Get the free DR 0253 (08/30/13) Income tax closing agreement

Get Form

Show details

*130253 19999* DR 0253 (08/30/13) Colorado department of revenue Denver, CO 80261-0005 www.TaxColorado.com Income Tax Closing Agreement I. Taxpayer for which/whom agreement is sought Last Name First

We are not affiliated with any brand or entity on this form

Get, Create, Make, and Sign dr 0253 083013 income

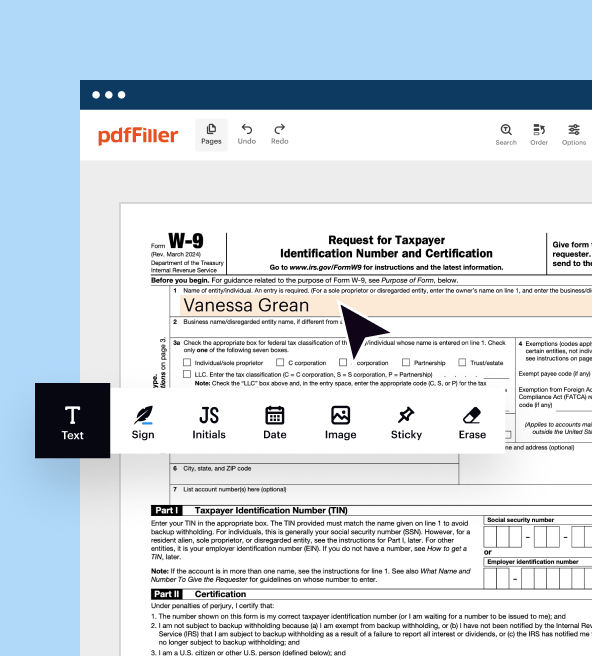

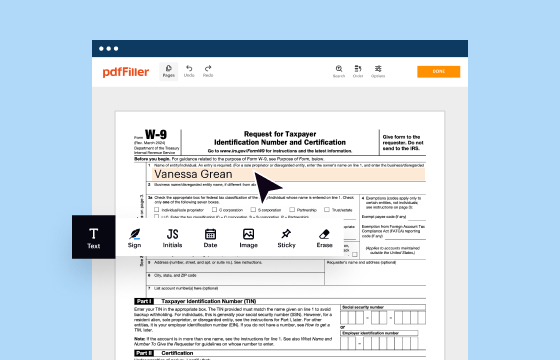

Edit your dr 0253 083013 income online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

