IRS 982 2011 free printable template

Get, Create, Make, and Sign IRS 982

Instructions and Help about IRS 982

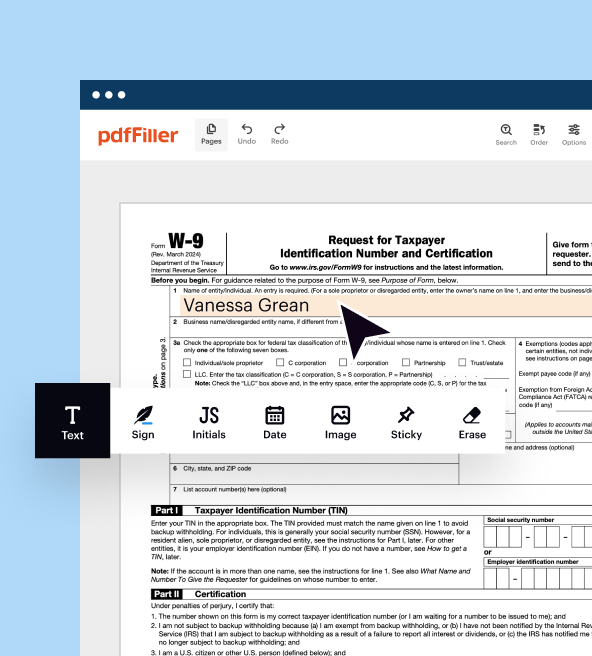

How to edit IRS 982

How to fill out IRS 982

About IRS previous version

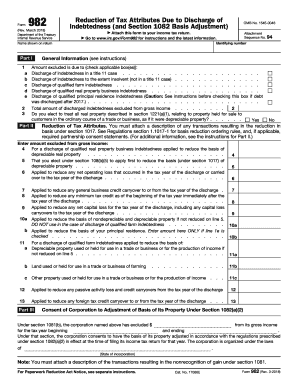

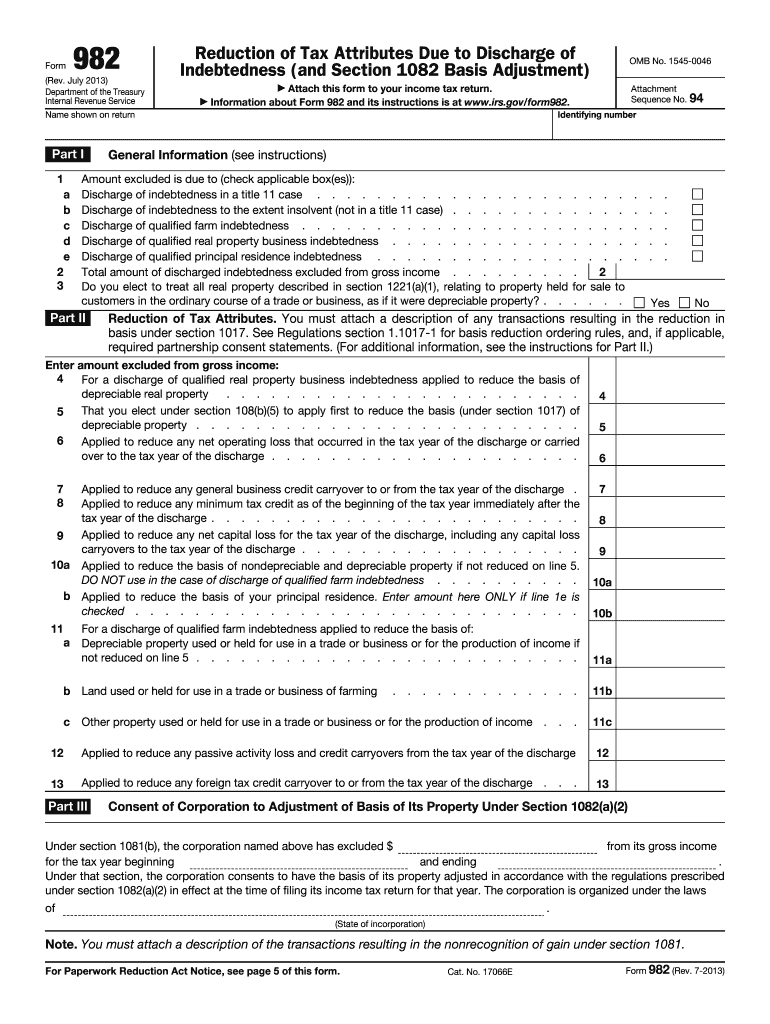

What is IRS 982?

Who needs the form?

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about IRS 982

What should I do if I realize I've made a mistake after submitting my 2011 982 form?

If you discover an error after filing your 2011 982 form, you should submit an amended or corrected version as soon as possible. Ensure you identify the specific changes needed and clearly indicate that it's a correction. Keeping detailed records of all submissions is essential for accurate tracking.

How can I verify that my 2011 982 form has been received and processed?

To verify receipt and processing of your 2011 982 form, you may contact the relevant submission authority or utilize online tracking tools provided by the service. Additionally, ensure you retain confirmation emails or receipts as proof of submission for your records.

What are some common errors filers make with the 2011 982 form, and how can I avoid them?

Common errors include incorrect taxpayer identification numbers and mismatched name entries. To avoid these mistakes, double-check all personal information and ensure consistency with prior submissions. Consulting guides or using filing software may also help minimize errors.

Are e-signatures acceptable when filing the 2011 982 form electronically?

Yes, e-signatures are generally accepted for electronically filed 2011 982 forms, provided they comply with the relevant legal standards. Ensure that your e-signature process meets any technical requirements specified by the filing authority to avoid rejection.

What steps should I take if I receive a notice regarding my 2011 982 form submission?

If you receive a notice related to your 2011 982 form submission, carefully read the details provided. Prepare any necessary documentation to respond and contact the issuing authority directly for clarification on any required actions to resolve the issue effectively.