Home Budget Templates

What are Home Budget Templates?

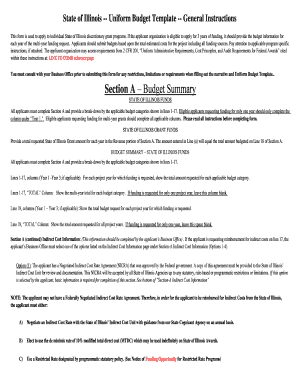

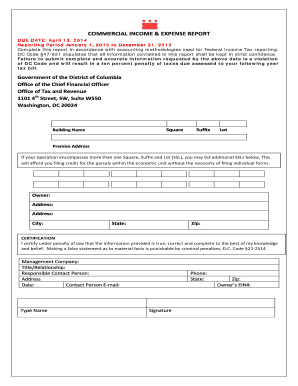

Home budget templates are pre-designed spreadsheets or forms that help individuals and families track their income, expenses, and savings. These templates provide a structured framework for organizing financial information and making informed decisions about personal finances. Whether you're managing your monthly household budget, planning for a big purchase, or saving for the future, home budget templates can be valuable tools in managing your money effectively.

What are the types of Home Budget Templates?

There are several types of home budget templates available to cater to different financial needs and preferences. Some common types include:

How to complete Home Budget Templates

Completing home budget templates is a straightforward process that requires gathering and inputting relevant financial information. Here are the steps to follow:

pdfFiller empowers users to create, edit, and share documents online. Offering unlimited fillable templates and powerful editing tools, pdfFiller is the only PDF editor users need to get their documents done.