Enter overpayment applied as credit from 2017 Form 1042. Credit for amounts withheld by other withholding agents Total payments. Phone no. Cat. No. 11384V Form 1042 2018 Page 2 a b c d e 70a Total tax reported as withheld or paid by withholding agent on all Forms 1042-S and 1000 Tax withheld by withholding agent. Add lines 65 through 67. If line 64e is larger than line 68 enter balance due here. Apply overpayment sum of lines 70a and 70b to check one Credit on 2019 Form 1042 or Refund 63a 63b 1...63b 2 63c 1 63c 2 63d 63e 64a 64b 64c 64d 64e 65a 65b 67a 67b 70b be 2a 2b 2c 2d Reconciliation of Payments of U.S. Source FDAP Income withheld upon under chapter 4 because Amount of income paid to recipients whose chapter 4 status established no withholding is required Amount of excluded nonfinancial payments. OMB No. 1545-0096 CC RD CAF CR EDC Enter date final income paid FD FF FP I SIC Record of Federal Tax Liability Do not show federal tax deposits here Tax liability for period including any...taxes assumed Line on Form s 1000 Jan. May Sept. Jan. total 25 May total 45 Sept. total Feb. June Oct. Feb. total 30 June total 50 Oct. total Mar. July 55 Nov. total 35 July total Mar. total Apr. Aug. Dec. 60 Dec. total 40 Aug. total Apr. total No. of Forms 1042-S filed a On paper b Electronically Total gross amounts reported on all Forms 1042-S and 1000 a Total U.S. source FDAP income other than U.S. source substitute payments reported. Annual Withholding Tax Return for U*S* Source Income of...Foreign Persons Form Department of the Treasury Internal Revenue Service. Ch* 4 Status Code Number street and room or suite no. if a P. O. box see instructions City or town state or province country and ZIP or foreign postal code If you do not expect to file this return in the future check here Line No* Period ending For IRS Use Only Employer identification number Name of withholding agent Section 1 Go to www*irs*gov/Form1042 for instructions and the latest information* If this is an amended...return check here. OMB No* 1545-0096 CC RD CAF CR EDC Enter date final income paid FD FF FP I SIC Record of Federal Tax Liability Do not show federal tax deposits here Tax liability for period including any taxes assumed Line on Form s 1000 Jan* May Sept. Jan* total 25 May total 45 Sept. total Feb. June Oct. Feb. total 30 June total 50 Oct. total Mar* July 55 Nov* total 35 July total Mar* total Apr* Aug. Dec* 60 Dec* total 40 Aug. total Apr* total No* of Forms 1042-S filed a On paper b...Electronically Total gross amounts reported on all Forms 1042-S and 1000 a Total U*S* source FDAP income other than U*S* source substitute payments reported. 62a 62c d Enter gross amounts actually paid if different from gross amounts reported. 62d Do you want to allow another person to discuss this return with the IRS see instructions Yes. Complete the following. Third Party Designee Phone Personal identification No name Paid Preparer Use Only Sign Here no. number PIN Under penalties of perjury...I declare that I have examined this return including accompanying schedules and statements and to the best of my knowledge and belief it is true correct and complete.

