Get the free Home Mortgage Disclosure Act Flashcards

Show details

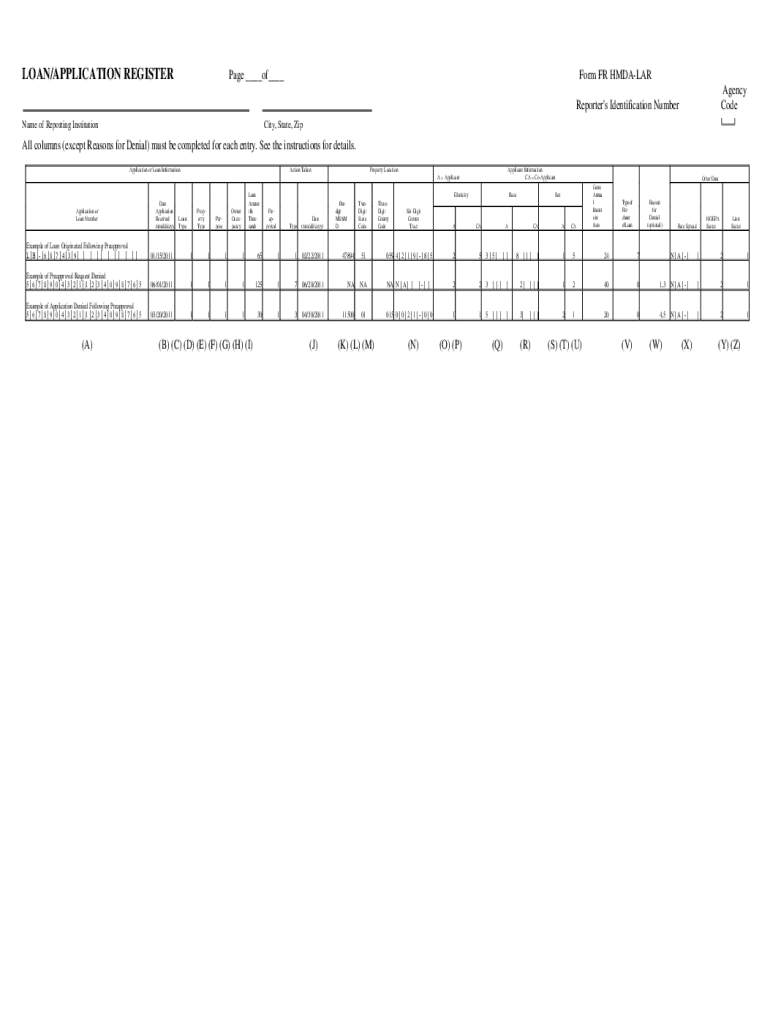

LOAN/APPLICATION REGISTERPage ___of___Form FR HMDALAR Agency CodeReporter\'s Identification Number Name of Reporting InstitutionCity, State, ZipAll columns (except Reasons for Denial) must be completed

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign home mortgage disclosure act

Edit your home mortgage disclosure act form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your home mortgage disclosure act form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit home mortgage disclosure act online

Here are the steps you need to follow to get started with our professional PDF editor:

1

Log in. Click Start Free Trial and create a profile if necessary.

2

Simply add a document. Select Add New from your Dashboard and import a file into the system by uploading it from your device or importing it via the cloud, online, or internal mail. Then click Begin editing.

3

Edit home mortgage disclosure act. Rearrange and rotate pages, add new and changed texts, add new objects, and use other useful tools. When you're done, click Done. You can use the Documents tab to merge, split, lock, or unlock your files.

4

Save your file. Select it from your records list. Then, click the right toolbar and select one of the various exporting options: save in numerous formats, download as PDF, email, or cloud.

It's easier to work with documents with pdfFiller than you could have believed. You may try it out for yourself by signing up for an account.

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out home mortgage disclosure act

How to fill out home mortgage disclosure act

01

Obtain the Home Mortgage Disclosure Act (HMDA) data collection guidelines.

02

Determine the applicable loan types that fall under HMDA reporting requirements.

03

Fill out the necessary information regarding the loan originator, borrower, and property details.

04

Include data on the applicant's race, ethnicity, and sex, ensuring that it is voluntarily provided.

05

Document the loan amount, the purpose of the loan, and the loan's location.

06

Submit the completed HMDA data to the appropriate regulatory authority within the specified deadline.

Who needs home mortgage disclosure act?

01

Lending institutions such as banks and credit unions that engage in residential mortgage lending.

02

Financial institutions that accept deposits and have at least one branch in a metropolitan statistical area (MSA).

03

Institutions that make loans for home purchases, home improvement, or refinancing.

