Get the free Mortgage Crisis: Exploring Incentives Prevalent During the Boom and Bust of the 2001...

Show details

Este trabajo de maestra explica el comportamiento del mercado hipotecario entre 2001 y 2007, discutiendo los incentivos econmicos que enfrentaron los participantes clave del mercado y analizando cmo

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign mortgage crisis exploring incentives

Edit your mortgage crisis exploring incentives form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your mortgage crisis exploring incentives form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit mortgage crisis exploring incentives online

To use the services of a skilled PDF editor, follow these steps:

1

Register the account. Begin by clicking Start Free Trial and create a profile if you are a new user.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit mortgage crisis exploring incentives. Replace text, adding objects, rearranging pages, and more. Then select the Documents tab to combine, divide, lock or unlock the file.

4

Save your file. Select it from your list of records. Then, move your cursor to the right toolbar and choose one of the exporting options. You can save it in multiple formats, download it as a PDF, send it by email, or store it in the cloud, among other things.

With pdfFiller, it's always easy to work with documents. Check it out!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out mortgage crisis exploring incentives

How to fill out mortgage crisis exploring incentives

01

Gather necessary financial documents, including income statements and credit reports.

02

Research available incentive programs that address mortgage crisis situations.

03

Evaluate eligibility criteria for each program to identify suitable options.

04

Complete application forms for selected incentive programs, ensuring all information is accurate and up-to-date.

05

Submit documentation required by the program, including proof of hardship if applicable.

06

Follow up with program administrators to check the status of your application and provide any additional information if requested.

07

Attend counseling sessions if required, to fully understand the implications of the incentives and options available.

Who needs mortgage crisis exploring incentives?

01

Homeowners facing difficulties in making mortgage payments due to financial hardship.

02

Individuals seeking to avoid foreclosure and explore alternatives.

03

Real estate professionals assisting clients navigating the mortgage crisis.

04

Non-profit organizations aiming to support at-risk homeowners.

05

Government agencies looking to implement or promote mortgage assistance programs.

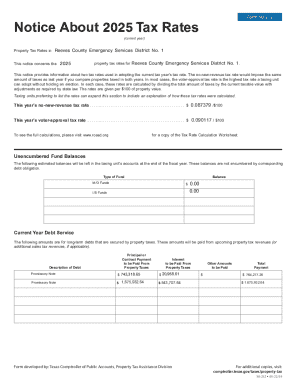

Mortgage crisis exploring incentives form

Understanding the mortgage crisis

The mortgage crisis, often referred to as the subprime mortgage crisis, represents a significant turning point in the history of finance and the housing market. It primarily emerged in the United States in the late 2000s, erupting into a global financial crisis that drastically altered economic landscapes worldwide. At its core, the crisis was characterized by a surge in home foreclosures and sharp declines in housing prices, which resulted from an unsustainable rise in mortgage lending practices.

Key factors that contributed to the mortgage crisis include the proliferation of subprime loans, the aggressive packaging of mortgage-backed securities, and rampant speculation in housing prices. As lenders relaxed their underwriting standards, borrowing became easier for individuals with poor credit histories. This trend perpetuated a dangerous cycle where borrowers took on loans they could not afford, leading to widespread defaults and ultimately triggering a market collapse.

Proliferation of subprime loans increased risk in the housing market.

Aggressive securitization of mortgages created complex financial products.

Speculative investments inflated house prices beyond sustainable levels.

The historical context surrounding the rise and fall of the housing market is essential for understanding the crisis. In the early 2000s, low-interest rates, combined with lax lending standards, fueled a housing boom. However, as interest rates began to rise, many adjustable-rate mortgages reset at higher rates, further exacerbating the financial strain on borrowers.

The role of incentives in the mortgage market

Incentives in the mortgage lending space significantly influence the behavior of lenders and borrowers alike. In essence, incentives refer to the various motivators that guide the actions of market participants. For lenders, these incentives often manifest in financial forms, encouraging them to either approve or reject mortgage applications based on potential profit margins.

