Annual Projected Profit Loss free printable template

Show details

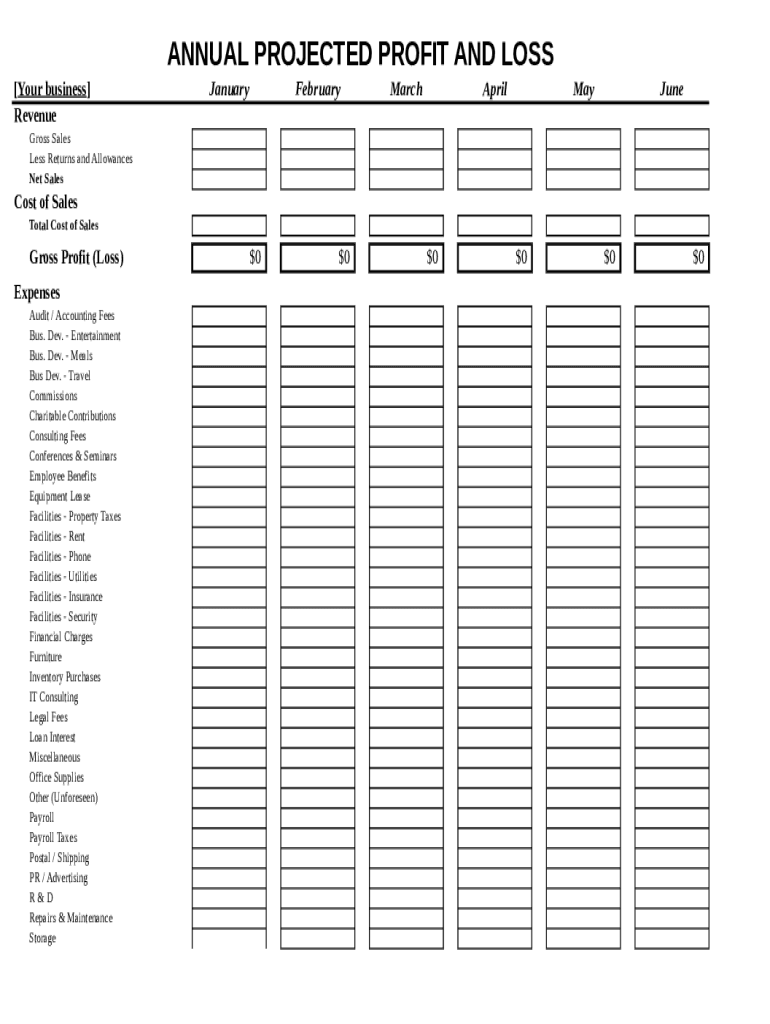

ANNUAL PROJECTED PROFIT AND LOSS Your business RevenueJanuaryFebruaryMarchAprilMayJuneGross Sales Less Returns and Allowances Net Salesroom of Sales Total Cost of Sales Gross Profit (Loss) Expenses

We are not affiliated with any brand or entity on this form

Get, Create, Make and Sign Annual Projected Profit Loss

Edit your Annual Projected Profit Loss form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your Annual Projected Profit Loss form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit Annual Projected Profit Loss online

To use the services of a skilled PDF editor, follow these steps:

1

Log in. Click Start Free Trial and create a profile if necessary.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit Annual Projected Profit Loss. Rearrange and rotate pages, add new and changed texts, add new objects, and use other useful tools. When you're done, click Done. You can use the Documents tab to merge, split, lock, or unlock your files.

4

Get your file. Select your file from the documents list and pick your export method. You may save it as a PDF, email it, or upload it to the cloud.

Uncompromising security for your PDF editing and eSignature needs

Your private information is safe with pdfFiller. We employ end-to-end encryption, secure cloud storage, and advanced access control to protect your documents and maintain regulatory compliance.

How to fill out Annual Projected Profit Loss

How to fill out Annual Projected Profit & Loss

01

Start with the header: clearly state the year for which you're projecting the profit and loss.

02

List all expected revenue sources: include every potential income stream.

03

Estimate total revenue: calculate the total projected revenue from all sources.

04

Identify fixed costs: list all regular, unchanging expenses such as rent and salaries.

05

Identify variable costs: detail expenses that fluctuate based on business activity, such as materials and utilities.

06

Calculate total costs: sum fixed and variable costs to find total projected expenses.

07

Determine gross profit: subtract total costs from total revenue.

08

Include any other income: add any additional income that is not from primary operations.

09

Calculate net profit: add gross profit and other income, then subtract taxes and interest.

Who needs Annual Projected Profit & Loss?

01

Business owners: to understand their financial forecast and make informed decisions.

02

Investors: to evaluate the potential profitability of investing in the business.

03

Lenders: to assess the financial health of the business for loan applications.

04

Financial analysts: to analyze and provide insights on the business's performance.

05

Management teams: for strategic planning and budgeting purposes.

Fill

form

: Try Risk Free

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

How can I send Annual Projected Profit Loss for eSignature?

Once your Annual Projected Profit Loss is ready, you can securely share it with recipients and collect eSignatures in a few clicks with pdfFiller. You can send a PDF by email, text message, fax, USPS mail, or notarize it online - right from your account. Create an account now and try it yourself.

How can I get Annual Projected Profit Loss?

The premium subscription for pdfFiller provides you with access to an extensive library of fillable forms (over 25M fillable templates) that you can download, fill out, print, and sign. You won’t have any trouble finding state-specific Annual Projected Profit Loss and other forms in the library. Find the template you need and customize it using advanced editing functionalities.

How do I fill out Annual Projected Profit Loss on an Android device?

On an Android device, use the pdfFiller mobile app to finish your Annual Projected Profit Loss. The program allows you to execute all necessary document management operations, such as adding, editing, and removing text, signing, annotating, and more. You only need a smartphone and an internet connection.

What is Annual Projected Profit & Loss?

Annual Projected Profit & Loss is a financial statement that estimates an organization's expected revenue, expenses, and net profit for the upcoming year, providing a forecast of financial performance.

Who is required to file Annual Projected Profit & Loss?

Typically, businesses, especially those seeking loans or investments, are required to file Annual Projected Profit & Loss. Additionally, certain regulatory agencies may mandate it for compliance purposes.

How to fill out Annual Projected Profit & Loss?

To fill out an Annual Projected Profit & Loss, start with estimated revenue figures, then list all anticipated expenses (fixed and variable). After calculating total revenue and total expenses, determine the projected net profit by subtracting expenses from revenue.

What is the purpose of Annual Projected Profit & Loss?

The purpose of the Annual Projected Profit & Loss is to provide a blueprint for financial planning, to help monitor business performance, and to serve as a tool for securing funding and making strategic decisions.

What information must be reported on Annual Projected Profit & Loss?

The information that must be reported includes projected revenue, breakdown of operational expenses, cost of goods sold, gross profit, operating expenses, taxes, and net profit.

Fill out your Annual Projected Profit Loss online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Annual Projected Profit Loss is not the form you're looking for?Search for another form here.

Relevant keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.