IRS 990-EZ 2019 free printable template

Get, Create, Make, and Sign IRS 990-EZ

Instructions and Help about IRS 990-EZ

How to edit IRS 990-EZ

How to fill out IRS 990-EZ

About IRS 990-EZ 2019 previous version

What is IRS 990-EZ?

Who needs the form?

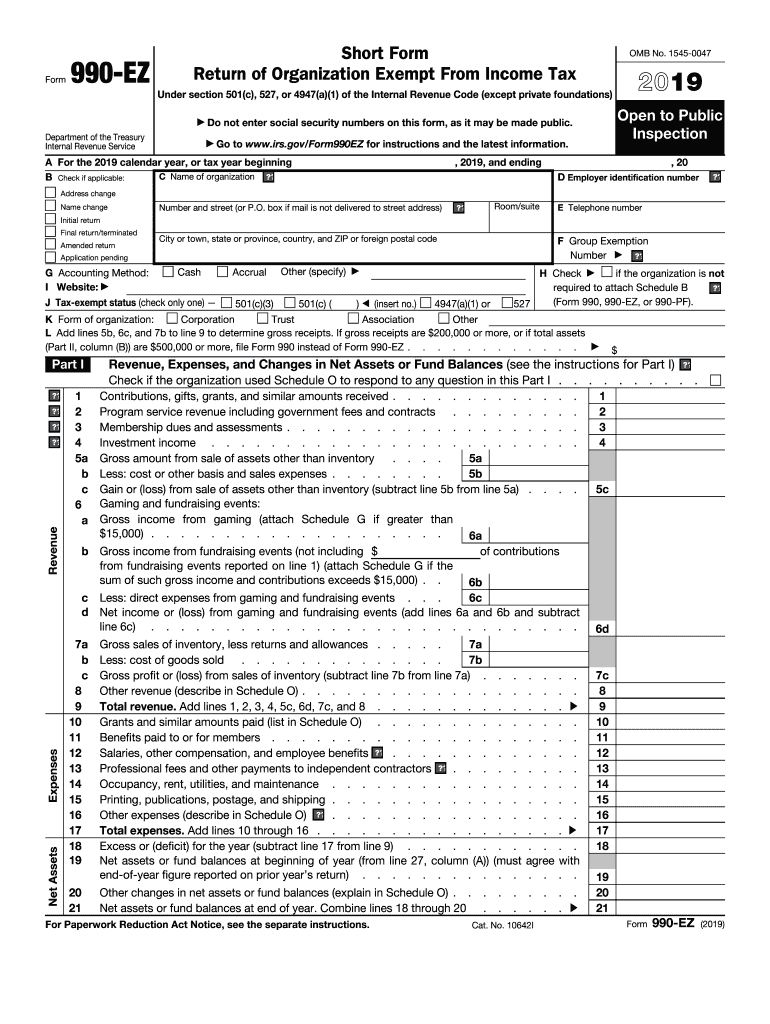

Components of the form

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

What is the purpose of this form?

When am I exempt from filling out this form?

Due date

What information do you need when you file the form?

Where do I send the form?

FAQ about IRS 990-EZ

What should I do if I notice a mistake after filing my IRS 990-EZ?

If you find an error after submitting your IRS 990-EZ, you should file an amended return using Form 990 EZ Amended Return. Clearly indicate that it’s an amendment and provide the corrected information. Send it to the same address where the original was filed.

How can I track the status of my IRS 990-EZ filing?

To track your IRS 990-EZ, you can use the IRS's online tools or call their customer service. Keep your submission details handy, as you may be asked for information related to your return. Also, note that e-filed returns may process faster than paper submissions.

Are there specific scenarios where I can authorize someone else to file my IRS 990-EZ?

You can authorize someone, such as a tax professional or trusted individual, to file your IRS 990-EZ using Form 2848, Power of Attorney. Ensure that they have the appropriate permissions and understand your organization's financial details.

What common errors should I avoid when filing the IRS 990-EZ?

Common errors include incorrect or missing financial data, failing to meet signature requirements, and not checking for math errors. Double-check your figures and ensure all parts of the form are complete to avoid any issues with processing.