Common types of financial incentives for lenders include interest rate adjustments, loan origination fees, and various subsidies or grants. For instance, lenders may offer lower interest rates to attract borrowers or charge higher origination fees to boost short-term revenue. Understanding these incentives is crucial, as they shape the lending landscape by determining who qualifies for loans, how much they pay, and ultimately, if they can maintain their mortgage obligations.

Interest rate adjustments can make loans more attractive or restrictive based on market conditions.

Loan origination fees directly impact lender revenue and borrower expenses.

Subsidies and grants can encourage lenders to extend credit to high-risk borrowers.

Behavioral economics plays a pivotal role in understanding how these incentives impact lender decisions. As lenders respond to potential profitability, their decision-making processes may inadvertently increase systemic risks. Thus, examining lender behavior in light of these incentives becomes imperative to develop strategies for mitigating future crises.

Exploring the impact of incentives on borrowers

The effects of lender incentives on borrowers are multifaceted, presenting both advantages and disadvantages. While incentives can provide opportunities for borrowers to access financing, they can also lead to unintended consequences. For example, aggressive lending practices might allow unqualified borrowers to secure loans, but this often results in elevated risks of foreclosure when they cannot repay.

Borrowers equipped with knowledge about these incentives often fare better in navigating the complex mortgage landscape. Understanding how incentives vary can alter the borrower experience significantly, impacting everything from loan terms to overall satisfaction. For instance, in markets where lenders prioritize fast processing over thorough evaluation, borrowers may find themselves trapped in unfavorable loan terms due to rushed decision-making.

Pros of lender incentives include increased access to mortgage funding for underserved demographics.

Cons include the risk of predatory lending practices targeting vulnerable borrowers.

Awareness of incentives allows borrowers to negotiate better loan terms.

Case studies highlighting borrower outcomes in various incentive scenarios reveal a stark contrast in experiences based on the market environment and lender strategies. In areas with more stringent lending standards, for example, borrowers experienced lower rates of default but also faced barriers to homeownership. Conversely, lax standards increased accessibility but raised concerns about long-term stability as evidenced by soaring foreclosure rates.

The fire sales phenomenon

Fire sales, characterized by the rapid liquidation of assets at below-market prices, have significant implications for the financial system, particularly during crises. When lenders face increased numbers of foreclosures, they often resort to fire sales to mitigate losses on their balance sheets. This triggers a downward spiral in asset prices, further eroding homeowner equity and trust in the market.

Lender incentives can inadvertently lead to fire sales, particularly when profit motives overshadow long-term stability. For example, a lender facing mounting defaults may prioritize quick cash recovery over a cautious, measured approach, exacerbating market fragility. The resulting rapid liquidation often yields a significant number of distressed sales, which in turn impacts the entire benefit structure of mortgages.

Fire sales can lead to cascading effects in the housing market, impacting overall stability.

Short-term recovery efforts may mask underlying systemic risks in the mortgage market.

Long-term outcomes of fire sales often include a lack of trust and increased resistance to lending.

To effectively address this phenomenon, policymakers must consider the broader economic repercussions of incentivizing rapid asset sales versus sustainable recovery programs. Striking a balance between short-term recovery and long-term stability is vital for reintegrating resilience into the housing market.

The role of government regulations

Government regulations aimed at curbing the excesses of the mortgage crisis illustrate the delicate balance between necessary oversight and excessive intervention. Since the crisis, various regulatory responses have been implemented, designed to stabilize the housing market and protect consumers from unscrupulous lending practices. These initiatives are often accompanied by specific incentives that encourage compliance among lenders.

However, these incentives can be a double-edged sword. While they aim to steer lenders towards more responsible practices, they can inadvertently create an environment where compliance becomes more about meeting regulatory requirements than fostering genuine credit access. For instance, the Dodd-Frank Act established oversight mechanisms that scrutinize lending practices but may also impose burdensome compliance costs on lenders, which could ultimately be passed onto borrowers.

Regulatory responses aim to prevent predatory lending and promote market stability.

Compliance incentives can lead to a checkbox mindset rather than true accountability.

Well-structured regulations can enhance trust in the mortgage system, benefiting consumers.

