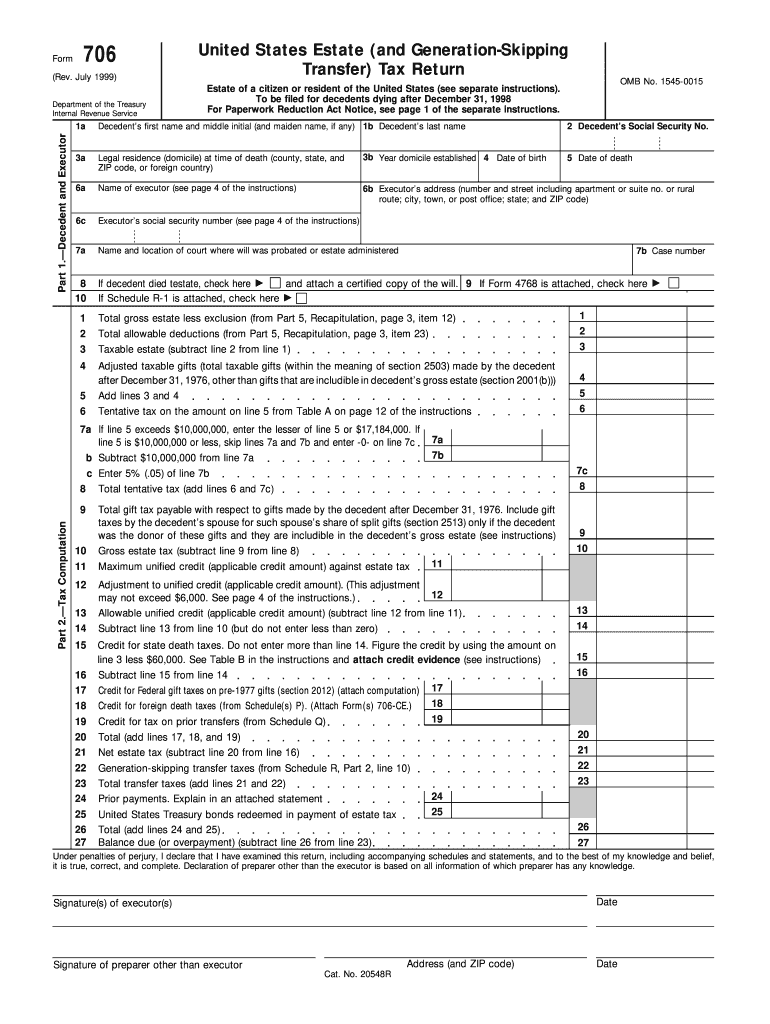

IRS 706 1999 free printable template

Show details

Rent of 600 payable monthly. Value based on appraisal copy of which is attached 96 000 November 1. Value based on appraisal copy of which is attached. Not disposed of within 6 months following death 7/1/99 90 000 February 1 1999 exchanged for farm on May 1 1999 2032A Valuation specially valued property received by the skip person at their special use value and one showing the same interests at their fair market value. The election to value certain farm and closely held business property at...

pdfFiller is not affiliated with IRS

Get, Create, Make and Sign

Edit your 1999 706 form form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your 1999 706 form form via URL. You can also download, print, or export forms to your preferred cloud storage service.

How to edit 1999 706 form online

Use the instructions below to start using our professional PDF editor:

1

Register the account. Begin by clicking Start Free Trial and create a profile if you are a new user.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit 1999 706 form. Add and change text, add new objects, move pages, add watermarks and page numbers, and more. Then click Done when you're done editing and go to the Documents tab to merge or split the file. If you want to lock or unlock the file, click the lock or unlock button.

4

Get your file. When you find your file in the docs list, click on its name and choose how you want to save it. To get the PDF, you can save it, send an email with it, or move it to the cloud.

The use of pdfFiller makes dealing with documents straightforward.

IRS 706 Form Versions

Version

Form Popularity

Fillable & printabley

How to fill out 1999 706 form

How to fill out 1999 706 form:

01

Gather all necessary information and documents related to the estate, including the deceased person's assets and liabilities, as well as any previous gift tax returns.

02

Start by identifying the decedent and the executor or personal representative of the estate on the first page of the form.

03

Provide detailed information about the decedent's assets and liabilities, including their fair market value at the time of death.

04

Calculate the total taxable estate by subtracting any allowable deductions from the total gross estate.

05

Determine the applicable tax rate and calculate the tentative tax on the taxable estate.

06

Report any previous taxable gifts made by the decedent and calculate the tax on those gifts.

07

Combine the tentative tax on the taxable estate with the tax on previous taxable gifts to arrive at the total federal estate tax.

08

Consider any available credits, such as the unified credit, that can be used to reduce the total federal estate tax.