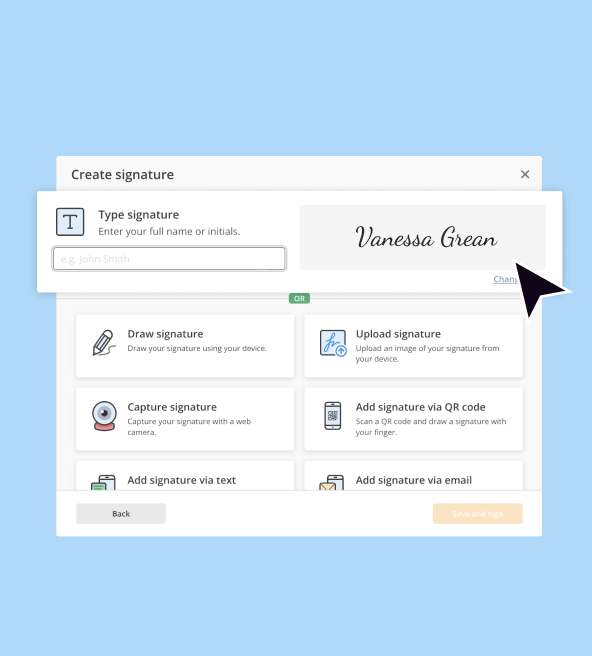

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

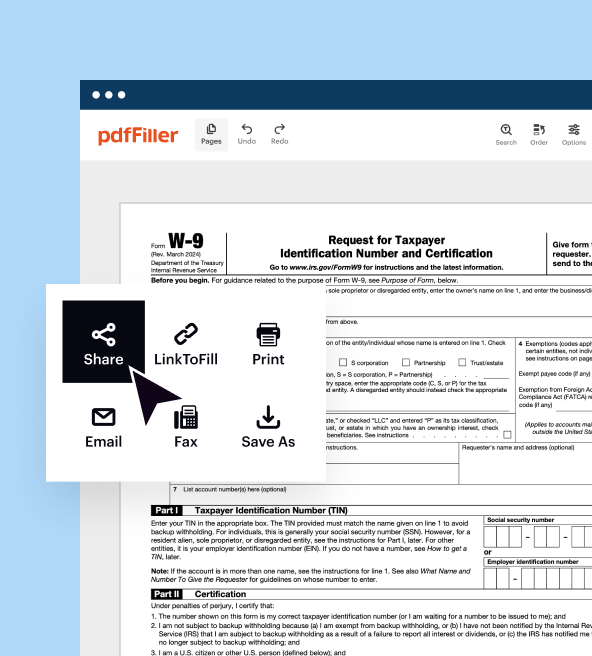

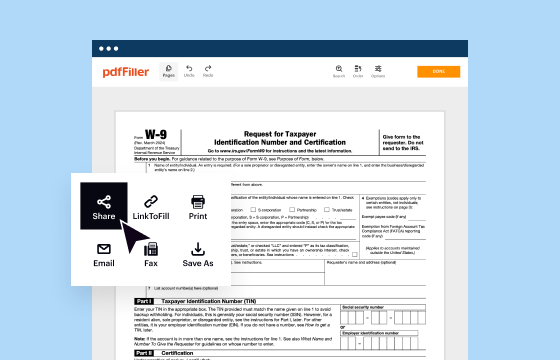

Share your form instantly

Email, fax, or share your dr 0253 083013 income via URL. You can also download, print, or export forms to your preferred cloud storage service.

Instructions and Help about dr 013 income

How to edit dr 013 income

How to fill out dr 013 income

Instructions and Help about dr 013 income

How to edit dr 013 income

To edit the dr 013 income tax form, you can use pdfFiller's tools designed for form editing. Begin by uploading your completed form to the platform. Once uploaded, you can make necessary changes by selecting the fields you want to edit. Save your changes and ensure all information is accurate before submission.

How to fill out dr 013 income

Filling out the dr 013 income tax form involves several key steps:

01

Gather necessary documentation such as income statements and tax IDs.

02

Complete the form by entering your personal information accurately.

03

Double-check all entries for accuracy.

To ensure a smooth submission process, follow these steps closely, and consider using pdfFiller for ease of use and to avoid mistakes.

Latest updates to dr 013 income

Latest updates to dr 013 income

Stay updated on any revisions to the dr 013 income tax form by checking the IRS website regularly. Updates may include changes in filing deadlines, modifications to reporting requirements, or alterations in penalties for non-compliance.

All You Need to Know About dr 013 income

What is dr 013 income?

What is the purpose of this form?

Who needs the form?

When am I exempt from filling out this form?

Components of the form

What are the penalties for not issuing the form?

What information do you need when you file the form?

Is the form accompanied by other forms?

Where do I send the form?

All You Need to Know About dr 013 income

What is dr 013 income?

The dr 013 income form is a specific tax document required by the IRS for reporting certain income types. It is essential for accurate tax compliance and helps the IRS track income sources for tax assessment purposes.

What is the purpose of this form?

The primary purpose of the dr 013 income form is to collect information on various income types received during the tax year. This form ensures that taxpayers report all income sources, thereby facilitating accurate tax assessments and compliance with federal tax laws.

Who needs the form?

Taxpayers who have received certain types of income, such as self-employment income, rental income, or other reported payments, are typically required to file the dr 013 income form. It is important for independent contractors and freelancers to understand their obligations for accurate reporting.

When am I exempt from filling out this form?

You may be exempt from filling out the dr 013 income form if your total income falls below the threshold for filing taxes, or if you did not earn the types of income that need to be reported on this form. Additionally, specific tax exemptions may apply based on your situation.

Components of the form

The dr 013 income form typically comprises sections for personal identification, income details, and applicable deductions. Each section must be completed thoroughly to ensure the accuracy of your tax return. Understanding these components is necessary for effective form completion.

What are the penalties for not issuing the form?

Failing to issue the dr 013 income form can lead to significant penalties from the IRS. These penalties may include fines for incorrect or late filings, which can increase based on the duration of the delay or the severity of the inaccuracies. It is crucial to comply with all requirements associated with the form.

What information do you need when you file the form?

When filing the dr 013 income form, you will need to provide several key pieces of information, including your Social Security number or Employer Identification Number (EIN), total income amount, and any applicable deductions. Make sure to have all relevant documentation organized for a smooth filing process.

Is the form accompanied by other forms?

The dr 013 income form may need to be submitted alongside other forms depending on your specific tax circumstances. For instance, you may need to include supporting documentation or other IRS forms that relate to the income type you reported.

Where do I send the form?

The completed dr 013 income form should be sent to the address specified by the IRS based on your state of residence and the type of income reported. It is critical to verify the correct address on the IRS website to ensure prompt processing of your submission.

Use this catalog to find any type of IRS forms. We've gathered all of them under this section uncategorized to help you to find a proper form faster. Once you spot it on this list, have a look at the versions and schedules you might need as attachments. All returns are available for 2016 and for previous fiscal years.