Get the free Home Equity Line of Credit Application - Reliance Bank

Show details

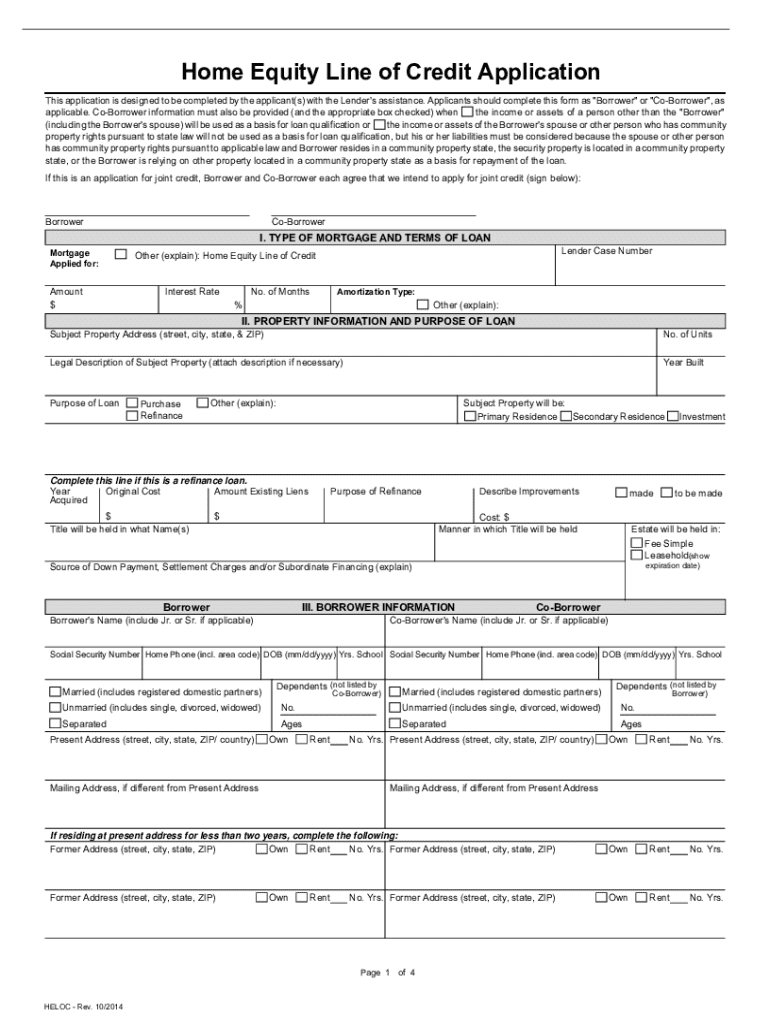

Wauchula State Bank, NMLS# 406389Home Equity Line of Credit Application This application is designed to be completed by the applicant(s) with the Lender\'s assistance. Applicants should complete this

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign home equity line of

Edit your home equity line of form online

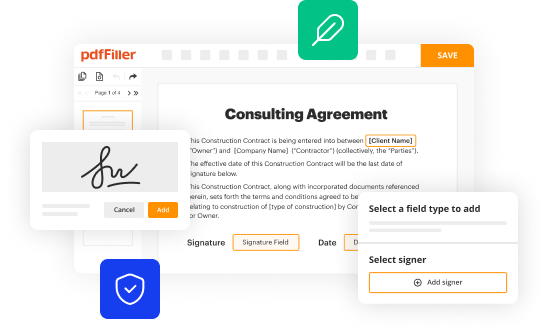

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your home equity line of form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing home equity line of online

Here are the steps you need to follow to get started with our professional PDF editor:

1

Log in. Click Start Free Trial and create a profile if necessary.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit home equity line of. Text may be added and replaced, new objects can be included, pages can be rearranged, watermarks and page numbers can be added, and so on. When you're done editing, click Done and then go to the Documents tab to combine, divide, lock, or unlock the file.

