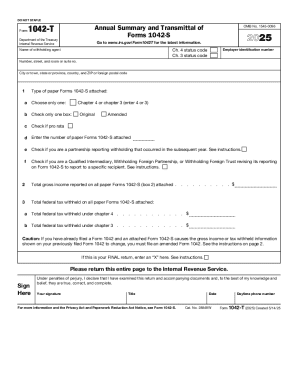

What is IRS 1042-T?

IRS 1042-T is a tax form used by withholding agents and foreign embassies to report income subject to withholding. It serves as a summary of the forms 1042-S, detailing the amounts paid to foreign individuals or entities. This form ensures transparency and compliance with U.S. tax regulations regarding non-resident payments.

Who needs the form?

IRS 1042-T must be filed by U.S. withholding agents, including banks, businesses, and other organizations that pay income to foreign individuals or entities. If you are making payments such as interest, dividends, rents, or royalties to foreign persons, you are required to submit this form along with the corresponding 1042-S forms for each recipient.

Components of the form

The IRS 1042-T includes several key components that require careful completion. These components are as follows:

01

Withholding Agent Information: Name, address, and TIN of the withholding agent.

02

Summary of Payments: Aggregate amounts paid to foreign recipients.

03

Recipient Details: Names, addresses, and TINs of the foreign persons who received payments.

04

Certification Information: Signature of the withholding agent confirming the accuracy of the information.

What information do you need when you file the form?

When filing the IRS 1042-T, it’s essential to gather specific information. You will need details about the payment recipients, including their names, addresses, and TINs. Additionally, you will collect the total amounts paid to each recipient and the type of income that was paid. Ensuring accuracy in this data is crucial to avoid penalties and ensure compliance.

What is the purpose of this form?

The purpose of IRS 1042-T is to report certain payments made to foreign persons or entities that may be subject to U.S. tax withholding. This form summarizes the data provided on the various IRS 1042-S forms issued to individual recipients. Filing this form helps the IRS track withholding amounts and verify compliance with tax obligations for foreign recipients.

When am I exempt from filling out this form?

You may be exempt from filling out IRS 1042-T if your payments fall under certain exclusions. For instance, payments made to U.S. citizens or residents do not require this form. Additionally, certain payments that are exempt from withholding, such as scholarships for foreign students, are also excluded from reporting requirements under the 1042-T.

What are the penalties for not issuing the form?

Failure to issue IRS 1042-T can result in significant penalties for withholding agents. The IRS imposes fines based on the lateness of the filing, the seriousness of the failure, and whether the failure was intentional. If you neglect to file or file late, you may be subject to fines ranging from $50 to $270 per form, with maximum penalties reaching $1.5 million per calendar year.

Is the form accompanied by other forms?

Yes, IRS 1042-T is typically accompanied by IRS 1042-S forms. While 1042-T serves as a summary of all 1042-S forms, each 1042-S must be filed for every payment made to foreign individuals or entities. Therefore, complete both forms for accurate reporting and compliance.

Where do I send the form?

The IRS 1042-T form should be mailed to the address specified on the form instructions. Generally, this includes the address for the appropriate processing center, which can depend on the withholding agent's location and whether the submission is being sent with a payment or not. Be sure to check the latest IRS guidelines for the most accurate mailing information.