09

Finally, calculate the net federal estate tax due by subtracting the credits from the total federal estate tax.

10

Sign and date the form, and provide any required attachments or schedules.

Who needs 1999 706 form:

01

Executors or personal representatives of an estate that meets certain criteria are required to file Form 706.

02

This form is typically used when the total gross estate, plus the adjusted taxable gifts and specific exemptions, exceeds a certain threshold set by the Internal Revenue Service (IRS).

03

It is important to consult with a tax professional or review the IRS instructions to determine whether filing the 1999 706 form is necessary for a specific estate.

Instructions and Help about 1999 706 form

Hello we will be going over form 706 together and if you want you can pull up your own copy of form 706, so I can pause this video then come back and let's go to that form 706 together your job is to prepare the in product which is the form 706 on your midterm and I expect form 706 to be as complete as possible a list that a list of what should be attached to the return but not the actual attachments should be included because I will not be reproducing the documents to include any attachments, but we want the return to look as complete as possible when you complete a form 706 I have a copy here we're going to go through some schedules and various pages of the form you're telling the deceit and story, but it reflects a snapshot of where the deceit was at the time of death it's important to be complete when you prepare them the starting point is to determine if a return is required the first step is to determine if the gross estate which is gross estate tax I should say on line 8 which you can see here exceeds the required exclusion amount, and you can see the exclusion amounts computed here in section 9 but when you compare those two numbers it still isn't quite that simple there are adjustments that have to be made and the adjustments to the exclusion amount are in the lines that follow the basic exclusion shown online a and those amounts those adjustments are the adjusted taxable gifts which are the pulse 76 gifts not included in the tax for state we have to reduce the applicable exclusion for any exam that was taken after September 8, 1976, and what I'm discussing now is shown here on line 10 in the 76 act they went from an exemption to what we now have today which is the unified credit when they made a change in the law going from this exemption to the unified credit that we have today for the period 98 76 to the end of 1976 if you used your exemption you had to reduce your credit by 20% of the exemption you use so that affects our clickable exclusion amount and that's why you see this adjustment that needs to be made whether you have to file a tax of form 706 depends on the amount of the gross estate not the net estate that generates an estate tax if we add back the exemption that we talked about not too long ago that you use posts September 8, 1976, as well as your adjusted taxable gifts let's see where that is on line 4 — your taxable estatonlinenrevisited FIF that amount exceeds the amount when you take your tax for state, and they're just a taxable gifts if is those two amounts exceeds your applicable exclusion amount that's on line 9 see for the most part then you know that you're going to have enough to require you to file a tax return so that's just a quick way of trying to gauge it not not so quick but at least before you go through everything in all the schedules so basically the filing requirement is the function of your gross estate now in addition to that if you have a situation where you have a dispute a deceased spouse's...

Fill form : Try Risk Free

People Also Ask about 1999 706 form

What is the alternate valuation date for 706?

What was the GST exemption in 1999?

What is the penalty for filing 706 late?

What is tax form 706 used for?

What was the estate tax credit in 1999?

What year 706 should I file?

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

What is 706 form?

The 706 form is a federal tax form, officially known as Form 706: United States Estate (and Generation-Skipping Transfer) Tax Return. It is used by the executors of a deceased individual's estate to report the transfer of assets and determine any estate tax liability. This form must be filed within nine months after the decedent's death, and it provides information about the assets, debts, and beneficiaries of the estate.

Who is required to file 706 form?

The 706 form, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is required to be filed by the executor or administrator of the estate of a deceased person. This form is used to report the estate's assets, calculate any estate tax owed, and determine if any generation-skipping transfer tax applies.

What is the purpose of 706 form?

Form 706, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is a tax form used to calculate and report federal estate taxes owed on the estate of a deceased individual. Its purpose is to determine the value of the estate, calculate the estate tax liability, and report the transfer of property to beneficiaries or other parties. The form must be filed by the executor or administrator of the estate for any US citizen or resident whose estate, combined with any lifetime taxable gifts, exceeds the applicable threshold set by the Internal Revenue Service (IRS).

When is the deadline to file 706 form in 2023?

The deadline to file a 706 form, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, in 2023 is typically nine months after the date of the individual's death. However, it's essential to note that tax laws are subject to change, so it is advisable to consult with a tax professional or refer to the Internal Revenue Service (IRS) website for the most accurate and up-to-date information.

What is the penalty for the late filing of 706 form?

The penalty for the late filing of Form 706, which is the United States Estate (and Generation-Skipping Transfer) Tax Return, can vary depending on the circumstances. The penalty is typically calculated based on the amount of tax owed that is not paid by the original due date of the return. The penalty can be up to 25% of the unpaid tax amount, and it may accrue interest as well. Additionally, if there is reasonable cause for the delay in filing, the penalty may be waived or reduced. It is important to consult with a tax professional or review the specific instructions and guidelines provided by the Internal Revenue Service (IRS) for accurate and up-to-date information on penalties for late filing of Form 706.

