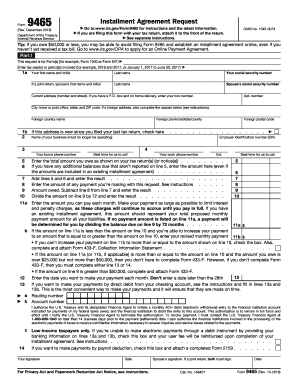

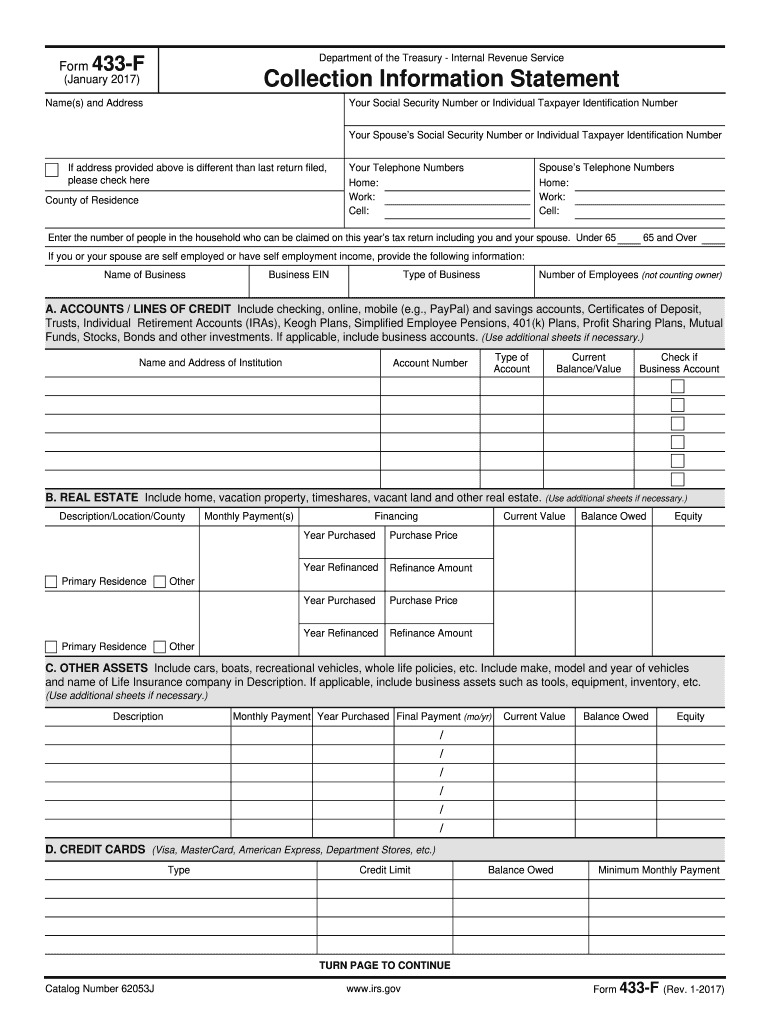

IRS 433-F 2017 free printable template

Get, Create, Make, and Sign IRS 433-F

Instructions and Help about IRS 433-F

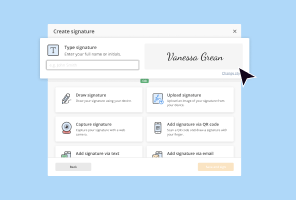

How to edit IRS 433-F

How to fill out IRS 433-F

About IRS 433-F 2017 previous version

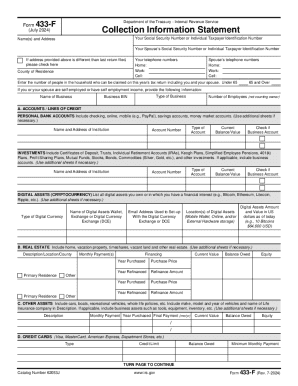

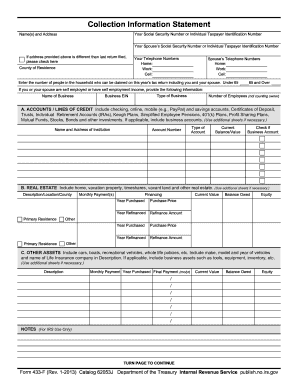

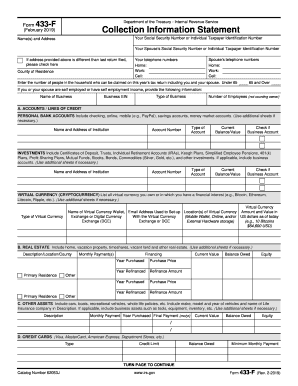

What is IRS 433-F?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

Where do I send the form?

What is the purpose of this form?

Who needs the form?

Components of the form

What information do you need when you file the form?

FAQ about IRS 433-F

What should I do if I realize I made a mistake after submitting IRS 433-F?

If you discover an error after filing IRS 433-F, the best course of action is to file an amended version of the form. Ensure that you clearly indicate any corrections made and provide appropriate supporting documentation where required to avoid any processing delays.

How can I check the status of my IRS 433-F submission after filing?

To track your IRS 433-F submission, you can log into your IRS online account. If e-filed, look for confirmation emails or messages indicating receipt. It's crucial to keep tabs on this status, especially to address issues such as common rejection codes promptly.

Are there specific requirements for electronically signing IRS 433-F?

E-signatures for IRS 433-F must meet IRS standards, which means using secure methods that ensure authenticity. Organizations and individuals need to familiarize themselves with these standards, especially if filing on behalf of someone else, to maintain compliance.

What common errors might I encounter while filing IRS 433-F, and how can I avoid them?

Some frequent mistakes when filing IRS 433-F include providing incorrect personal details or failing to include necessary attachments. Double-check all information, ensure accuracy, and consult IRS resources or a tax professional to minimize these errors.

What should I do if my IRS 433-F is rejected and I need a refund?

In cases where your IRS 433-F submission is rejected, review the rejection notice for specific reasons. After correcting errors, you may file again and, in some cases, request a refund if applicable. Always refer to IRS guidelines for the steps to take after a rejection.