4

Get your file. Select your file from the documents list and pick your export method. You may save it as a PDF, email it, or upload it to the cloud.

With pdfFiller, it's always easy to work with documents. Try it!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out home equity line of

How to fill out home equity line of

01

Gather necessary documents: income proof, credit report, and property details.

02

Research lenders and compare home equity line of credit (HELOC) options.

03

Complete the application form provided by the lender.

04

Provide the required documentation to the lender.

05

Wait for the lender to assess your creditworthiness and property value.

06

Review the loan terms and conditions once the lender approves your application.

07

Sign the agreement and complete the closing process.

08

Access your line of credit as needed for expenses.

Who needs home equity line of?

01

Homeowners looking to finance large expenses such as home renovations.

02

Individuals seeking to consolidate high-interest debt.

03

People in need of funds for education or medical expenses.

04

Homeowners wanting to take advantage of their home's increased value.

Home equity line of form: A comprehensive how-to guide

Understanding home equity lines of credit (HELOCs)

A home equity line of credit (HELOC) is a revolving credit option that allows homeowners to borrow against the equity in their property. As a flexible financing solution, it operates similarly to a credit card, where you draw funds as needed up to a predetermined credit limit. Unlike traditional personal loans or fixed home equity loans that offer a lump sum, a HELOC allows you to withdraw funds during the draw period, which typically lasts 5 to 10 years.

Home equity refers to the market value of your home minus any outstanding mortgage balances. By leveraging this equity, borrowers can access cash for various purposes, such as home renovations, debt consolidation, or unexpected expenses. HELOCs generally have lower interest rates compared to unsecured loans, making them appealing for many homeowners.

Flexibility in borrowing: Withdraw as needed within the credit limit.

Lower interest rates compared to other unsecured loans.

Potential tax-deductible interest if used for home improvements.

Key terms and concepts

To navigate a home equity line of form successfully, it is crucial to understand key terms related to HELOCs. The credit limit is the maximum amount a lender approves for borrowing against your equity. The draw period is the time frame during which you can access funds, and the repayment period follows, during which you must pay back the borrowed amount. HELOCs typically offer variable interest rates, which can change over time based on market conditions, although some lenders might offer fixed-rate options.

The home equity line of form

The home equity line of form is an essential document for anyone looking to apply for a HELOC. This form serves as your official application to the lender, providing all the necessary details they require to evaluate your financial health and equity position. Completing this form accurately can expedite the approval process and improve your chances of securing a favorable line of credit.

Key components of the form often include personal information, current mortgage details, and financial credentials. This will include specifics like your income, existing debts, and the purpose for which you'll use the line of credit. Before filling out the home equity line of form, gather all relevant documents and information to streamline the process and minimize errors.

Where to find the home equity line of form

Accessing the home equity line of form is simple. You can easily download or access this form through online platforms like pdfFiller. It’s essential to ensure you’re using official sources to prevent potential fraud or errors. Look for authorized lenders or financial institutions that provide necessary documentation on their websites.

Step-by-step guide to filling out the home equity line of form

When preparing to fill out the home equity line of form, it's beneficial to approach it in a structured manner. Here’s a breakdown of the key sections:

Personal Information: Include your full name, address, and contact details.

Financial Information: Disclose your total income, existing debts, assets, and liabilities for a clear picture of your financial standing.

Property Details: Provide information on your current mortgage status and remaining balance, along with a brief description of the property.

HELOC Specifics: Indicate the desired line of credit amount and its intended use, while selecting draw and repayment terms.

Filling out this form requires attention to detail and honesty. Ensure all information is accurate to prevent delays. Common pitfalls include omitting relevant information or providing inaccurate data, so double-check everything before submission. You can utilize tools on pdfFiller for auto-fill features and digital signatures to enhance efficiency.