The evolving nature of regulations shapes both lender and borrower behavior, influencing everything from interest rates to loan terms. Continuous evaluation of these incentives within regulatory frameworks remains vital for fostering a lending environment that supports sustainable growth and protects at-risk borrowers.

Evaluating the effectiveness of current incentives

Assessing the effectiveness of current mortgage incentives requires a thorough analysis of various metrics. Key performance indicators might include foreclosure rates, loan accessibility, borrower satisfaction, and overall market stability. By examining these metrics, stakeholders can glean insights into which incentive structures are yielding the most favorable outcomes and which are failing to meet their intended goals.

Success stories emerge from regions that adopted effective incentives leading to market stabilization. For example, certain community programs encouraging responsible lending and reducing risks of foreclosures have demonstrated how targeted incentives can create positive cycles in local economies, bolstering both lenders and borrowers.

Comparative analysis of foreclosure rates pre- and post-incentive implementation can highlight efficacy.

Borrower feedback can provide qualitative insights into the success of incentive programs.

A holistic approach to evaluating incentives ensures that all stakeholder perspectives are considered.

Nevertheless, areas exist for improvement based on lessons learned from the crisis. Stakeholders must prioritize transparency in incentive structures while remaining vigilant against complacency which can allow systemic vulnerabilities to re-emerge. Continuous dialogue and adaptation are crucial to safeguard the mortgage market against potential downturns.

Interactive tools for managing mortgage documents

In today’s digitally driven landscape, managing mortgage documents efficiently is more critical than ever. Interactive tools like those provided by pdfFiller can streamline the document management process, ensuring that both lenders and borrowers maintain clear and precise records of their transactions. Understanding the essentials of document management can significantly enhance the operational efficiency of mortgage transactions.

Features of the pdfFiller platform empower users to create, edit, sign, and share documents effortlessly. For example, seamless PDF editing allows users to modify documents directly, while eSigning capabilities ensure authenticity without the need for physical interaction. Collaboration tools also enhance team communication, allowing for smoother interactions among participants in the mortgage process.

Seamless PDF editing enables users to make urgent amendments efficiently.

eSigning capabilities simplify the document approval process, minimizing delays.

Real-time collaboration tools improve communication among lenders, borrowers, and agents.

Leveraging interactive tools in the context of mortgages can lead to better document handling, reducing the risk of errors that could escalate into larger compliance issues. This is especially important given the array of forms required throughout the mortgage process. Users can effectively streamline their operations, ensuring a smoother experience for all parties involved.

Filling out the incentives form: step-by-step guide

When navigating the complexities of mortgage incentives, properly filling out the incentives form is crucial. This form serves as a key mechanism through which stakeholders can communicate their needs and intentions, thus shaping their engagement with lenders and the broader market. Below is a step-by-step guide to ensure accurate and compliant submissions, leveraging the capabilities of the pdfFiller platform.

Step 1 involves accessing the form through the pdfFiller portal, where users can find the specific template tailored to mortgage incentives. Next, in Step 2, proceed to edit the document, filling out the required fields thoroughly. Pay careful attention to detail, as omissions or inaccuracies can delay the process. Step 3 mandates the addition of eSignatures, ensuring the authenticity of the document. Finally, in Step 4, save and share the document with pertinent parties to facilitate processing.

Access the incentives form through the pdfFiller platform.

Edit and fill out all required fields meticulously.

Add eSignatures to validate the document.

Save and share the completed document with involved stakeholders.

Best practices for ensuring compliance and accuracy include double-checking all entries before submission and keeping a copy of the final document for reference. By following these steps and utilizing interactive tools effectively, users can foster smoother interactions within the mortgage landscape, thereby enhancing overall outcomes.

Collaborative strategies for mortgage stakeholders

Collaboration among mortgage stakeholders is paramount for fostering stability and innovation. Engaging teams and stakeholders in document management processes promotes transparency and accountability, which are essential to rebuilding trust in the mortgage system post-crisis. Leveraging tools like pdfFiller can enhance collaboration through efficient document sharing and collaborative capabilities.

