IRS 8840 2017 free printable template

Get, Create, Make, and Sign IRS 8840

Instructions and Help about IRS 8840

How to edit IRS 8840

How to fill out IRS 8840

About IRS 8 previous version

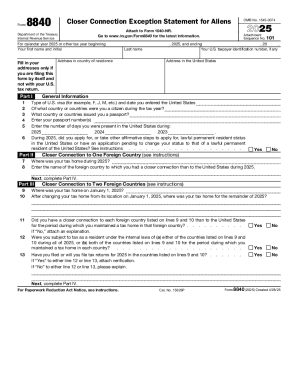

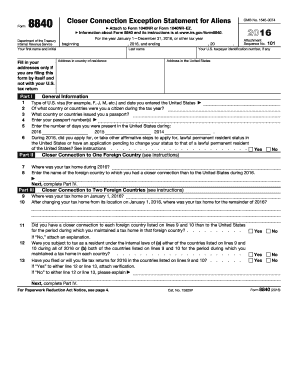

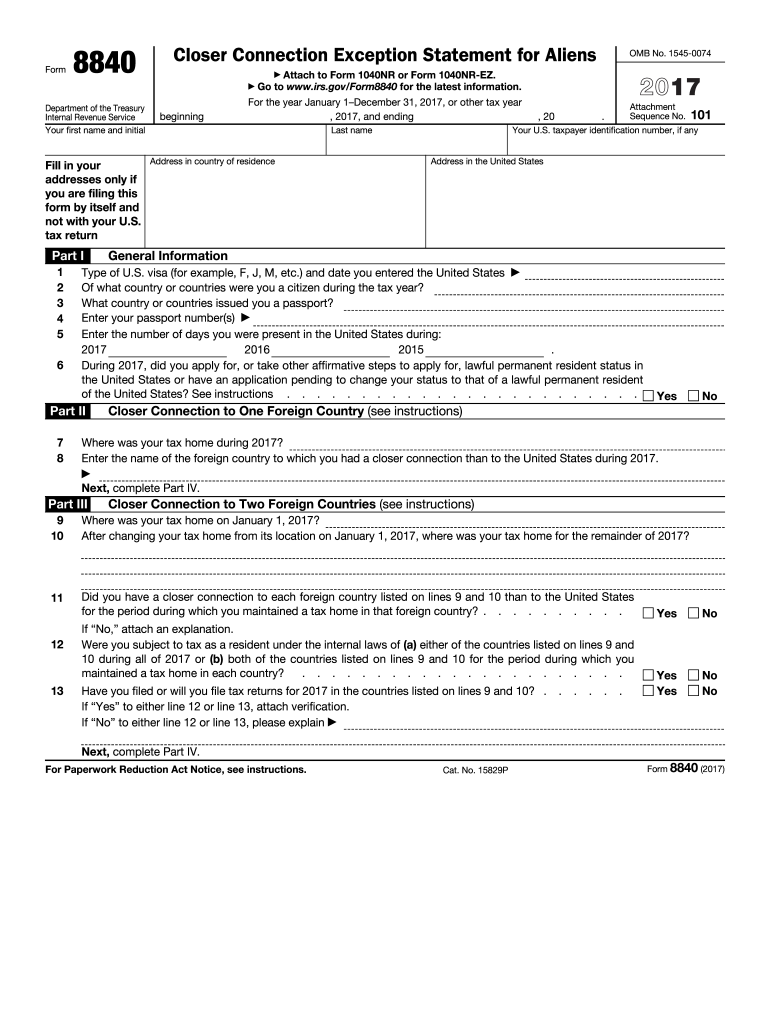

What is IRS 8840?

Who needs the form?

Components of the form

What information do you need when you file the form?

Where do I send the form?

What is the purpose of this form?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

FAQ about IRS 8840

How can I submit an amended 8840 2017 form if I discover an error?

If you need to submit an amended 8840 2017 form, first ensure that you have the corrected information. You can file the amended form along with any necessary explanations regarding the changes made. It's crucial to annotate the amended form clearly to specify it as such to avoid any confusion by the IRS.

What should I do if my e-filed 8840 2017 form gets rejected?

If your e-filed 8840 2017 form is rejected, you will receive a notification detailing the rejection reason. Resolve the identified issues, correct the errors, and resubmit the form promptly. Keeping track of rejection codes can help you prevent similar issues in the future.

What are the security measures in place for submitting the 8840 2017 form electronically?

When submitting the 8840 2017 form electronically, your personal data is safeguarded through encryption protocols to ensure security and privacy. It is recommended to utilize reputable e-file services that comply with IRS standards for protecting sensitive information during transmission.

Can someone file the 8840 2017 form on behalf of another individual?

Yes, an authorized representative can file the 8840 2017 form on behalf of another individual. Proper documentation, such as a Power of Attorney (POA), must be in place to ensure that the representative is legally permitted to act on the individual's behalf in dealings with the IRS.

How long should I retain records of my submitted 8840 2017 form?

It is advisable to retain records of your submitted 8840 2017 form for at least three years after submission. This time frame is recommended in case of an audit or if the IRS requests additional information regarding your filing.