?

Typically, individuals or entities who obtain a mortgage or take out a home equity loan are required to file the associated documentation. This includes homeowners who have borrowed against their home equity for various purposes.

How to fill out mortgage and home equity?

To fill out a mortgage or home equity application, one must provide personal information such as income, employment history, property details, and existing debts. This usually involves completing standardized forms provided by the lender.

What is the purpose of mortgage and home equity?

The purpose of a mortgage is to finance the purchase of real estate, allowing individuals to buy homes without paying the total price upfront. Home equity can be used for various financial needs, such as home renovations, debt consolidation, or funding education.

What information must be reported on mortgage and home equity?

Key information that must be reported includes the loan amount, interest rate, loan term, monthly payment, outstanding balance, property value, and any additional costs associated with the loan such as closing costs or insurance.

Fill out your mortgage and home equity online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Mortgage And Home Equity is not the form you're looking for?Search for another form here.

Relevant keywords

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.