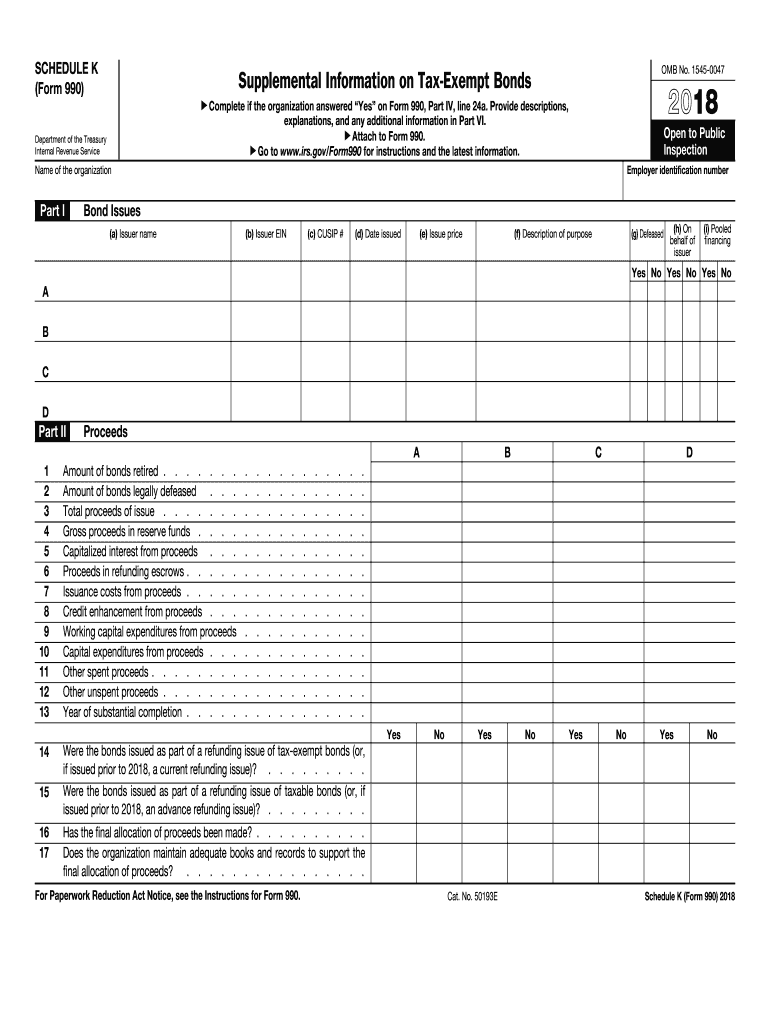

IRS 990 - Schedule K 2018 free printable template

Get, Create, Make, and Sign IRS 990 - Schedule K

Instructions and Help about IRS 990 - Schedule K

How to edit IRS 990 - Schedule K

How to fill out IRS 990 - Schedule K

About IRS 990 - Schedule K 2018 previous version

What is IRS 990 - Schedule K?

Who needs the form?

Components of the form

What payments and purchases are reported?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

What is the purpose of this form?

When am I exempt from filling out this form?

Due date

How many copies of the form should I complete?

What information do you need when you file the form?

Where do I send the form?

FAQ about IRS 990 - Schedule K

What should I do if I made a mistake on my IRS Form Schedule K?

If you've identified a mistake after filing your IRS Form Schedule K, you need to submit an amended return using the correct form. Ensure you clearly indicate that it's an amendment and provide the necessary corrected information. This will help prevent any future complications with your tax filing.

How can I track the status of my IRS Form Schedule K submission?

To track your IRS Form Schedule K submission, you can use the IRS 'Where's My Refund?' tool available on their website. Additionally, if you filed electronically and received a confirmation, keep this receipt as it may assist in tracking the processing status of your form.

Are there any common errors I should be aware of when submitting IRS Form Schedule K?

Yes, common errors include incorrect taxpayer identification numbers and mismatched amounts reported on other tax forms. Double-checking your entries and ensuring all necessary attachments are included can help minimize the chances of submission errors on your IRS Form Schedule K.

How long should I retain copies of my IRS Form Schedule K?

It's recommended to keep your records for at least three years after the date you filed your IRS Form Schedule K. This retention period is important in case of audits or discrepancies regarding your tax returns, ensuring you have supporting documentation available.