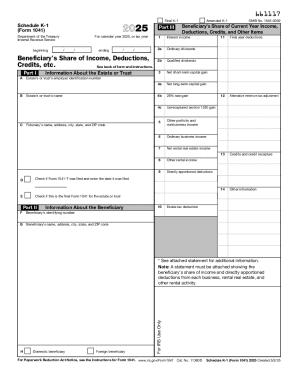

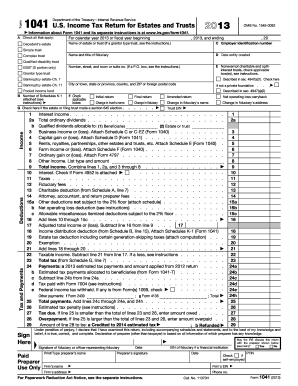

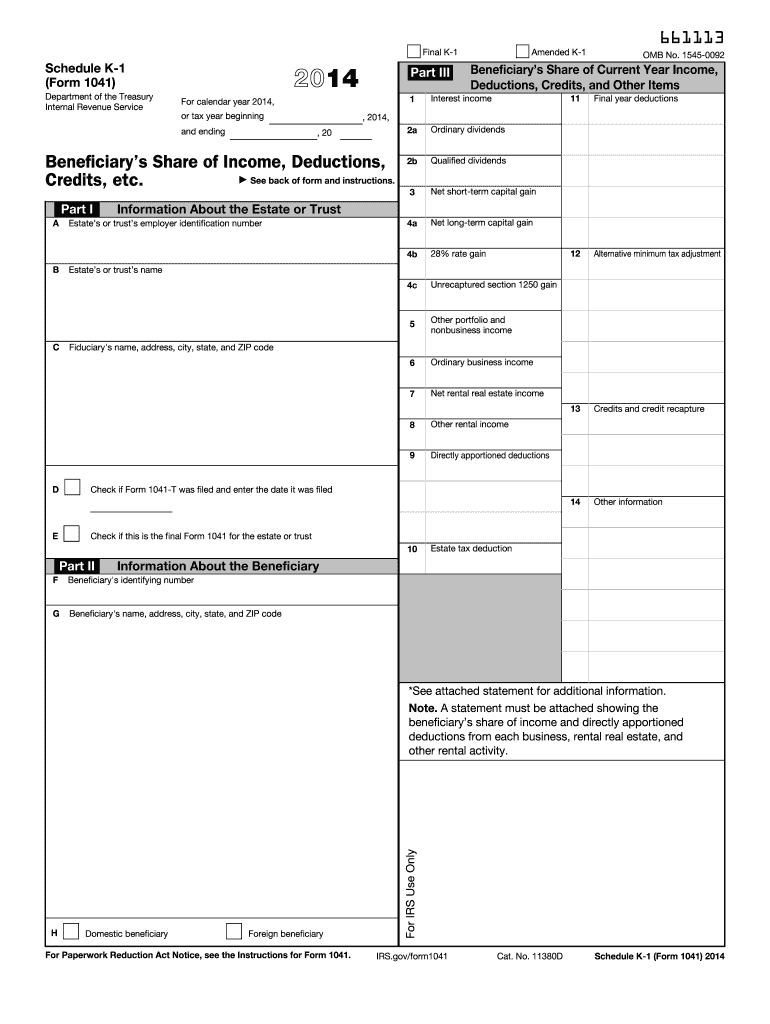

IRS 1041 - Schedule K-1 2014 free printable template

Get, Create, Make, and Sign IRS 1041 - Schedule K-1

Instructions and Help about IRS 1041 - Schedule K-1

How to edit IRS 1041 - Schedule K-1

How to fill out IRS 1041 - Schedule K-1

About IRS 1041 - Schedule K-1 2014 previous version

What is IRS 1041 - Schedule K-1?

When am I exempt from filling out this form?

What are the penalties for not issuing the form?

Is the form accompanied by other forms?

What is the purpose of this form?

Who needs the form?

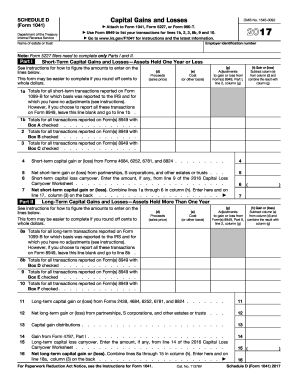

Components of the form

What information do you need when you file the form?

Where do I send the form?

FAQ about IRS 1041 - Schedule K-1

What should I do if I realize I've made a mistake on my filed IRS 1041 - Schedule K-1?

If you've made a mistake on your IRS 1041 - Schedule K-1 after filing, you should submit an amended return using Form 1041-X. This allows you to correct the errors and ensure that the information reported aligns with your tax obligations. It's essential to provide accurate information to avoid complications during the review process.

How can I verify if my IRS 1041 - Schedule K-1 has been received by the IRS?

You can verify if your IRS 1041 - Schedule K-1 has been received by checking the status through your IRS online account or by contacting the IRS directly. Be prepared to provide relevant details such as your Social Security number and the tax year in question to facilitate the inquiry.

What common errors should I be aware of when submitting an IRS 1041 - Schedule K-1?

Common errors when submitting an IRS 1041 - Schedule K-1 include incorrect taxpayer identification numbers, mismatched names, and omitting required income details. Carefully reviewing each entry before submission can help prevent these issues and ensure compliance with IRS requirements.

Are there specific privacy and data security measures I should take when submitting my IRS 1041 - Schedule K-1?

When submitting your IRS 1041 - Schedule K-1, it is crucial to use secure methods, such as e-filing through authorized providers or mailing forms via certified mail. Additionally, ensure that your personal and financial information is protected by using strong passwords and encrypted communications when communicating with tax preparers.