IRS 1065 - Schedule D-1 2010 free printable template

Show details

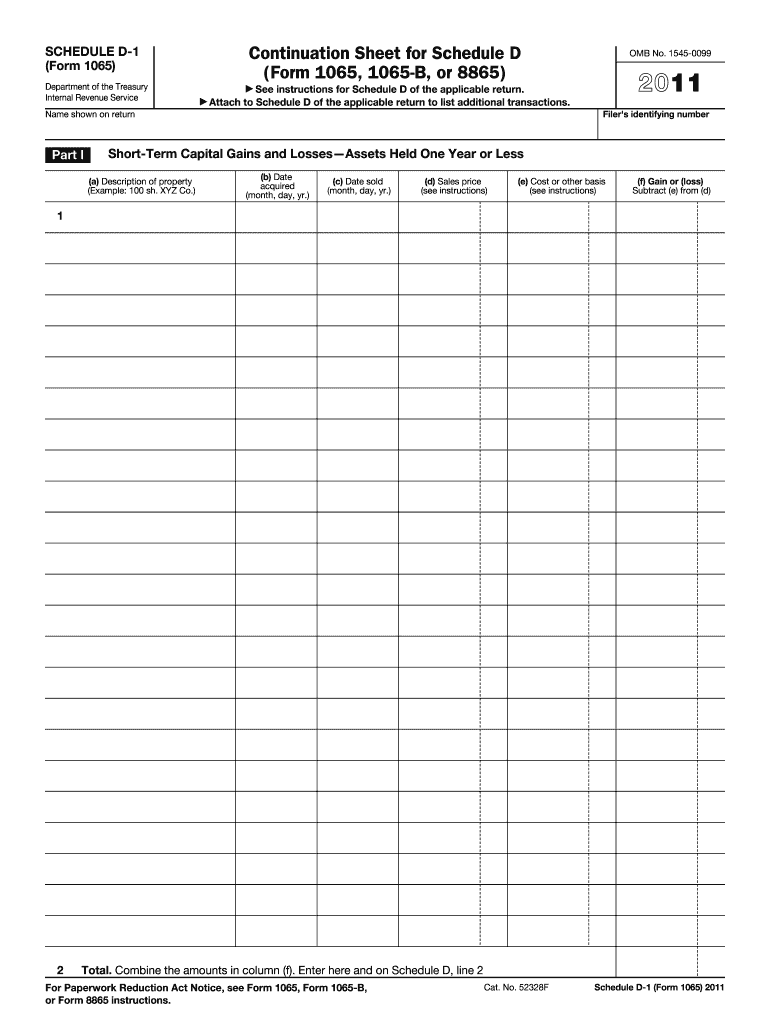

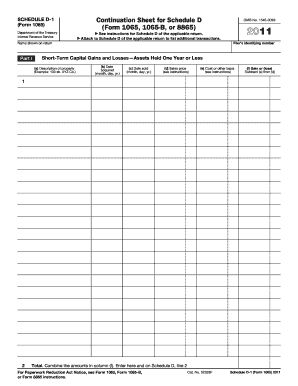

SCHEDULE D-1 (Form 1065)

Department of the Treasury Internal Revenue Service Name shown on return

Attach

See instructions for Schedule D of the applicable return. to Schedule D of the applicable

pdfFiller is not affiliated with IRS

Get, Create, Make and Sign IRS 1065 - Schedule D-1

Edit your IRS 1065 - Schedule D-1 form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your IRS 1065 - Schedule D-1 form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit IRS 1065 - Schedule D-1 online

To use the services of a skilled PDF editor, follow these steps below:

1

Log in. Click Start Free Trial and create a profile if necessary.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit IRS 1065 - Schedule D-1. Text may be added and replaced, new objects can be included, pages can be rearranged, watermarks and page numbers can be added, and so on. When you're done editing, click Done and then go to the Documents tab to combine, divide, lock, or unlock the file.

4

Get your file. Select your file from the documents list and pick your export method. You may save it as a PDF, email it, or upload it to the cloud.

The use of pdfFiller makes dealing with documents straightforward. Try it right now!

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

IRS 1065 - Schedule D-1 Form Versions

Version

Form Popularity

Fillable & printabley

How to fill out IRS 1065 - Schedule D-1

How to fill out IRS 1065 - Schedule D-1

01

Obtain Form 1065 and Schedule D-1 from the IRS website.

02

Complete the basic information on Form 1065, including partnership name, address, and EIN.

03

Determine the type of gain or loss to report on Schedule D-1.

04

Gather your partnership's data on capital gains and losses from sales of assets.

05

Fill out Part I of Schedule D-1 with details of capital assets sold, including descriptions, dates acquired, dates sold, and sale amounts.

06

Calculate the capital gain or loss for each transaction and enter the totals in Part II.

07

Complete any additional sections if your partnership has special circumstances or unique transactions.

08

Review the completed form to ensure accuracy and completeness.

09

Submit Form 1065 and Schedule D-1 by the due date, either electronically or by mail.

Who needs IRS 1065 - Schedule D-1?

01

Partnerships that have capital gains or losses from the sale of capital assets.