Understanding the Home Mortgage Disclosure Act Form: A Comprehensive Guide

Understanding the Home Mortgage Disclosure Act (HMDA)

The Home Mortgage Disclosure Act (HMDA) was enacted to provide transparency in the lending process by ensuring that lenders disclose certain information about mortgage applications. Its primary purpose is to promote fair lending and ensure that financial institutions serve the housing needs of their communities.

For consumers, HMDA data can help in understanding lending patterns within their communities, thereby facilitating informed decisions while applying for mortgages. Lenders benefit from HMDA as it helps them identify potential biases in their lending practices, ensuring compliance with fair lending laws.

Supporting fair lending practices through transparency.

Providing valuable insights into mortgage activity in specific communities.

Helping regulators enforce policies that prevent discriminatory lending.

The Home Mortgage Disclosure Act form explained

The HMDA form is a standardized document that lenders must fill out when they process mortgage applications. This form collects essential data that regulators analyze to ensure compliance with lending laws. Financial institutions that meet specific thresholds regarding the number of loans issued are typically required to complete the HMDA form.

The information collected through the HMDA form helps assess lending patterns and informs policymakers about mortgage applications. This data includes not only details about the loans—such as the loan type and amounts—but also applicant demographics and geographical data to ensure equal access to credit across all communities.

Details about the loan including type, amount, and terms.

Demographic information such as race, ethnicity, and gender of applicants.

Geographical specifics regarding census tracts and locations.

Filling out the HMDA form

Completing the HMDA form may seem daunting, but with proper preparation, it becomes manageable. Begin by gathering necessary documentation like loan applications, applicant demographics, and geographical data. A clear and organized approach will help ensure each section of the HMDA form is filled out accurately.

The HMDA form consists of several sections. Each section has specific data requirements, so take your time to review what is needed. Pay close attention to detail, ensuring that the information matches your documentation. This diligence will help avoid common errors that could lead to compliance issues.

Gather all necessary supporting documentation before starting.

Take a moment to understand the layout and requirements of each form section.

Double-check the accuracy of the data entered before submission.

Common mistakes to avoid

One of the most common mistakes when filling out the HMDA form is providing incomplete information. Ensure all required fields are filled, as leaving something blank may trigger compliance issues. Misinterpretation of data requirements can also pose a problem; be sure to understand what information is needed for each category.

Also, be cautious of date formats and specific terminology. Employing uniform language and formats can prevent confusion and ensure accuracy. When in doubt, consult HMDA guidelines or resources available through platforms like pdfFiller to clarify any uncertainties.

Tools for managing your HMDA form

Utilizing tools like pdfFiller can streamline the process of filling out HMDA forms. This platform allows users to edit, sign, and collaborate seamlessly on PDF documents. Its cloud-based capabilities mean you can manage your forms anywhere, making it particularly convenient for teams working together on compliance projects.

Features like electronic signatures and document editing allow for a more efficient workflow. With these digital tools, there's no need to print and scan documents, saving you time and reducing the risk of errors during manual handling.

Edit and customize the HMDA form directly within the platform.

Utilize e-signature capabilities for faster approvals.

Collaborate on documents in real-time with your team.

Submission process for the HMDA form

Submitting your HMDA form is crucial for compliance and must be done correctly. Electronic submission is the preferred method, allowing for instant processing. Detailed instructions are typically provided by regulatory authorities on the submission portal. Ensure that you follow these guidelines carefully to avoid any delays.

Alternately, some lenders may have the option to submit forms by mail or other methods. If so, adhere strictly to the provided timelines and instructions for alternative submissions. Always keep a record of your submission, including any confirmation details, to track the status of your submission.

Follow the provided guidelines on electronic submission portals.

Consider alternative methods only if electronic submission is not an option.

Retain records and confirmation of your submission for future reference.

Tracking your submission

Once your HMDA form is submitted, you may wish to confirm its receipt. Most submission portals will provide a confirmation message or receipt, so pay attention to these details after submission. It’s imperative to understand response timelines set by regulatory authorities to manage your expectations regarding any follow-up requirements.

In case you do not hear back within the expected timelines, follow up with the appropriate regulatory office to ensure your submission was received and processed. This proactive approach ensures that you remain compliant and aware of any follow-up actions necessary.

Implications of HMDA data

Investing in proper compliance with the HMDA form prevents discriminatory lending and promotes fair practices across the mortgage market. HMDA data is deeply influential as it informs policymakers regarding lending patterns and helps anticipate housing needs within various communities. Understanding how this data is used is integral to grasping the larger picture of mortgage dynamics in the U.S.

Official bodies utilize HMDA reports to monitor trends over time, ensuring that lending is equitable. By analyzing HMDA trends, stakeholders—including consumers—can advocate for better access to credit in underserved communities, thus enhancing broader economic stability.

Monitoring and policy-making to prevent discriminatory practices.

Fostering accountability in lending patterns by banks and institutions.

Providing essential data that reflects community housing needs.

