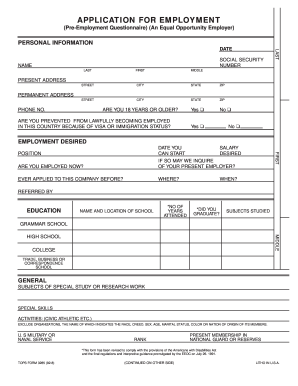

Equal Credit Opportunity Act Sample Notification Form Templates

What are Equal Credit Opportunity Act Sample Notification Form Templates?

Equal Credit Opportunity Act Sample Notification Form Templates are standardized forms that notify individuals of their rights under the Equal Credit Opportunity Act. These forms provide information on the discrimination protections offered by the Act and how individuals can take action if they believe they have been discriminated against in credit transactions.

What are the types of Equal Credit Opportunity Act Sample Notification Form Templates?

There are several types of Equal Credit Opportunity Act Sample Notification Form Templates available, including but not limited to:

How to complete Equal Credit Opportunity Act Sample Notification Form Templates

To complete an Equal Credit Opportunity Act Sample Notification Form Template, follow these simple steps:

pdfFiller empowers users to create, edit, and share documents online. Offering unlimited fillable templates and powerful editing tools, pdfFiller is the only PDF editor users need to get their documents done.