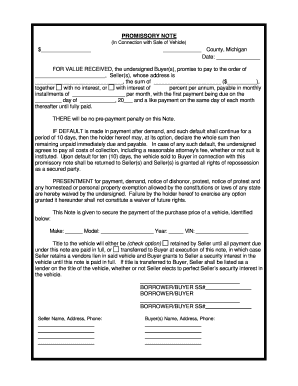

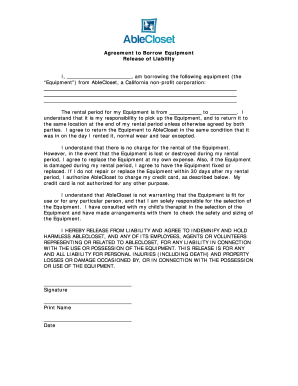

Lending Terms And Conditions Template

There’s no need to search through hundreds of terms and conditions samples trying to find one that is similar to what your business needs. Instead, you can simply select a template from the list of Lending Terms And Conditions forms listed below. The forms available in this section already contain the provisions specific to your industry. All you need to do is fill in your company information and adjust any provisions as needed. Open a template in our convenient document editor and easily create a legal agreement.

What is Lending Terms And Conditions Template?

A Lending Terms and Conditions Template is a document that outlines the terms and conditions under which a lender is willing to provide a loan to a borrower. It includes important information such as the loan amount, interest rate, repayment schedule, and any other specific terms agreed upon between the lender and borrower.

What are the types of Lending Terms And Conditions Template?

There are several types of Lending Terms and Conditions Templates available, including but not limited to:

How to complete Lending Terms And Conditions Template

Completing a Lending Terms and Conditions Template is a straightforward process. Here are the steps to follow:

pdfFiller empowers users to create, edit, and share documents online. Offering unlimited fillable templates and powerful editing tools, pdfFiller is the only PDF editor users need to get their documents done.