Updates and changes to HMDA regulations

HMDA regulations have undergone significant revisions to enhance transparency and effectiveness. Understanding these changes is crucial for lenders and borrowers alike, as they affect reporting requirements and compliance obligations. For example, adjustments to the data fields collected can influence how lenders assess and document applicant information.

These evolving regulations highlight the importance of staying informed about potential changes in compliance requirements. Maintaining awareness through resources, such as pdfFiller's guidance, ensures that both lenders and consumers can navigate the landscape effectively and remain compliant with any new standards.

Stay updated with significant revisions to HMDA guidelines.

Understanding the implications of these changes for your compliance strategy.

Engage with educational resources to enhance knowledge over time.

Future outlook for HMDA compliance

The future of HMDA compliance is likely to involve increased scrutiny and tighter regulations. As data privacy becomes a paramount concern, stakeholders will need to ensure borrower information is handled with care while still meeting disclosure requirements. Ongoing education will play a vital role in keeping lenders informed about new expectations and providing consumers with the knowledge they need to uphold their rights.

By prioritizing transparency and accountability, the mortgage industry can better align itself with the community's needs. Therefore, continuous evolution in HMDA regulations will help ensure that fair lending practices remain at the forefront of the conversation in the housing market.

Frequently asked questions (FAQs) about the HMDA form

General FAQs

Understanding the HMDA form often comes with questions surrounding its purpose and requirements. Common misconceptions include the belief that only certain types of loans require reporting. In reality, any mortgage application from a covered lender is subject to HMDA reporting, which helps build a comprehensive view of loan activity across various demographics.

Another frequent question pertains to what happens if errors are found post-submission. Addressing mistakes promptly is essential, as lenders may need to revise submitted data to correct any inaccuracies, ensuring their compliance standing isn't compromised.

Specific scenarios and applications

When considering unique case examples, individuals may wonder if all applicants need to self-identify their demographic information. While borrowers are encouraged to provide this information, there are options for applicants to decline to answer without impacting their application negatively.

Another scenario involves utilizing the HMDA form for joint applications. Understanding lender policies on joint applications is crucial, as these may vary. It's advisable to check with specific lenders for their practices regarding combined applicant data on the HMDA form.

Getting support and assistance

Navigating the complexities of the HMDA form can be overwhelming, but various resources are available to provide guidance. The Consumer Financial Protection Bureau (CFPB) is an official source that offers comprehensive guidelines and explanations regarding the HMDA form requirements.

Further, utilizing digital platforms like pdfFiller can ease data entry challenges and enhance document management practices. If necessary, consulting with professionals who specialize in regulatory compliance can provide additional assurance regarding your HMDA reporting processes.

Utilize the CFPB as a resource for HMDA guidelines.

Leverage pdfFiller to simplify document management.

Consider engaging professionals when complex questions arise.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I send home mortgage disclosure act for eSignature?

home mortgage disclosure act is ready when you're ready to send it out. With pdfFiller, you can send it out securely and get signatures in just a few clicks. PDFs can be sent to you by email, text message, fax, USPS mail, or notarized on your account. You can do this right from your account. Become a member right now and try it out for yourself!

Where do I find home mortgage disclosure act?

The pdfFiller premium subscription gives you access to a large library of fillable forms (over 25 million fillable templates) that you can download, fill out, print, and sign. In the library, you'll have no problem discovering state-specific home mortgage disclosure act and other forms. Find the template you want and tweak it with powerful editing tools.

How do I make edits in home mortgage disclosure act without leaving Chrome?

Install the pdfFiller Chrome Extension to modify, fill out, and eSign your home mortgage disclosure act, which you can access right from a Google search page. Fillable documents without leaving Chrome on any internet-connected device.

What is home mortgage disclosure act?

The Home Mortgage Disclosure Act (HMDA) is a U.S. law that requires financial institutions to collect and disclose data about mortgage applications to help ensure compliance with fair lending laws.

Who is required to file home mortgage disclosure act?

Lenders that meet certain thresholds, including depository institutions and non-depository mortgage lenders, are required to file the Home Mortgage Disclosure Act data.

How to fill out home mortgage disclosure act?

To fill out the HMDA data, lenders must collect specific data fields related to mortgage applications and approvals, and submit it through the appropriate reporting channels to the regulatory authority.

What is the purpose of home mortgage disclosure act?

The purpose of the HMDA is to promote transparency in mortgage lending, help identify discriminatory lending practices, and ensure that lenders serve the housing needs of their communities.

What information must be reported on home mortgage disclosure act?

Lenders must report information such as the loan amount, property location, race, ethnicity, gender of applicants, loan outcomes, and other relevant details regarding mortgage applications.

Fill out your home mortgage disclosure act online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Home Mortgage Disclosure Act is not the form you're looking for?Search for another form here.

Relevant keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.