Managing your home equity line of credit

Once your HELOC has been approved, managing it wisely is critical. You gain the flexibility to draw against your line of credit as needed, but it's vital to monitor the variable interest rates closely, as they can fluctuate based on the market. Managing your withdrawals with a clear strategy can help you avoid overextending your financial obligations.

Responsible use of your HELOC is crucial. It is essential to establish a budget and avoid treating it as a long-term solution to financial difficulties. Use it for planned projects or solid financial opportunities; this will help maintain your financial health. Watch for key indicators like your ability to manage repayments, your credit utilization, and overall financial stability.

Repayment strategies

Planning how to repay your HELOC should begin as soon as you draw funds. Many borrowers opt for the interest-only payment during the draw period but must prepare for the transition into full repayment later. Consider paying back more than the minimum whenever possible, as this reduces interest costs over time.

Reassessing your position regularly can provide options for refinancing or even paying off your HELOC early if financial situations change. Keep tabs on current interest rates and evaluate if it’s more beneficial to consolidate or refinance for lower payments.

Benefits of utilizing pdfFiller for your home equity line of form

pdfFiller stands out as an invaluable resource when it comes to managing your home equity line of form. The user-friendly interface equips individuals and teams with interactive tools and templates designed for seamless document management. With cloud access, users can edit, sign, and collaborate on their forms anytime, anywhere.

Collaboration features allow you to work with financial advisors or team members effectively. Real-time updates and document-sharing capabilities mean you can receive feedback swiftly and stay organized throughout the application process. This ensures that the information submitted is accurate and up-to-date, enhancing your overall financial strategy.

Comprehensive document management

Additionally, pdfFiller offers secure storage and retrieval options for all your completed forms. The ability to utilize digital backups ensures you won’t lose vital documents, especially when managing multiple loans or credits. Ongoing access to your documents makes tracking your financial health and commitments through your HELOC straightforward.

Additional insights and resources

Navigating the nuances of a home equity line of credit can raise questions. Some common FAQs include understanding how interest rates are determined or whether HELOC interest may be tax-deductible. Addressing these queries can lead to informed financial decision-making.

Further, there are numerous articles and guides available on pdfFiller about related topics such as home equity management, credit utilization, and financial planning strategies. Utilizing these resources can deepen your understanding of your financial options and help you make informed decisions concerning your home equity line of credit.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How do I make changes in home equity line of?

With pdfFiller, it's easy to make changes. Open your home equity line of in the editor, which is very easy to use and understand. When you go there, you'll be able to black out and change text, write and erase, add images, draw lines, arrows, and more. You can also add sticky notes and text boxes.

How do I edit home equity line of in Chrome?

Install the pdfFiller Chrome Extension to modify, fill out, and eSign your home equity line of, which you can access right from a Google search page. Fillable documents without leaving Chrome on any internet-connected device.

How do I fill out the home equity line of form on my smartphone?

Use the pdfFiller mobile app to fill out and sign home equity line of. Visit our website (https://edit-pdf-ios-android.pdffiller.com/) to learn more about our mobile applications, their features, and how to get started.

What is home equity line of?

A home equity line of credit (HELOC) is a revolving line of credit that allows homeowners to borrow funds against the equity in their home, typically at variable interest rates.

Who is required to file home equity line of?

Homeowners who have taken out a home equity line of credit may be required to file, especially if they itemize deductions on their tax returns or if the funds are used for significant home improvements.

How to fill out home equity line of?

To fill out a home equity line of credit application, provide personal information, details about your income, the value of your home, existing mortgage information, and specify estimated borrowings.

What is the purpose of home equity line of?

The purpose of a home equity line of credit is to provide borrowers with access to funds for expenses such as home improvements, debt consolidation, education costs, or other financial needs.

What information must be reported on home equity line of?

Information that must be reported includes the amount borrowed, the date the line was established, the terms of the credit line, and interest paid during the tax year.

Fill out your home equity line of online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Home Equity Line Of is not the form you're looking for?Search for another form here.

Relevant keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.