How to fill out 706 form?

Filling out Form 706, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, can be a complex process. Here is a general guide on how to fill out the form:

1. Understand the purpose of Form 706: Form 706 is used to calculate and report any estate taxes owed after someone's death. It includes information about the decedent, their assets, debts, and distribution of their estate.

2. Gather the necessary information and documentation: Collect all relevant information, including the decedent's personal details (such as name, Social Security number, date of death), their will, and any other legal documentation related to the estate. Also, gather information about the decedent's assets and liabilities, including bank accounts, real estate, investments, debts, etc.

3. Complete the header section: Provide the decedent's personal details, including name and Social Security number. Fill in the date of death as well, as this will determine the applicable tax laws.

4. Determine the filing status and election: Determine the filing status based on whether the estate is required to file Form 706. Additionally, choose whether the estate makes an election to allow the surviving spouse to use any unused portion of the decedent's estate tax exemption (known as the "portability election").

5. Calculate the gross estate: Determine the total value of the decedent's assets using fair market values as of the date of death. This includes real estate, stocks, bonds, personal property, etc. Subtract any allowable deductions (e.g., mortgages, debts, and administrative expenses) to arrive at the value of the gross estate.

6. Determine the taxable estate: Make adjustments to the gross estate by subtracting allowable deductions, such as funeral expenses, debts, qualifying charitable bequests, and marital deduction if applicable. This will arrive at the taxable estate value.

7. Calculate and pay estate tax: Use the taxable estate value to determine the estate tax owed. Refer to the appropriate tax tables and instructions provided by the IRS to calculate the tax liability accurately. Pay any tax due with the submission of the form.

8. Complete the remainder of the form: Provide detailed schedules and supporting documents as requested in Form 706. These schedules will depend on the specifics of the decedent's estate.

9. Sign and submit the form: Sign the completed Form 706 and attach any required schedules and supporting documents. Send the form to the appropriate IRS processing center as indicated in the instructions.

It is crucial to note that the information provided here is only a basic overview. Form 706 can be complex, and it is recommended to consult with a tax professional or estate attorney for guidance to ensure accurate completion before submission.

What information must be reported on 706 form?

Form 706 is the United States Estate (and Generation-Skipping Transfer) Tax Return. It must be filed by the executor of a deceased person's estate and reports the value of their taxable estate and any generation-skipping transfers.

The following information must be reported on Form 706:

1. Decedent Information: This includes the name, Social Security number, date of birth, date of death, and address of the deceased person.

2. Executor Information: The name, address, and Social Security number of the person responsible for administering the estate.

3. Estate Assets: The value of all assets owned by the decedent at the time of death must be reported. This includes real estate, bank accounts, investments, life insurance proceeds, business interests, and personal belongings.

4. Estate Liabilities: Any debts, mortgages, loans, or other obligations of the decedent that are owed at the time of death are reported.

5. Funeral Expenses: The cost of the decedent's funeral and burial expenses must be reported.

6. Debts and Administrative Expenses: Any expenses related to the administration of the estate, such as attorney fees, court costs, and appraiser fees, must be reported.

7. Charitable Bequests: If the decedent included any charitable donations in their will or estate plan, these must be reported.

8. Generation-Skipping Transfers: If the decedent made any transfers to grandchildren or others that skipped a generation, these must be reported separately.

9. Estate Tax Computation: This section calculates the amount of federal estate tax owed based on the value of the taxable estate and applicable tax rates.

10. Signature and Verification: The executor signs the form under penalty of perjury, confirming that the information provided is true, accurate, and complete.

It is important to consult with a qualified tax professional or attorney for specific guidance and to ensure accurate completion of Form 706.

How do I make changes in 1999 706 form?

The editing procedure is simple with pdfFiller. Open your 1999 706 form in the editor. You may also add photos, draw arrows and lines, insert sticky notes and text boxes, and more.

How do I edit 1999 706 form in Chrome?

Install the pdfFiller Google Chrome Extension in your web browser to begin editing 1999 706 form and other documents right from a Google search page. When you examine your documents in Chrome, you may make changes to them. With pdfFiller, you can create fillable documents and update existing PDFs from any internet-connected device.

How do I complete 1999 706 form on an iOS device?

Install the pdfFiller app on your iOS device to fill out papers. If you have a subscription to the service, create an account or log in to an existing one. After completing the registration process, upload your 1999 706 form. You may now use pdfFiller's advanced features, such as adding fillable fields and eSigning documents, and accessing them from any device, wherever you are.

Fill out your 1999 706 form online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Not the form you were looking for?

Keywords

Related Forms

If you believe that this page should be taken down, please follow our DMCA take down process

here

.