pdfFiller is not affiliated with IRS

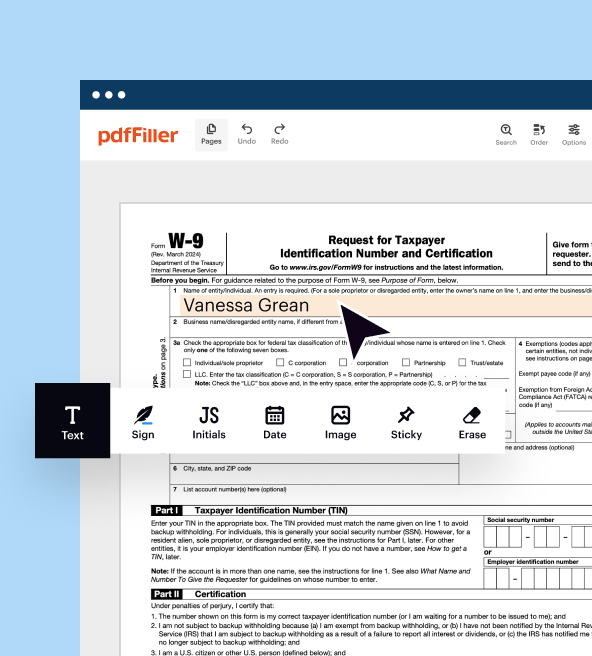

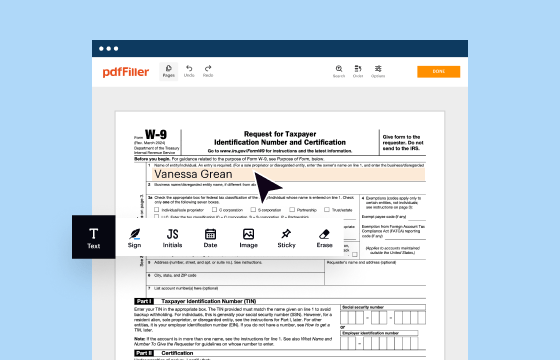

Get, Create, Make, and Sign form 1042

Edit your form 1042 online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

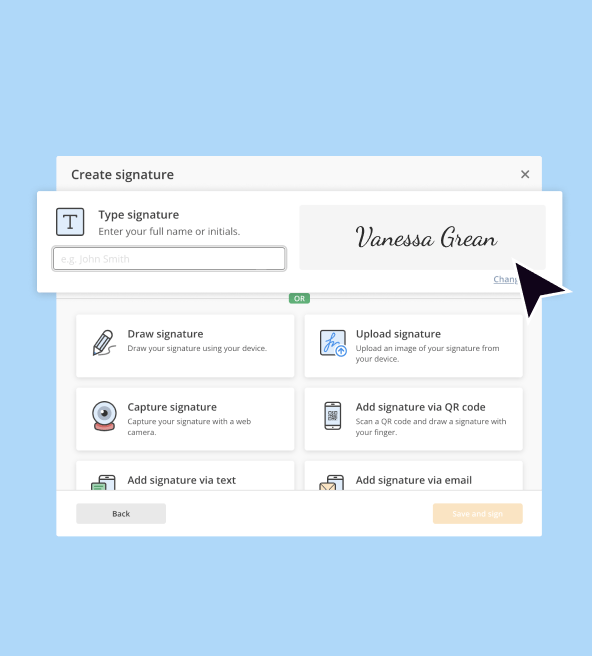

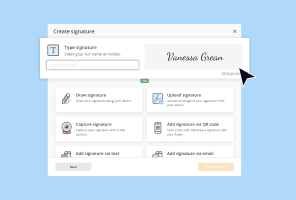

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

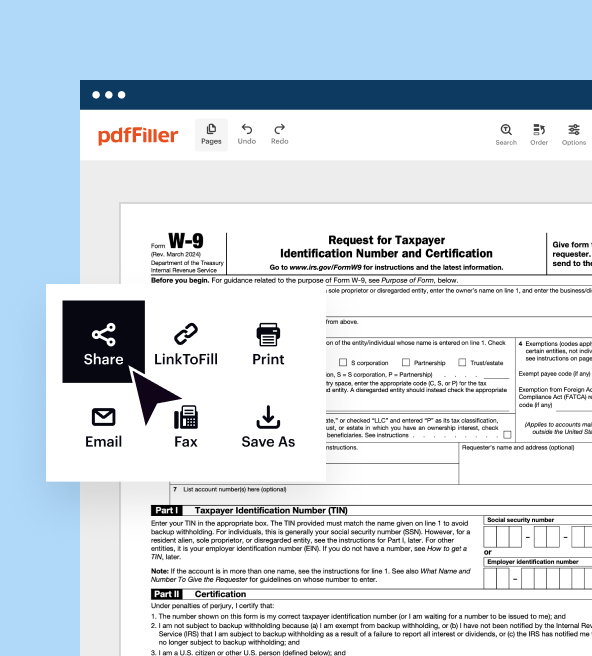

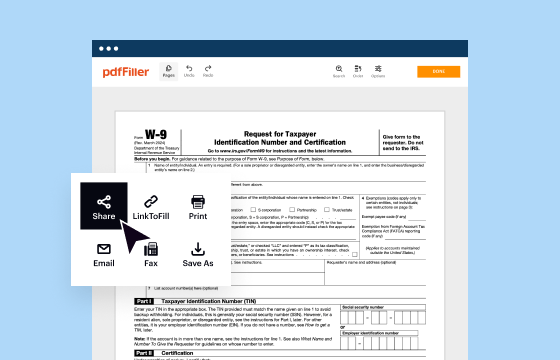

Share your form instantly

Email, fax, or share your form 1042 via URL. You can also download, print, or export forms to your preferred cloud storage service.

