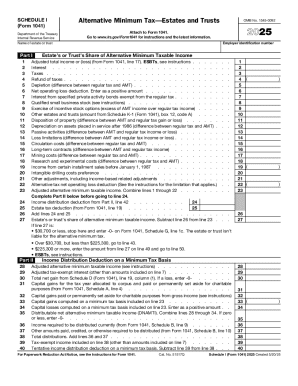

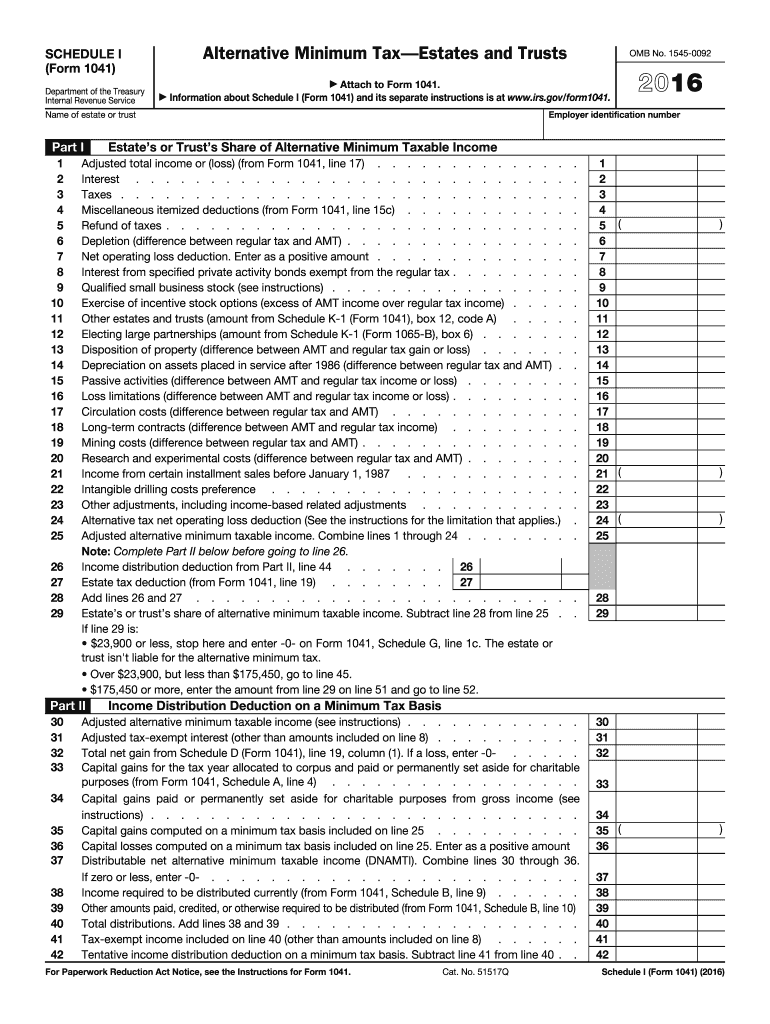

IRS 1041 - Schedule I 2016 free printable template

Get, Create, Make, and Sign IRS 1041 - Schedule I

Instructions and Help about IRS 1041 - Schedule I

How to edit IRS 1041 - Schedule I

How to fill out IRS 1041 - Schedule I

About IRS 1041 - Schedule I 2016 previous version

What is IRS 1041 - Schedule I?

Who needs the form?

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about IRS 1041 - Schedule I

How can I correct mistakes on my submitted 2016 estates form?

If you've identified an error on your 2016 estates form after submission, you may file an amended form. Clearly indicate the changes and ensure that you address any specific areas that were incorrect. This process helps update the information with the authority effectively while maintaining compliance.

What should I do if I receive a notice regarding my 2016 estates form?

Receiving a notice can indicate a request for more information or an audit. Carefully review the notice and prepare the necessary documentation that supports your filings. Respond promptly to the notice, ensuring you meet any deadlines specified.

Can I e-file the 2016 estates form, and what should I know about software compatibility?

Yes, you can e-file the 2016 estates form. It’s important to ensure that you are using compatible software or online platforms to avoid rejections. Check the technical requirements for e-filing to ensure a smooth submission process.

What are the common errors to avoid when filing the 2016 estates form?

Common errors when filing the 2016 estates form include incorrect taxpayer identification numbers and mismatched information between forms. Double-check all data entries to prevent delays or rejections, and consider having a second party review your submission.

What is the record retention period for the 2016 estates form after filing?

After submitting the 2016 estates form, you should retain records for at least three years. This allows you to provide adequate documentation in case of an audit or if any discrepancies arise following your submission.