02

Partners in a partnership who need to report their share of these gains or losses.

03

Any entity classified as a partnership for tax purposes that is required to file Form 1065.

Instructions and Help about IRS 1065 - Schedule D-1

After reporting small business or self-employment income on Schedule C report any capital gains or losses on Schedule D a lot of people won't have any capital gains transactions but if you sell securities or other capital assets held outside a retirement account you'll have to fill out Schedule D and don't worry the IRS has devised a system to help remind you of the need to report capital gains transactions if you sell any securities your broker or mutual fund should send you a 1099 B which lists the proceeds of the sale since the 1099 B lists the proceeds of the sale you'll have to include at least the gross proceeds on Schedule D however the 1099 B currently doesn't show the actual gain or loss you realized for that you're largely on your own when it comes to capital gains calculations your so-called basis in the property is important in its simplest sense your basis is the cost of the property, but your basis can be adjusted up or down depending on circumstances let's say you invested one thousand dollars in a mutual fund whose shares were selling for $10 your one thousand dollar investment gives you 100 shares further assume that you made this investment in early January the fund moved up over the year and on December 15th of the same year the fund distributed to you $60 in dividends you reinvested these dividends in five shares of the fund when the fund was $12 a share a few days later on December 20th you sold all your holdings in the fund because you thought the market would go down assume your selling price was $12 a share so your sale of 105 shares at $12 a share yielded 1260 dollars your mutual fund then sends you a 1099 B which shows 1260 dollars in gross proceeds so what's your total gain on the sale you invested $1,000 back in January, so your reportable gain is 260 dollars right wrong your reportable gain is actually only $200 not two hundred and sixty dollars that's because the $60 in reinvested dividends are added to the basis of your holdings like any additional purchase, so your cost basis in the mutual fund is the original $1000 investment plus the $60 in reinvested dividends or one thousand and sixty dollars when you subtract this from your gross proceeds of one thousand two hundred and sixty dollars you get a net gain of two hundred dollars and in case you're wondering you do have to pay taxes on the $60 in distributed dividends that you received the $60 in dividends are reported on a 1099 — div and our taxed on Schedule B so if you reinvest your mutual fund dividends but don't adjust your cost basis up you'll wind up paying taxes twice on that dividend you'll pay ordinary income taxes once when the dividend is distributed and capital gains taxes once when you sell if you don't adjust your cost basis up unfortunately calculating your capital gains can get difficult the example I gave was simple but imagine if your mutual fund makes monthly distributions, and you buy and sell chunks of the fund during the year determining...

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I edit IRS 1065 - Schedule D-1 from Google Drive?

You can quickly improve your document management and form preparation by integrating pdfFiller with Google Docs so that you can create, edit and sign documents directly from your Google Drive. The add-on enables you to transform your IRS 1065 - Schedule D-1 into a dynamic fillable form that you can manage and eSign from any internet-connected device.

Can I create an electronic signature for signing my IRS 1065 - Schedule D-1 in Gmail?

Upload, type, or draw a signature in Gmail with the help of pdfFiller’s add-on. pdfFiller enables you to eSign your IRS 1065 - Schedule D-1 and other documents right in your inbox. Register your account in order to save signed documents and your personal signatures.

Can I edit IRS 1065 - Schedule D-1 on an Android device?

You can edit, sign, and distribute IRS 1065 - Schedule D-1 on your mobile device from anywhere using the pdfFiller mobile app for Android; all you need is an internet connection. Download the app and begin streamlining your document workflow from anywhere.

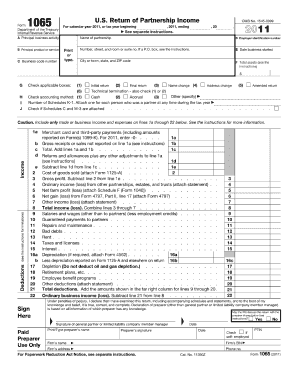

What is IRS 1065 - Schedule D-1?

IRS 1065 - Schedule D-1 is a supplementary form used by partnerships to report income, gain, loss, deductions, and credits from activities in which the partnership is involved.

Who is required to file IRS 1065 - Schedule D-1?

Partnerships that have capital gains or losses, or other income and deductions that must be reported on the schedule, are required to file IRS 1065 - Schedule D-1.

How to fill out IRS 1065 - Schedule D-1?

To fill out IRS 1065 - Schedule D-1, partnerships must provide details about their capital gains and losses by reporting the transactions and relevant financial information in the specified sections of the form.

What is the purpose of IRS 1065 - Schedule D-1?

The purpose of IRS 1065 - Schedule D-1 is to properly report the partnership's capital gains and losses to the Internal Revenue Service, ensuring compliance with tax regulations.

What information must be reported on IRS 1065 - Schedule D-1?

IRS 1065 - Schedule D-1 requires reporting information such as details of capital asset transactions, specific gains and losses, and relevant deductions associated with the partnership's activities.

Fill out your IRS 1065 - Schedule D-1 online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

IRS 1065 - Schedule D-1 is not the form you're looking for?Search for another form here.

Relevant keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.