Instructions and Help about IRS 1042

How to edit IRS 1042

How to fill out IRS 1042

Instructions and Help about IRS 1042

How to edit IRS 1042

To edit IRS 1042, you can use various online tools that facilitate form modification and ensure compliance with IRS requirements. It is essential to make your edits carefully, maintaining accurate entries to reflect your financial situation. Ensure that any new information aligns with the latest IRS guidelines prior to re-submission.

How to fill out IRS 1042

To fill out IRS 1042 accurately, follow these structured steps:

01

Begin by downloading the form from the IRS website or accessing it through your tax software.

02

Identify the taxpayer (withholding agent) and payee information, ensuring that all names and addresses are correctly entered.

03

Document the income subject to withholding in the appropriate sections, as errors can lead to penalties.

04

Double-check that all required signatures are present to validate the form.

About IRS previous version

What is IRS 1042?

What is the purpose of this form?

Who needs the form?

When am I exempt from filling out this form?

Components of the form

What are the penalties for not issuing the form?

What information do you need when you file the form?

Is the form accompanied by other forms?

Where do I send the form?

About IRS previous version

What is IRS 1042?

IRS 1042 is the tax form used for reporting income paid to foreign persons, including non-resident aliens and foreign entities. This form is crucial for withholding agents who must report and remit the correct tax amounts. Understanding this form is vital for compliance with U.S. tax laws regarding payments made to non-residents.

What is the purpose of this form?

The primary purpose of IRS 1042 is to report income subject to U.S. withholding tax and the corresponding tax withheld on payments to foreigners. This includes various types of U.S.-source income, ensuring that tax obligations are met by non-resident recipients in accordance with U.S. tax legislation.

Who needs the form?

Individuals and entities that make payments to foreign persons must use IRS 1042. This includes financial institutions, corporations, and individuals making payments such as interest, dividends, rents, or royalties. Understanding your obligation to file this form is essential for compliance and to avoid penalties.

When am I exempt from filling out this form?

Exemptions from filing IRS 1042 generally apply to certain types of payments and specific foreign recipients. For instance, payments made to foreign governments, international organizations, or certain non-profits may be exempt. It's important to consult IRS guidelines or a tax professional to clarify your specific situation.

Components of the form

IRS 1042 consists of several key components, including the identification of the withholding agent, information about the payments made, tax withheld, and certifications of non-residency. Each section must be completed thoroughly to ensure accurate reporting and compliance.

What are the penalties for not issuing the form?

Failing to issue IRS 1042 when required can result in significant penalties, including fines and interest on unpaid taxes. The IRS may impose penalties based on the amount of tax required to be reported and if the failure is deemed intentional, penalties can increase dramatically. Therefore, timely and accurate filing is critical.

What information do you need when you file the form?

When filing IRS 1042, the necessary information includes the withholding agent's details, the payment recipient's identifying information, the type of payments made, and the corresponding amounts withheld. Accurate record-keeping prior to filing will simplify the process and ensure compliance.

Is the form accompanied by other forms?

IRS 1042 may be accompanied by several other forms, depending on the specific circumstances of the payments and the tax treaty benefits claimed. Commonly used forms may include IRS 1042-S, which reports the income paid and tax withheld, so ensure thorough preparation and inclusion as necessary.

Where do I send the form?

IRS 1042 should be submitted to the address specified in the form's instructions. This may vary based on the type of filing and the location of the withholding agent. It's essential to verify the submission address to avoid any delays in processing.

Use this catalog to find any type of IRS forms. We've gathered all of them under this section uncategorized to help you to find a proper form faster. Once you spot it on this list, have a look at the versions and schedules you might need as attachments. All returns are available for 2016 and for previous fiscal years.