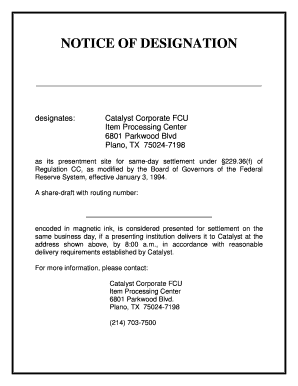

Annual Regulation E Notice

What is Annual regulation e notice?

The Annual Regulation E notice is a document that informs consumers of their rights under the Electronic Fund Transfer Act. This notice outlines the rules and regulations regarding electronic fund transfers, such as ATM transactions, direct deposits, and debit card purchases.

What are the types of Annual regulation e notice?

There are two main types of Annual Regulation E notice: the initial notice and the updated notice. The initial notice is provided to consumers when they first open an account that allows electronic fund transfers. The updated notice is sent out annually to remind consumers of their rights and responsibilities under the Electronic Fund Transfer Act.

How to complete Annual regulation e notice

Completing the Annual Regulation E notice is a simple process that can be done online or in person. Follow these steps to complete the notice:

pdfFiller empowers users to create, edit, and share documents online. Offering unlimited fillable templates and powerful editing tools, pdfFiller is the only PDF editor users need to get their documents done.