Utilizing pdfFiller for enhanced collaboration enables teams to work in unison, thus facilitating preparedness in the event of future crises. By adopting a shared approach to document handling, stakeholders can streamline workflows and ensure that all parties are on the same page. This collaborative model allows stakeholders to anticipate potential obstacles and devise collective strategies to mitigate risks associated with the mortgage ecosystem.

Engaging teams ensures comprehensive coverage of all document needs.

Utilizing pdfFiller improves accessibility, allowing stakeholders to manage documents from anywhere.

Collective action among stakeholders mitigates risks of future crises.

Fostering a culture of collaboration within the mortgage sector can lead to innovative solutions that better serve borrowers and contribute to a more resilient market. Creating such environments empowers stakeholders to share resources and insights while collectively navigating any obstacles that may arise.

Looking forward: the future of mortgage incentives

As we look toward the future of mortgage incentives, emerging trends in incentive structures are expected to significantly reshape the landscape. Increasingly, technology is playing a transformative role in how mortgage products are developed and marketed, with data-driven insights informing personalized lending solutions tailored to meet borrower needs.

Moreover, innovative financial products that incorporate risk-sharing mechanisms may align lender interests more closely with borrower success. Potential advances in predictive analytics will also enable lenders to make more informed decisions, potentially reducing systemic risks while promoting sustained stability across the mortgage market.

Emerging technologies enable more personalized mortgage solutions that meet specific borrower needs.

Risk-sharing arrangements can align lender and borrower incentives, promoting mutual success.

Predictive analytics can enhance decision-making processes for lenders and reduce systemic vulnerabilities.

Preparing for future crises requires a proactive approach, where stakeholders embrace transparency and resilient practices. Collectively, developing robust frameworks that prioritize stability, accountability, and borrower protection will ensure the long-term sustainability of the mortgage market.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How do I edit mortgage crisis exploring incentives online?

pdfFiller allows you to edit not only the content of your files, but also the quantity and sequence of the pages. Upload your mortgage crisis exploring incentives to the editor and make adjustments in a matter of seconds. Text in PDFs may be blacked out, typed in, and erased using the editor. You may also include photos, sticky notes, and text boxes, among other things.

Can I create an eSignature for the mortgage crisis exploring incentives in Gmail?

When you use pdfFiller's add-on for Gmail, you can add or type a signature. You can also draw a signature. pdfFiller lets you eSign your mortgage crisis exploring incentives and other documents right from your email. In order to keep signed documents and your own signatures, you need to sign up for an account.

How do I edit mortgage crisis exploring incentives on an iOS device?

Yes, you can. With the pdfFiller mobile app, you can instantly edit, share, and sign mortgage crisis exploring incentives on your iOS device. Get it at the Apple Store and install it in seconds. The application is free, but you will have to create an account to purchase a subscription or activate a free trial.

What is mortgage crisis exploring incentives?

The mortgage crisis exploring incentives refers to various programs and policies designed to provide financial relief and support to individuals and homeowners affected by the mortgage crisis, which typically involves high rates of foreclosures and loan defaults.

Who is required to file mortgage crisis exploring incentives?

Homeowners, lenders, and various financial institutions may be required to file for mortgage crisis exploring incentives if they are seeking assistance or are a part of a program aimed at addressing the mortgage crisis.

How to fill out mortgage crisis exploring incentives?

To fill out mortgage crisis exploring incentives, individuals or institutions generally need to gather required documentation, follow specified guidelines outlined by regulatory bodies, and complete any necessary forms accurately before submission.

What is the purpose of mortgage crisis exploring incentives?

The purpose of mortgage crisis exploring incentives is to alleviate the financial burden on those impacted by the mortgage crisis, prevent foreclosures, stabilize housing markets, and promote economic recovery.

What information must be reported on mortgage crisis exploring incentives?

Information that must be reported typically includes personal or business details, mortgage account information, financial hardships faced, and any previous attempts at obtaining relief or assistance.

Fill out your mortgage crisis exploring incentives online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Mortgage Crisis Exploring Incentives is not the form you're looking for?Search for another form here.

Relevant keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.